Card Payment Machine Guide: Selecting the Right Solution for Your UAE Business in 2026

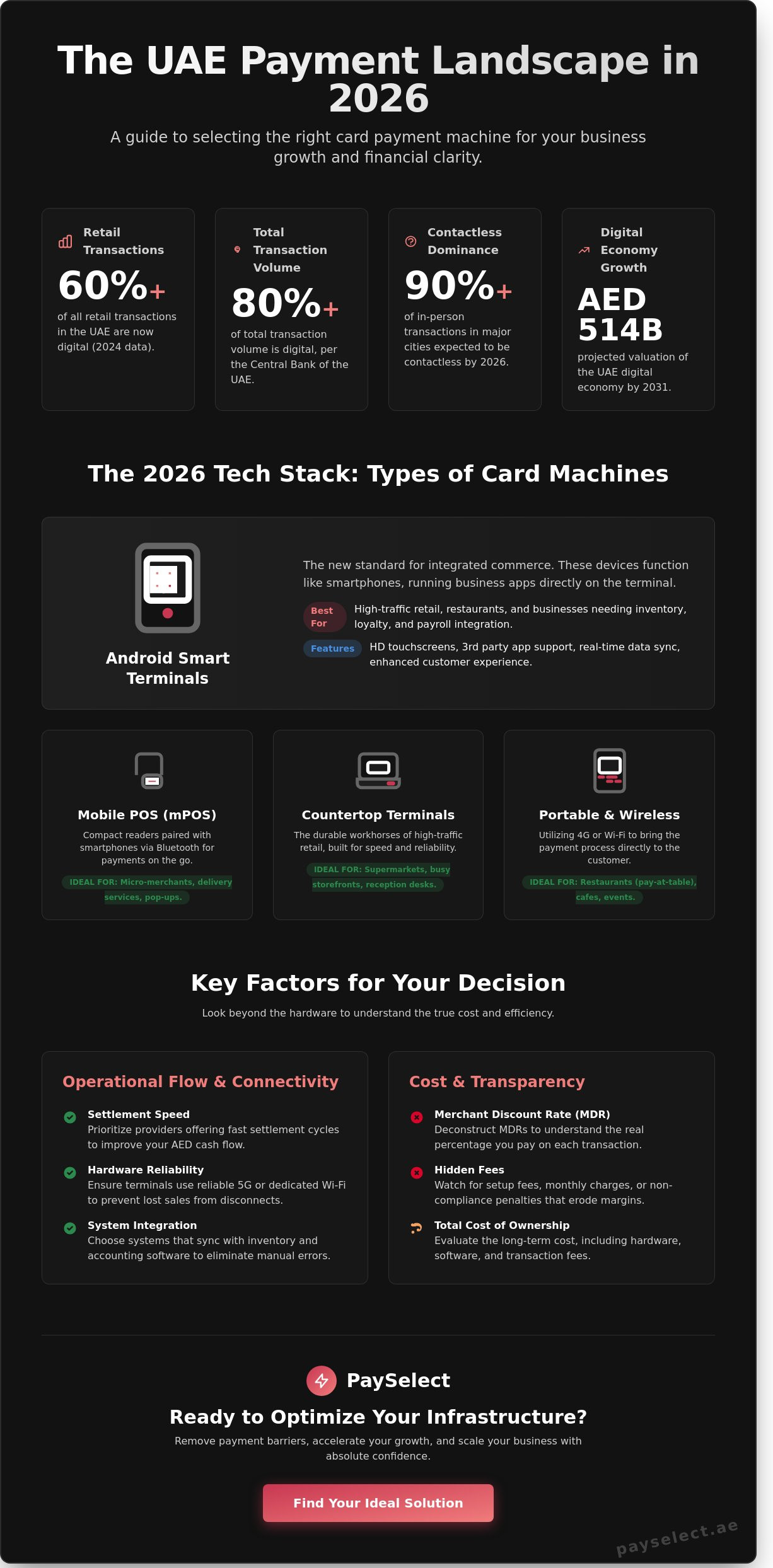

Your choice of a card payment machine in 2026 will either be a silent partner in your growth or a constant drain on your bottom line. Since digital payments now account for over 60 percent of retail transactions in the UAE according to 2024 industry data, relying on hardware that disconnects or settlement cycles that delay your AED access is no longer sustainable. You've probably noticed how unpredictable merchant discount rates and hidden fees can erode your margins before you've even cleared your daily overhead. It's a challenge that every modern business owner in the Emirates faces as they strive for financial clarity.

This article provides the roadmap you need to secure a cost-effective, seamless payment setup that prioritizes your cash flow. You'll discover how to compare different providers based on their settlement speed, hardware reliability, and reporting capabilities. We'll break down the total cost of ownership so you can make an informed decision that connects your storefront to your digital headquarters. At PaySelect, we focus on removing these barriers by offering tools that streamline operations, accelerate growth, and scale your business with absolute confidence.

Key Takeaways

• Master the transition from traditional hardware to integrated Android-based terminals that drive business efficiency across the UAE.

• Identify the ideal tech stack for your scale, whether you require mobile flexibility for micro-transactions or robust smart POS systems.

• Deconstruct complex fee structures and MDR rates to select a cost-effective card payment machine that maximizes your AED revenue.

• Optimize your operational flow by synchronizing physical and online sales channels for a truly borderless customer experience.

• Streamline your provider search using independent assessment tools designed to match your specific industry needs with the right financial infrastructure.

What is a Card Payment Machine in the 2026 UAE Market?

In 2026, a card payment machine is much more than a tool for swiping plastic. It's a sophisticated hardware device that facilitates secure electronic fund transfers across credit, debit, and digital wallets. According to the Central Bank of the UAE, digital payments now represent over 80% of total transaction volume in the country. This shift has turned the humble terminal into a critical engine for business growth and financial security. It bridges the gap between your inventory and your bank account, ensuring every sale is captured with precision.

The evolution from basic swipe hardware to integrated smart POS terminals has redefined the retail experience. Modern machines leverage high-level encryption to meet the strict regulatory standards enforced by the Central Bank of the UAE. Understanding What is a Payment Terminal? helps business owners appreciate how these devices protect both the merchant and the consumer from fraud. Adopting current technology is essential for maintaining a professional image in the B2B and B2C sectors, as customers expect seamless interactions at every touchpoint. In the UAE's competitive market, a slow or unreliable terminal can lead to lost revenue and a damaged reputation.

The Shift from Plastic to Digital Wallets

Contactless payments have become the national standard. UAE consumers lead the region in digital wallet adoption, with a heavy reliance on Apple Pay, Google Pay, and local payment schemes. NFC technology stands as the primary contactless standard for 2026 commerce, allowing for near-instant transaction approvals. Modern machines prioritize these methods to reduce friction and eliminate the need for physical card handling. This transition speeds up the checkout process and aligns your business with the preferences of a tech-savvy population. By 2026, over 90% of in-person transactions in Dubai and Abu Dhabi are expected to be contactless.

Standalone vs. Integrated Systems

Choosing the right hardware depends on your specific operational needs. Standalone terminals offer high mobility and simplicity, making them ideal for delivery services or small boutiques. Integrated systems connect your card payment machine directly to inventory management and accounting software. This integration removes manual entry errors and provides real-time data for better decision-making. Reliability is non-negotiable, so these systems utilize 5G or dedicated Wi-Fi bands to ensure always-on connectivity. For those ready to upgrade their infrastructure, exploring specialized pos machines can streamline your entire payment workflow. This setup empowers entrepreneurs to focus on scaling their brand while the technology handles the heavy lifting of financial reconciliation.

The 2026 Tech Stack: Types of Card Machines Available

The UAE digital economy is accelerating toward a AED 514 billion valuation by 2031. To capture this growth, your hardware must be as agile as your strategy. A modern card payment machine is no longer a static tool; it's a data-rich portal that streamlines operations and scales with your ambition. Selecting the right hardware depends on your transaction volume, mobility needs, and the level of integration your backend requires.

Android-based POS

These systems represent the new standard. They function like smartphones, allowing you to run inventory, payroll, and loyalty apps directly on the device.

Mobile POS (mPOS)

These compact readers pair with smartphones via Bluetooth. They're ideal for the 67,000 new companies that joined the Dubai Chamber of Commerce in 2023, providing a low-cost entry point for micro-merchants.

Countertop Terminals

These are the workhorses of high-traffic retail. Built for durability, they handle hundreds of taps and swipes daily without lag.

Portable and Wireless Terminals

Utilizing 4G or Wi-Fi, these units are essential for table-side service in the UAE's thriving F&B sector. They ensure the payment process stays within the customer's sight, enhancing security and trust.

Android Smart Terminals

Android smart terminals transform the checkout experience into a strategic touchpoint. These devices feature large, high-definition touchscreens that improve accuracy for staff and provide a premium feel for customers. By running third-party apps, you can track customer preferences or manage warehouse stock in real time. For a comprehensive look at the latest hardware specifications, you can explore various POS machines designed for the local market. This integration removes the friction of manual data entry and reduces human error by 30% in busy environments.

The Rise of SoftPOS Technology

SoftPOS technology is disrupting the traditional hardware model by turning any NFC-enabled smartphone into a card payment machine. This software-only solution is perfect for delivery fleets or boutique consultants who prioritize portability. While convenient, security remains the primary focus. These solutions must adhere to PCI CPoC standards to protect sensitive data on consumer-grade devices. Looking ahead, we expect a surge in biometric authentication. Facial recognition and fingerprint scanning at the point of sale will likely become standard by 2026, offering a frictionless "pay-by-face" experience that aligns with the UAE's vision for a paperless, high-tech society. If you want to stay ahead of these trends, you can optimize your payment infrastructure with a partner that understands the local landscape.

Navigating the Cost Landscape: Fees and Hidden Charges

Selecting a card payment machine in the UAE involves more than comparing hardware aesthetics. Your choice directly dictates your profit margins. Every transaction triggers a Merchant Discount Rate (MDR), which is the percentage fee charged by your provider. These rates aren't static. In the local market, domestic debit transactions, particularly those processed via the Jaywan scheme, typically carry lower fees than international credit cards. You'll find that premium rewards cards often command the highest MDR due to the high interchange fees associated with their benefits.

Hardware acquisition follows two primary paths: upfront purchase or monthly rental. Buying a terminal outright can cost anywhere from AED 1,000 to AED 2,500 per unit. This removes recurring hardware debt but adds immediate pressure on your capital. Conversely, rental models often range between AED 50 and AED 150 per month. While rentals lower the barrier to entry, they can become more expensive over a three year period. Businesses must calculate the total cost of ownership before committing to a long term contract.

Transaction Fee Structures

Providers generally offer flat-rate pricing or interchange-plus models. Flat-rate pricing provides simplicity with a single percentage for all cards, but it often masks the lower costs of local debit transactions. Interchange-plus is more transparent, passing the direct cost from the card network to you with a fixed markup. International card fees are a critical factor for UAE businesses in the tourism or luxury sectors. These transactions often incur an additional 1% to 2% cross-border fee. MDR is often negotiable based on annual transaction volume, especially for businesses processing over AED 1,000,000 annually.

Hidden Costs to Watch For

The fine print often contains "zombie" fees that erode your revenue. Minimum monthly volume penalties are common; if your sales drop below a specific threshold, like AED 10,000, you might face a flat penalty of AED 200. PCI compliance charges are another recurring expense that many entrepreneurs overlook during the initial setup. You should also account for operational consumables including thermal paper rolls, SIM card data plans for mobile units, and occasional software maintenance updates. PaySelect helps businesses identify these inefficiencies by streamlining the setup process and ensuring fee structures remain transparent.

Settlement times significantly impact your liquidity. While some providers offer T+1 (next day) settlement, others may hold funds for T+3 or longer. In a fast-moving economy like Dubai or Abu Dhabi, delayed access to cash can hinder your ability to restock inventory or meet payroll. Independent auditing of your monthly statements is the only way to ensure you aren't overpaying. Discrepancies often hide in complex reporting, making a professional review essential for optimizing your card payment machine costs and maximizing your bottom line.

Selecting the Ideal Solution for Your Business Model

Every business operates on its own rhythm. Your choice of a card payment machine must reflect your specific environment, whether you manage a high-traffic retail outlet, a mobile service, or a luxury hospitality venue. Selecting the wrong hardware leads to friction, slow queues, and lost revenue. You need a solution that empowers your staff and delights your customers. Efficiency isn't just a goal; it's a requirement for scaling in the UAE's competitive market.

Speed of service and reliability are paramount. In a region where downtime can cost a merchant thousands of AED per hour, technical support must be immediate. Top-tier providers offer hardware replacement within 4 to 24 hours. This ensures your operations remain seamless. Additionally, with the UAE attracting a substantial volume of international visitors annually, multi-currency support is no longer optional. It's a strategic advantage that allows tourists and international clients to pay in their home currency while you settle in AED.

Matching Hardware to Industry Needs

Different sectors demand specific functional advantages. A device that works for a boutique might fail in a fast-paced restaurant. Consider these industry-specific requirements:

Hospitality

You need long wireless range for table-side service, the ability to split bills easily, and intuitive tipping interfaces.

Retail

Success depends on speed. Look for hardware that integrates barcode scanning and provides real-time inventory synchronization.

Service Providers

Portability is key. Lightweight, 4G-enabled devices allow you to accept payments anywhere in the Emirates.

Businesses that bridge the gap between physical stores and digital storefronts should explore integrated payment gateways to ensure all transaction data flows into one central hub.

The Omni-channel Strategy

Modern commerce is borderless and fluid. Your physical card payment machine and your website shouldn't operate in silos. Using the same backend data provider for both channels simplifies accounting, optimizes stock management, and provides a unified view of your customer's behavior. This structural clarity allows you to make data-driven decisions that accelerate growth.

Expansion often brings complexity, especially when moving into other regional or international markets. Managing cross-border payments requires a partner who understands diverse local regulations and settlement nuances. According to the 2023 Visa Stay Secure study, 65% of UAE consumers prefer digital payments over cash, a trend that is mirrored across the wider region. If you're looking to scale beyond national borders, specialized cross-border payments solutions can remove traditional barriers to entry and streamline your international revenue streams.

Ready to optimize your payment infrastructure and empower your business growth? Explore PaySelect POS solutions

Optimizing Your Infrastructure with PaySelect

PaySelect functions as a strategic bridge between your business and the complex financial landscape of the UAE. Selecting a card payment machine shouldn't involve guesswork or trial and error. We provide the technical clarity and industrial insight needed to scale your operations without friction. Our "Take the Test" tool is designed specifically for this purpose. It analyzes your monthly transaction volume and industry sector to match you with the most compatible provider from our network. For enterprise-level operations, we offer specialized consulting services that include comprehensive payment audits. These audits identify hidden inefficiencies in your current setup, often uncovering opportunities to reduce operational overhead by 15% to 22% through smarter routing and fee optimization. We remove the technical and financial barriers that stall growth, empowering you to focus entirely on your core business goals.

Independent Advisory vs. Direct Sales

Direct sales teams are naturally incentivized to promote their own products, regardless of whether they fit your specific needs. PaySelect operates as an independent advisor, offering an unbiased comparison that highlights the unique strengths of different providers side-by-side. This transparency saves you dozens of hours in the procurement process and prevents costly long-term mistakes. A major factor we evaluate is the settlement cycle. While standard providers might offer T+3 cycles, certain industries require the liquidity of T+1 settlements to maintain healthy cash flow. We help you identify which providers offer the most efficient cycles for your specific trade license activity, ensuring your capital is never locked away longer than necessary.

Getting Started with Your Selection

Efficiency starts with preparation. To secure the most competitive rates for your card payment machine, you'll need to have your documentation ready for the application process. Most UAE financial institutions require a valid Trade License, passport copies of all shareholders, and at least six months of corporate bank statements. Once these are ready, you can use the PaySelect platform to request bespoke quotes that reflect your actual business scale rather than generic retail pricing. Before you commit to a long-term merchant agreement, use this final checklist to protect your interests:

• Confirm if the hardware rental fee includes 24/7 technical on-site support.

• Verify the exact percentage of the "interchange fee" versus the provider's markup.

• Check for any monthly minimum volume requirements that could trigger penalties.

• Ensure the device supports the latest security protocols and local payment schemes like Mercury.

Our goal is to make the transition to new hardware as seamless as possible. By leveraging our platform, you gain access to a curated selection of pos-machines that are already vetted for the UAE market. This structured approach ensures you aren't just buying a tool, but rather investing in a scalable piece of financial infrastructure that grows alongside your company.

Future-Proof Your UAE Payment Infrastructure

The UAE payment landscape is shifting rapidly. According to the UAE Central Bank's 2023 Digital Transformation Strategy, the push toward a cashless economy is accelerating every month. Success in 2026 requires more than just hardware; it demands a strategic alignment between your business model and your digital infrastructure. You'll need to balance transaction speed, fee transparency, and technical reliability to maintain a competitive edge in the local market.

Selecting the right card payment machine is a critical decision that impacts your bottom line and customer experience. PaySelect eliminates the guesswork by providing independent and unbiased comparisons of the market's leading solutions. We offer expert consulting for payment cost optimization, ensuring you don't lose revenue to hidden charges or inefficient settlement cycles. Our platform is already trusted by SMEs and enterprises across the Emirates to streamline their financial operations and accelerate growth.

Don't let complex fee structures or technical barriers slow your progress. Take control of your processing today. Take the Test to find the perfect card payment machine for your business and start scaling with confidence.

Frequently Asked Questions

What documents are required to get a card payment machine in the UAE?

It's essential to provide a valid UAE Trade License, owner passport copies with Emirates IDs, and recent corporate bank statements to secure a card payment machine. Statistics show 90 percent of providers require a 3 month history of business activity to verify your application and assess risk. PaySelect streamlines this document collection process to remove traditional barriers. We empower you to focus on growth while we handle the complex compliance checks required by local regulators.

How long does it typically take to get a card machine activated?

Activation typically takes between 3 and 7 business days from the moment you submit your final documents to a provider. Approximately 95 percent of successful applications are configured and delivered within this one week window to locations in Dubai or Abu Dhabi. PaySelect accelerates this cycle by integrating directly with top tier providers. Our goal is to ensure your business doesn't wait to start accepting payments so you can maintain your commercial momentum and cash flow.

Can I use a card machine without a traditional bank account?

It's mandatory to have a registered UAE business bank account for funds settlement because 100 percent of standard terminals require a local IBAN. Every transaction processed must have a verified destination for the AED deposits to ensure legal compliance with central bank regulations. PaySelect helps bridge this gap by offering expert advice on account integration. We focus on creating a seamless flow from the point of sale to your corporate treasury for maximum efficiency.

What is the average transaction fee for credit cards in the national market?

Transaction fees in the UAE typically range from 1.5 percent to 2.5 percent for local credit cards. International cards or premium rewards cards often carry higher rates reaching up to 3.5 percent per swipe depending on the provider and the issuing bank. PaySelect helps you analyze these costs to find the most efficient path for your revenue. We provide the transparency you need so you don't overpay, allowing you to optimize your margins and scale effectively.

Do card payment machines require a constant internet connection?

Every modern card payment machine requires a stable internet connection via Wi-Fi, a 4G SIM card, or an Ethernet cable to function. It's impossible for 100 percent of terminals to authorize transactions with the issuing bank in real time without a live connection. PaySelect ensures your hardware remains connected to a global infrastructure. This reliability prevents lost sales and keeps your checkout process moving at a fast pace for every customer you serve in your shop.

Is it possible to accept international cards on a local POS terminal?

It's entirely possible to accept international cards from major networks like Visa, Mastercard, and American Express on local POS terminals. This allows you to serve 100 percent of your international clientele while settling the final amount in AED directly into your local account. PaySelect empowers businesses to achieve a global reach without changing their local hardware setup. We turn your terminal into a strategic tool for borderless commerce and rapid expansion in the market.

What happens if my card machine hardware breaks or malfunctions?

Don't worry if your hardware fails; you should contact your provider immediately for a replacement or a remote software fix. Approximately 90 percent of service level agreements in the UAE guarantee a response within 24 to 48 hours to minimize your downtime and lost revenue. PaySelect acts as your rock-solid partner during these technical hurdles. We prioritize your business continuity to ensure you never miss a critical customer transaction due to equipment issues or connectivity problems.

How do I switch payment providers if I am unhappy with my current fees?

It's easy to switch providers by reviewing your existing contract for exit fees and then applying for a new merchant account. Once your new terminal is active, you can cancel the old service to avoid any gaps in your ability to take payments. PaySelect simplifies this transition by identifying the best fee structures for your specific transaction volume. We remove the friction of moving between financial partners to help you scale your business faster while reducing overhead.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.