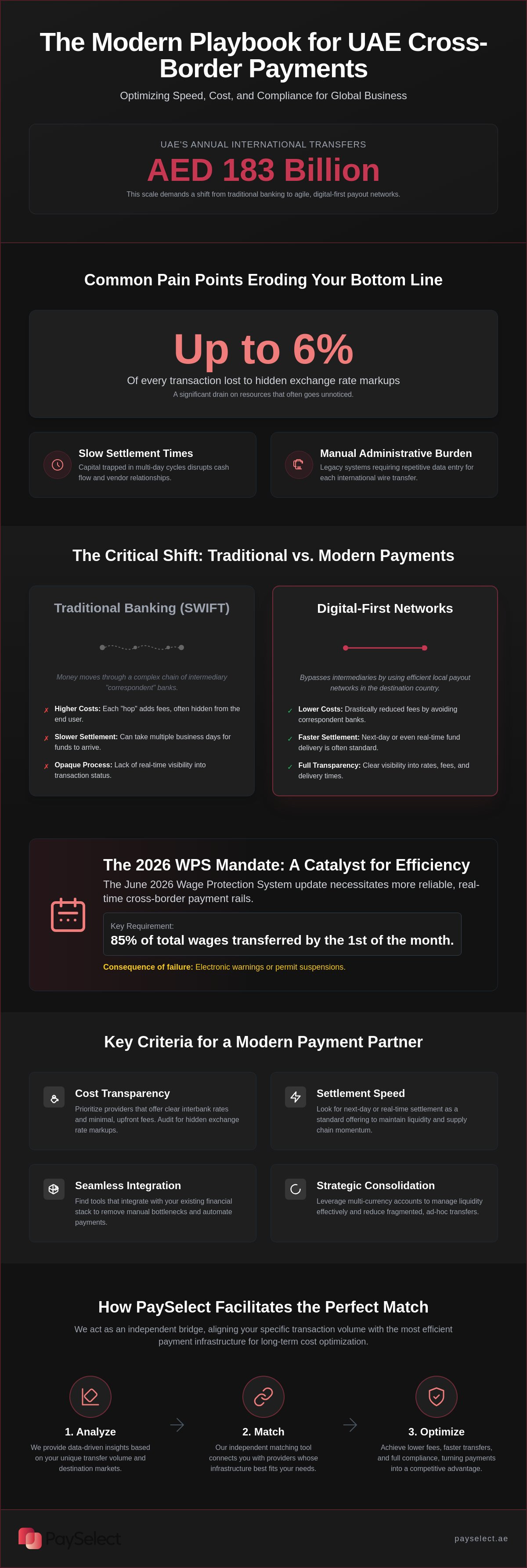

Did you know that while the UAE processes over AED 183 billion in cross-border transfers annually, many enterprises still lose up to 6% of every transaction to hidden exchange rate markups? It's a significant drain on resources that often goes unnoticed until you scrutinize the interbank rates. To protect your margins and scale effectively, you must compare business money transfer providers uae with a focus on transparency, speed, and cost efficiency.

You likely recognize the friction caused by slow settlement times and the heavy administrative burden of manual wire transfers. With the June 2026 Wage Protection System (WPS) updates now requiring 85% of total wages to be transferred by the first of each month, the need for operational efficiency has never been more urgent. We promise to help you master these complexities by adopting a strategic approach to your international payment infrastructure.

This guide provides a clear framework for selecting the right partners to achieve lower fees and real-time visibility into your global cash flow. We will examine how PaySelect acts as an independent bridge, helping you identify tools that integrate seamlessly with your financial stack while removing the operational barriers that hinder your international ambition.

Key Takeaways

• Identify the shift from traditional correspondent banking to digital-first networks to ensure your enterprise stays competitive in the 2026 global market.

• Learn how to compare business money transfer providers uae by auditing hidden exchange rate markups and prioritizing providers that offer next-day settlement as standard.

• Discover how to transition from fragmented, ad-hoc transfers to a consolidated strategy that leverages multi-currency accounts for better liquidity management.

• Understand the critical role of the 2026 Wage Protection System updates and how they necessitate more reliable, real-time cross-border payment rails.

• Leverage independent matching tools to align your specific transaction volume with the most efficient payment infrastructure for long-term cost optimization.

The Evolving Landscape of Business International Money Transfers

The UAE's position as a global commerce powerhouse is undisputed in 2026. Its fintech sector grew by over 35% in 2025, reflecting a massive shift in how capital moves across borders. UAE enterprises now manage approximately AED 183 billion in annual international transfers. This scale demands a transition from traditional correspondent banking to agile, digital-first payout networks. These modern systems don't just move funds; they optimize liquidity by ensuring capital isn't trapped in multi-day settlement cycles.

To navigate this fast-moving environment, leaders must compare business money transfer providers uae with precision. Relying on a single legacy bank often leads to stagnant processes and high overheads. Diversifying your payment infrastructure allows your business to leverage the best technical rails for each specific market you enter. It's a strategic move that transforms a back-office necessity into a competitive advantage.

The Shift from Traditional Banking to Digital Platforms

Traditional banking relies on the SWIFT relay, a system where money moves through a chain of intermediary institutions. When you look at how wire transfers work, you see how each "hop" adds costs and settlement time. Digital-first providers bypass this by using local payout networks in emerging markets. They settle funds domestically, which often allows for next-day or even real-time delivery. This efficiency is why many UAE firms now use a mix of providers to ensure they always have a high-speed path to their vendors and partners.

Common Pain Points for National Enterprises

Expansion often brings hidden costs that erode your bottom line. Opaque foreign exchange markups and the administrative weight of manual wire transfers can stall growth. Compliance is another critical factor. The June 1, 2026, update to the Wage Protection System (WPS) requires employers to pay 85% of total wages by the first of the month. Failure to meet these deadlines leads to electronic warnings or permit suspensions. Common frictions include:

Currency Conversion Losses

High markups above the interbank rate that are often hidden in the total cost.

Regulatory Pressure

Meeting strict WPS and Central Bank reporting thresholds for transfers exceeding AED 3,500.

Manual Bottlenecks

Legacy systems requiring repetitive data entry for every international transaction.

PaySelect addresses these frictions by offering a cross-border payment solution matching tool. It serves as an independent guide, helping you find a provider that integrates with your financial stack and removes operational barriers. Instead of guessing which service fits your volume, you can use data-driven insights to optimize every transfer.

Understanding the Mechanisms of Cross-Border Payments

Cross-border payments are the digital conduits that allow capital to flow across national boundaries. While the sheer scale of global remittance flows illustrates the volume of individual transfers, B2B commerce requires far more sophisticated rails. These rails represent the technical infrastructure used to move funds from an AED account within the UAE to a vendor's account abroad. Understanding these mechanisms is the first step toward reducing operational friction.

Most international business transactions rely on "push" mechanisms. This means the sender initiates the transfer, providing full control over the timing and security of the capital. In contrast, "pull" mechanisms, like global direct debits, allow the receiver to initiate the collection. For UAE enterprises, push payments remain the standard for high-value vendor settlements because they offer a clear audit trail and immediate confirmation of dispatch.

Liquidity providers play a silent but vital role in this process. They ensure that when you convert AED to another currency, there is sufficient volume to maintain a stable price. In traditional wire transfers, your funds often pass through intermediary banks. These entities act as bridges between the sending and receiving institutions, but they frequently introduce additional fees and settlement delays that can disrupt your supply chain.

SWIFT vs. Local Payout Networks

The SWIFT network is a messaging protocol that instructs banks on how to move money. Because it relies on a chain of correspondent banks, it often results in opaque fees and multi-day waiting periods. Local-to-local models offer a more efficient alternative. By using these systems, providers settle your payment through domestic clearing houses in the destination country. Local payout networks are decentralized systems that bypass international correspondent banking to settle funds directly through domestic financial infrastructure for near-instant delivery.

The Role of Foreign Exchange (FX) Management

The mid-market rate is the only "real" exchange rate. It's the midpoint between the buy and sell prices on global currency markets. Most traditional providers add an FX markup to this rate, which acts as a hidden tax on your business growth. For an enterprise transferring large sums, even a 1% markup can result in thousands of dirhams in unnecessary costs. Sophisticated firms use forward contracts to mitigate this risk, allowing them to lock in a specific exchange rate for future payments and protect their margins from market volatility.

If you want to eliminate these hidden costs, it's essential to compare business money transfer providers uae to see which ones offer the most transparent FX structures. Using an independent matching tool can help you identify providers that prioritize mid-market rates over high-margin markups, ensuring more of your capital reaches its intended destination.

Key Criteria for Evaluating Transfer Providers

High performing enterprises don't choose payment partners based on brand name alone. They use a rigorous evaluation framework to ensure every dirham is accounted for. Security is the non negotiable foundation of this framework. You must verify that any partner complies with the latest CBUAE Wire Transfer Requirements. For instance, regulations now mandate that all transfers equal to or exceeding AED 3,500 must be accompanied by full verified details for both the sender and the beneficiary. This regulatory alignment ensures your funds remain secure and your business stays compliant with anti money laundering protocols.

Beyond security, prioritize system connectivity. A solution that doesn't communicate with your existing ERP or accounting software creates unnecessary manual work. It introduces human error and slows down your financial closing cycles. To maintain momentum, you should compare business money transfer providers uae based on how easily they plug into your current financial stack to automate data reconciliation.

Transparency in Fee Structures and FX Markups

Many traditional institutions advertise low flat fees while hiding a significant spread in the exchange rate. This spread is the difference between the interbank mid market rate and the price you are actually charged. A zero fee transfer might actually be your most expensive option if the provider adds a 3% markup to the currency conversion. Use this checklist to audit your current provider:

• Identify the exact timestamp of your transfer and check it against the mid market rate.

• Calculate the percentage difference between the market rate and your quoted rate.

• Look for "correspondent bank fees" that may have been deducted from the final amount received by your vendor.

Settlement Speed and Operational Fluidity

In a global economy, waiting three business days for a payment to clear is no longer acceptable. It stalls your supply chain and erodes vendor trust. Next day settlement has become the new business standard for UAE enterprises. Modern platforms offer 24/7 transfer capabilities and automated payout scheduling. This removes the administrative burden of manual entries and ensures your capital moves as fast as your operations. Faster payments improve your liquidity and allow you to negotiate better terms with global suppliers who value certain and immediate payment.

PaySelect helps you navigate these choices through its cross-border payment solution matching tool. It acts as an independent guide, helping you cut through the fine print to find a provider that balances speed and cost tailored to your specific transaction volume.

Optimising Your International Payment Infrastructure

Scaling a UAE enterprise requires moving beyond one-off, ad-hoc transfers. A fragmented approach to global commerce often leads to "leakage," which refers to small, recurring losses caused by poor timing, inefficient rails, or redundant fees. To protect your margins, you must transition to a consolidated payment strategy. This involves auditing your existing setup to identify where manual processes are slowing down your financial team and where automated solutions can take over.

One of the most effective ways to drive efficiency is through the strategic use of multi-currency accounts. These digital wallets allow you to hold, receive, and spend funds in multiple global currencies without the need for constant, costly conversions. By holding funds in the currency of your vendors, you eliminate the "hidden tax" of FX markups on every transaction. When you compare business money transfer providers uae, look for those that offer robust multi-currency capabilities as a standard feature rather than an expensive add-on.

A comprehensive infrastructure audit can reveal significant cost saving opportunities. Many businesses find that they're paying for premium features they don't use or are stuck with legacy providers that haven't updated their pricing in years. Optimising your stack isn't just about saving money; it's about building a resilient foundation that supports international ambition without increasing your administrative load. For those managing operations in the UK, using a platform like greencompare.co.uk can help you compare and secure the best commercial utility and business finance rates to further reduce overhead.

Managing Mass Payouts and Global Supply Chains

If your business manages hundreds of international invoices, individual wire transfers are no longer viable. Batch processing allows your team to upload a single file to execute multiple payments simultaneously, saving hours of manual labor and reducing the risk of data entry errors. Modern platforms also automate the KYC (Know Your Customer) process for international beneficiaries, ensuring that every recipient is verified before funds are released. For retail and service businesses, linking your POS systems with global payout accounts creates a fluid cycle where domestic revenue can be quickly deployed to satisfy international supply chain obligations.

Regulatory Compliance and Security Standards

Security isn't a feature; it's a prerequisite. As digital payment regulations in the MENA region evolve, staying compliant with Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) protocols is vital. You should ensure your chosen provider utilizes bank grade data encryption and mandatory two factor authentication for all business accounts. These layers of protection shield your capital from external threats and internal fraud. A secure infrastructure gives you the calm assurance needed to focus on expansion rather than risk management.

To find the most efficient setup for your specific needs, you can compare business money transfer providers uae using our independent tool. It's designed to align your transaction volume with the most secure and cost-effective payout networks available in 2026.

How PaySelect Facilitates the Perfect Provider Match

In a market saturated with marketing claims, an independent perspective is your most valuable asset. Many platforms are incentivized to favor specific providers, which can lead to biased recommendations that don't serve your bottom line. PaySelect operates as an unbiased bridge between complex global infrastructures and your specific business needs. We provide the clarity required to compare business money transfer providers uae without the noise of hidden agendas. This ensures your choice is based on technical utility and cost efficiency rather than a provider's marketing budget.

Our specialized matching tool aligns provider capabilities with your actual transaction volume. It's a data-driven approach that simplifies the cross-border payment selection process. By analyzing your specific corridors and settlement requirements, we help you identify the rails that offer the most fluidity and security for your capital. We don't just list options; we find the exact technical fit that allows your enterprise to scale with confidence.

Using Independent Data to Drive Financial Decisions

Success in the digital economy depends on moving beyond surface-level promises to real-world performance metrics. PaySelect gives you access to unbiased comparisons of payment gateways and international payout providers. We focus on the ultimate business outcome: lower fees, faster settlements, and seamless system connectivity. This transparency builds the operational confidence needed to expand your international footprint without fear of unforeseen costs. When you have the right data, you can make decisions that lead to long-term savings and a leaner financial stack.

Bespoke Advisory for Enterprise Scale

For large-scale organisations and hotel groups, a standard off-the-shelf solution is rarely sufficient. These entities require a tailored infrastructure audit to identify deep-seated inefficiencies. PaySelect offers high-level consulting and a Payment Cost Optimization Audit specifically designed for enterprise needs. We work with you to re-architect your payment stack, focusing on reducing Merchant Discount Rates (MDR) and optimizing every point of contact in your financial flow. Partnering with experts who understand the complex MENA landscape allows you to navigate regulatory shifts with calm assurance. This strategic partnership ensures your business remains a leader in global commerce while maintaining absolute control over its cross-border costs.

Secure Your Competitive Advantage in Global Commerce

The landscape of international commerce in 2026 demands more than just reliability; it requires speed and absolute cost transparency. Moving away from legacy correspondent banking allows your enterprise to unlock trapped liquidity and strengthen vendor relationships through next-day settlements. By implementing multi-currency accounts and mass payout automation, you remove the operational barriers that often stall international expansion.

To ensure your financial stack remains lean and compliant with the latest CBUAE regulations, you must strategically compare business money transfer providers uae. Relying on surface-level marketing claims isn't enough for a sophisticated organization. PaySelect provides the independent and unbiased advisory you need to navigate the complex MENA payments landscape with confidence. Our specialized UAE market expertise and proven cost-optimisation frameworks help you identify the perfect technical match for your specific transaction volume.

Find the best cross-border payment solution for your business and transform your payment infrastructure into a strategic tool for growth. The future of your global success depends on the fluidity of your capital. Take control of your international payments today and build a foundation for limitless ambition.

Frequently Asked Questions

What is the cheapest way to send business money internationally from the UAE?

Digital-first payout networks are generally the most cost-effective option because they bypass traditional intermediary bank fees. While banks often charge 2% to 6% in exchange rate markups, fintech providers often offer rates much closer to the mid-market benchmark. You should compare business money transfer providers uae to identify those with transparent fee structures that don't hide costs in the spread.

How long do business international money transfers typically take in 2026?

Next-day settlement is the current business standard in the UAE, with many digital providers facilitating near-instant transfers. Traditional SWIFT transfers can still take 3 to 5 business days due to the chain of correspondent banks involved. Choosing a provider with local payout networks in your destination country is the fastest way to ensure your capital reaches vendors without delay.

Are digital payout platforms as secure as traditional UAE banks?

Yes, digital payout platforms are highly secure as long as they're licensed and regulated by the Central Bank of the UAE. These institutions must adhere to the same rigorous AML and CTF protocols as traditional banks. They utilize bank-grade encryption and two-factor authentication to protect your enterprise's capital and sensitive data.

What information do I need to provide for a business cross-border transfer?

You must provide the full name, account number, and address or identification details for both the sender and the beneficiary. For any transfer equal to or exceeding AED 3,500, current CBUAE regulations mandate that this data is fully verified. Ensuring this information is accurate prevents delays and ensures compliance with international wire transfer standards.

Can I automate my international vendor payments from the UAE?

Automation is entirely possible through batch processing and mass payout tools offered by modern providers. You can upload payment files directly or use API integrations to link your financial stack with your payout provider. PaySelect can help you find a partner that supports these automated workflows to reduce your administrative burden.

How do I avoid hidden exchange rate markups on business transfers?

Always check your provider's quoted rate against the real-time mid-market rate to identify the hidden spread. Many providers advertise low or zero fees while adding a significant markup to the exchange rate itself. To protect your margins, you should compare business money transfer providers uae that commit to transparent, spread-based, or flat-fee pricing models.

What is the difference between a payment gateway and a cross-border payout solution?

A payment gateway is designed to accept payments from customers, whereas a cross-border payout solution is used to send funds to international vendors or employees. While some providers offer both, they serve different functions in your financial infrastructure. Gateways focus on the "pull" of revenue, while payout solutions manage the "push" of global expenses and supply chain settlements.

Is there a limit on how much money a business can transfer internationally?

There is no legal limit on the amount a business can transfer, provided you comply with reporting and verification requirements. However, individual providers or banks may have their own internal caps based on your account's risk profile or transaction history. For large enterprise-scale transfers, working with a specialist consultant can help you navigate these limits and optimize your transfer strategy.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.