Your headline processing rate is a marketing tactic designed to mask the actual drain on your bottom line. While a low percentage looks attractive on a landing page, the reality of calculating the total cost of a payment gateway involves navigating a maze of interchange settlements, network assessments, and hidden "junk" fees. You likely face the frustration of unpredictable monthly statements and complex PCI compliance charges that stall your operational momentum. We agree that this lack of transparency creates unnecessary barriers for businesses ready to scale.

This guide empowers you to master these complexities and uncover your true effective rate for maximum profitability. You'll gain a clear formula to compare providers and leverage the latest 2026 interchange fee reductions to lower your transaction costs. PaySelect facilitates this transition by providing payment pricing comparisons and cost optimization audits that strip away the noise. We explore how different pricing models impact your settlement cycles and reserve requirements, transforming your payment setup into a strategic tool for international growth.

Key Takeaways

• Understand why headline rates are often marketing tactics and how to define your true Total Cost of Ownership.

• Master the specific formula for calculating the total cost of a payment gateway to reveal hidden fees across your monthly statements.

• Compare flat-rate, tiered, and interchange-plus models to select the most transparent and cost-effective structure for your business scale.

• Leverage PaySelect’s pricing comparison tools to navigate unpredictable statements and remove the complexity of comparing different provider models.

• Transform your payment setup into a strategic advantage by optimizing your infrastructure for faster settlements and higher profitability.

Beyond the Headline Rate: Why Total Cost of Ownership Matters

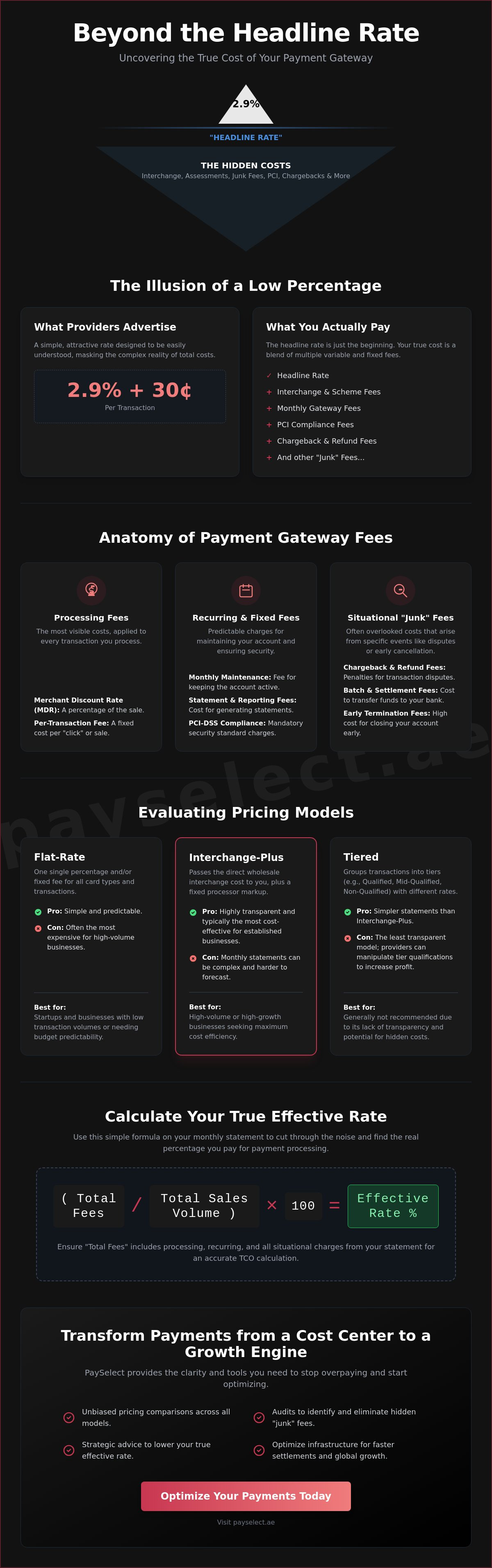

The headline rate is a marketing facade. When you see a flat 2.9% fee, it's easy to assume your costs are predictable. However, for most merchants, that 2.9% is simply the starting point. True profitability depends on calculating the total cost of a payment gateway by looking at the entire ecosystem of fees, technical debt, and operational friction. In the 2026 landscape, a competitive edge isn't found in the lowest percentage; it's found in the highest efficiency. Total Cost of Ownership (TCO) accounts for every dollar that leaves your business, whether it's through a visible transaction fee or a hidden administrative burden.

Inefficient gateways act as a silent drain on your margins. If your infrastructure doesn't support rapid scaling or international expansion, you're paying a "cost of inaction." Choosing a provider based solely on a low entry rate can lead to significant technical hurdles later. This results in lost revenue from failed transactions and higher costs for custom workarounds. PaySelect helps businesses avoid these traps by providing a payment gateway comparison that highlights the long-term impact of different fee structures.

The Illusion of the Low Percentage

Low percentages often hide a multitude of fixed costs. A Payment Service Provider (PSP) may offer an attractive rate but offset it with high per-transaction "cents" fees. These small charges add up quickly, especially for businesses with low average ticket sizes. You must also account for:

• Monthly minimum processing requirements.

• Statement and PCI compliance fees.

• Ancillary charges for "premium" fraud protection or reporting tools.

High-volume businesses often find that a slightly higher percentage with lower fixed fees results in a better effective rate.Operational and Technical Overhead

The true cost includes the resources required to keep the system running. Developer hours for initial API integration and ongoing maintenance are significant expenses. If a gateway lacks reliability, the cost of downtime is measured in lost customer lifetime value. Administrative time spent on manual reconciliation and managing disputes further erodes your profits. A sophisticated partner offers more than just processing; they provide technical utility that acts as a catalyst for growth. By focusing on fluidity and removing operational barriers, you ensure your payment infrastructure supports your international ambition rather than hindering it.

The Anatomy of Payment Gateway Fees: Visible and Invisible Costs

To accurately perform the task of calculating the total cost of a payment gateway, you must dissect the monthly statement into its core components. The most prominent figure is the Merchant Discount Rate (MDR). This is the percentage of each sale kept by the processor. While it seems straightforward, understanding credit card processing fees requires looking at the interplay between this percentage and fixed transaction fees. These "cents" or "fils" per click might seem negligible. However, for businesses with high transaction volumes or small average ticket sizes, they often become the primary cost driver.

One-time setup fees and recurring monthly maintenance charges further complicate the math. These infrastructure costs ensure your system remains connected and secure. You must also account for the penalties of modern retail. Chargeback and refund fees are often overlooked until a dispute occurs. For high-volume merchants, these invisible costs can significantly erode monthly margins. Identifying these variables is essential for any business aiming for long-term financial health.

Hidden "Junk" Fees to Audit

Transparency is often sacrificed for complexity in merchant statements. You should regularly audit your bills for "junk" fees that offer little tangible value. Statement fees and PCI-DSS compliance charges are common examples. While compliance is mandatory, the administrative cost passed to you is often negotiable. Similarly, batch processing and settlement fees—the cost of moving your funds from the gateway to your business bank account—can vary wildly between providers. When calculating the total cost of a payment gateway, these hidden charges often represent the difference between a profitable channel and a break-even one. Be wary of early termination liquidated damages, as these clauses can lock you into an inefficient system.

The Cost of International Ambition

Expanding into global markets introduces a new layer of financial complexity. Cross-border transaction surcharges add weight to every sale made outside your primary region. Beyond the surcharge, currency conversion (FX) markups are a significant revenue stream for gateways. These markups are often baked into the exchange rate, making them difficult to track without a professional payment pricing comparison. For businesses looking to scale globally, optimizing for cross-border payment solutions is essential to protect international margins. If you find your current statement confusing, a Payment Cost Optimization Audit can provide the clarity needed to make an informed decision.

Evaluating Pricing Models: Flat-Rate vs. Interchange-Plus vs. Tiered

Selecting the right pricing structure is the most influential factor when calculating the total cost of a payment gateway. The model you choose determines whether your business benefits from industry-wide rate reductions or remains insulated from potential savings. In the 2026 landscape, the gap between the most expensive and most efficient models has widened. Understanding these differences allows you to move beyond surface-level comparisons and find a partner that aligns with your specific transaction profile.

Subscription-based models have also gained momentum recently. Instead of a traditional percentage-based markup, these providers charge a flat monthly fee for access to wholesale rates. While this offers high predictability for established businesses, it requires a high enough volume to offset the fixed membership cost. For many, the choice remains a balance between simplicity and granular control over every basis point.

Interchange-Plus: The CFO’s Preferred Model

Interchange-plus, often called pass-through pricing, is the gold standard for transparency and scalability. This model separates the non-negotiable bank fee (interchange) from the provider's markup. It's particularly powerful in 2026 following the June settlement that reduced the U.S. combined average effective credit interchange rate by 10 basis points. Under this model, those savings flow directly to your bottom line. It allows for precise calculating the total cost of a payment gateway because every fee is itemized. You can clearly identify interchange optimization opportunities, such as lower rates for standard consumer cards compared to premium or commercial rewards cards. This clarity provides the leverage needed for better negotiation during a payment pricing comparison.

When Flat-Rate Makes Sense

Flat-rate pricing offers an attractive simplicity for low-volume startups and micro-merchants. You pay one consistent rate for all card types, whether it's a basic debit card or an international premium credit card. This simplifies accounting and provides immediate predictability. However, this convenience comes with a hidden cost. Because the rate is averaged out, you often overpay for lower-cost transactions, such as debit card payments. As your volume grows, the "debit card tax" inherent in flat-rate models can drain thousands from your margins. Transitioning to a more transparent model is a natural step for businesses ready to scale. If you're unsure if your current volume justifies a switch, a Payment Cost Optimization Audit can reveal your true effective rate compared to industry benchmarks.

For merchants looking to implement these savings, LyrxPay provides specialized merchant services focused on lower-fee payment processing solutions that can significantly reduce operational costs.

The Danger of Tiered Pricing

Tiered pricing groups transactions into "Qualified," "Mid-Qualified," and "Non-Qualified" buckets. While the "Qualified" rate looks low, providers have the discretion to classify many transactions as "Non-Qualified" at much higher rates. This model is frequently criticized for its lack of transparency. It makes calculating the total cost of a payment gateway nearly impossible until the statement arrives. We recommend avoiding this model in favor of structures that offer clear, unbundled data for every transaction.

The Calculation Framework: Determining Your True Effective Rate

The only metric that provides an objective comparison between providers is the Effective Rate. While marketing materials highlight the Merchant Discount Rate, your bottom line feels the weight of every unstated charge. To master calculating the total cost of a payment gateway, you must look at your historical data through a specific mathematical lens. The Effective Rate formula is simple: (Total Fees / Total Sales Volume) x 100. This single percentage represents the reality of your processing environment, stripping away the complexity of different pricing models.

To get an accurate result, start by aggregating all fees from a three-month statement period. Using a single month is often misleading due to seasonal fluctuations or one-time chargeback events. You must sum every line item: the percentage markup, per-transaction cents, monthly maintenance, and PCI compliance charges. Once you have this total, separate your transaction-based costs from your fixed monthly overhead. This distinction is vital for understanding how your costs will shift as your business scales. If your fixed costs are high, your effective rate will decrease as your volume increases, whereas a high transaction fee remains a constant drain.

The Settlement Delay Factor

True cost isn't just about what you pay; it's about when you get paid. Settlement cycles vary significantly between providers, and the "opportunity cost" of delayed funds can impact your operational liquidity. If one provider offers a T+2 cycle while another requires T+7, you're effectively losing five days of working capital. For a high-volume business, this delay acts as an interest-free loan to the processor. You must also account for the "Rolling Reserve," where a percentage of your funds is withheld to cover potential risk. These withheld funds are part of calculating the total cost of a payment gateway because they restrict your ability to reinvest and grow. Fluidity in your cash flow is a competitive advantage that often outweighs a minor difference in the headline rate.

Benchmarking Your Results

Once you've calculated your effective rate, you need a benchmark to determine if you're overpaying. While average credit card processing fees typically range from 1.5% to 3.5% per transaction, your specific industry and card mix will dictate your ideal target. Identifying red flags is essential. If your calculated effective rate is more than 1% higher than your headline rate, you're likely suffering from "junk" fee bloat or inefficient tier classification. You can use PaySelect’s payment gateway comparison tool to benchmark your current performance against market averages. If your results show significant discrepancy, it's time to leverage a Payment Cost Optimization Audit to identify redundant services and negotiate more transparent terms.

Strategic Optimization: Leveraging Independent Advisory for Cost Reduction

Relying on a single provider for cost analysis is a strategic error. Most payment processors design their statements to be opaque, making it difficult to identify where your margins are being eroded. By leveraging independent advisory, you gain an objective perspective that prioritizes your profitability over provider retention. Independent audits are essential for identifying redundant services and overcharged tiers that often go unnoticed during standard calculating the total cost of a payment gateway. You need a partner that evaluates the landscape without bias to ensure your infrastructure remains lean and efficient.

Negotiation becomes a data-driven exercise. When you present your true effective rate alongside market benchmarks, you gain the leverage needed to lower provider markups. Implementing a multi-gateway strategy further optimizes costs by allowing you to route transactions based on the lowest available rate or the most reliable path. This approach reduces technical risk, enhances operational fluidity, and ensures your business remains resilient in a fast-moving digital economy. You should treat your payment infrastructure as a strategic tool for transformation rather than a static utility.

The PaySelect Advantage

PaySelect acts as a bridge between complex global infrastructures and your intuitive business needs. Our "Take the Test" tool matches your specific transaction volume to the most efficient fee structure available today. We provide an unbiased payment gateway comparison that cuts through the marketing noise of a fragmented market. Our payment infrastructure consulting reduces the technical friction of switching providers, ensuring your transition to a more cost-effective solution is smooth and frictionless. We focus on the user experience as a competitive advantage, helping you remove operational barriers to growth.

Future-Proofing Your Payments

The payments landscape is shifting rapidly. The June 2026 federal settlement has introduced a 10 basis point reduction in interchange fees that many providers have yet to pass on to their merchants. Staying ahead requires a proactive approach to regulatory changes and the continuous monitoring of security controls under PCI DSS 4.0.1. You must prepare for new payment methods like Buy Now Pay Later and Digital Wallets without allowing fee bloat to compromise your margins. Your final step to operational excellence is to compare current market rates now to see how much you could save.

Mastering Your Payment Infrastructure for 2026 and Beyond

Mastering your payment infrastructure is no longer just about accepting transactions; it's about optimizing every basis point for your bottom line. You now have the tools to look past the headline rate and identify the hidden operational drains that stall growth. By applying the effective rate formula and auditing your statements for "junk" fees, you move from passive acceptance to active financial control. This clarity ensures that your capital remains where it belongs: reinvested in your business.

The process of calculating the total cost of a payment gateway reveals whether your current provider supports your international ambition or acts as a barrier to scale. True efficiency requires moving beyond biased advice and leveraging data-driven insights. PaySelect provides the independent, unbiased advisory you need to navigate the landscape with confidence. Our platform utilizes UAE-market specific data and proven cost-reduction strategies for enterprises to ensure your setup remains lean and high-performing. Take the next step toward operational fluidity and maximum profitability today.

Optimize Your Payment Costs with PaySelect’s Comparison Tool and transform your payments into a strategic asset for expansion. You're ready to build a more transparent and profitable future.

Frequently Asked Questions

What is the difference between a headline rate and an effective rate?

The headline rate is the advertised percentage you see in marketing materials, while the effective rate is the actual percentage you pay after all fees are included. You calculate the effective rate by dividing your total monthly fees by your total sales volume and multiplying by 100. This metric is the only objective way to compare providers because it accounts for fixed costs, monthly charges, and per-transaction fees that the headline rate ignores.

How often should I audit my payment gateway fees?

You should audit your payment gateway fees every three to six months to ensure your pricing model still aligns with your transaction volume. As your business scales, a model that worked for a startup might become a significant financial drain. Regular audits allow you to identify redundant "junk" fees and ensure you're benefiting from any recent industry rate reductions or regulatory shifts that impact your bottom line.

Are there specific UAE regulations that affect payment gateway costs?

Yes, merchants in the UAE must operate within the Central Bank of the UAE (CBUAE) Retail Payment Services and Card Schemes Regulation. This framework governs how payment service providers manage transactions and security protocols within the region. These regulations impact your total cost by mandating specific compliance standards and reporting requirements. Adhering to these local frameworks ensures operational stability and protects your business from potential regulatory fines.

Can I negotiate my payment processing fees with my current provider?

You can negotiate the processor's markup even though interchange and assessment fees are non-negotiable. Processors are often willing to lower their percentage or fixed per-transaction fees to retain high-volume clients with consistent processing histories. When calculating the total cost of a payment gateway, use your historical effective rate data as leverage to show your value as a long-term partner during these negotiations.

What is a 'rolling reserve' and how does it affect my total cost?

A rolling reserve is a percentage of your daily sales held by the processor for a set period to cover potential chargebacks or fraud risks. While it isn't a direct fee, it impacts your total cost by restricting your working capital and operational liquidity. High-risk businesses typically face larger reserves. This withholding of funds acts as an opportunity cost that can hinder your ability to reinvest and grow your business.

Is a flat-rate pricing model always more expensive than interchange-plus?

Flat-rate pricing is not always more expensive, but it often becomes less efficient as your transaction volume grows. For micro-merchants with low ticket sizes, the simplicity and lack of monthly fees might be more cost-effective. However, larger businesses usually find that interchange-plus pricing offers lower costs by passing through wholesale rates for debit and standard consumer cards. Choosing the wrong model for your scale can lead to thousands in unnecessary expenses.

How do cross-border fees impact my total cost if I sell internationally?

Cross-border fees significantly increase your total cost through international processing surcharges and currency conversion (FX) markups. These costs are often hidden within the exchange rate provided at the time of settlement rather than appearing as a clear line item. If you sell internationally, calculating the total cost of a payment gateway must include an analysis of how these surcharges impact your margins across different geographic regions and currencies.

What hidden fees should I look for on my merchant statement?

Look for statement fees, PCI compliance charges, batch settlement fees, and monthly minimum processing requirements. These are often categorized as administrative costs and can vary widely between different providers. Identifying these specific line items on your merchant statement is the first step toward removing redundant services. Auditing these fees ensures your infrastructure remains lean and your payment setup is optimized for maximum profitability.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.