What if the lowest advertised percentage is actually costing your business thousands in hidden maintenance fees? Most merchants find that opaque fee structures from traditional banks and unexpected integration costs quickly erode their profit margins. Finding a reliable credit card processing fees uae comparison often feels impossible when every provider uses different terminology and hidden surcharges.

You're likely frustrated by the difficulty of comparing local gateways against international providers while trying to stay compliant with the latest Federal Decree-Law No. 6 of 2025. This guide empowers you to master the complexities of merchant discount rates and hidden transaction costs to optimize your business margins. We provide a clear framework to compare different fee models, identify immediate cost-saving opportunities, and view a shortlist of provider types that match your specific volume. You'll learn how to transform your payment infrastructure into a strategic tool for business expansion and operational efficiency.

Key Takeaways

• Identify how the Merchant Discount Rate (MDR) impacts your revenue and navigate the complex ecosystem of acquirers, networks, and gateways.

• Evaluate the trade-offs between flat-rate and interchange-plus pricing models through a detailed credit card processing fees uae comparison to find your ideal match.

• Spot hidden operational expenses, such as FX markups and payout fees, that can quietly erode your business margins.

• Leverage PaySelect’s comparison tools and infrastructure consulting to match your business with the most efficient payment solutions.

• Build a transparent framework to compare providers and identify cost-saving opportunities that align with your specific transaction volume.

Understanding Credit Card Processing Fees in the UAE

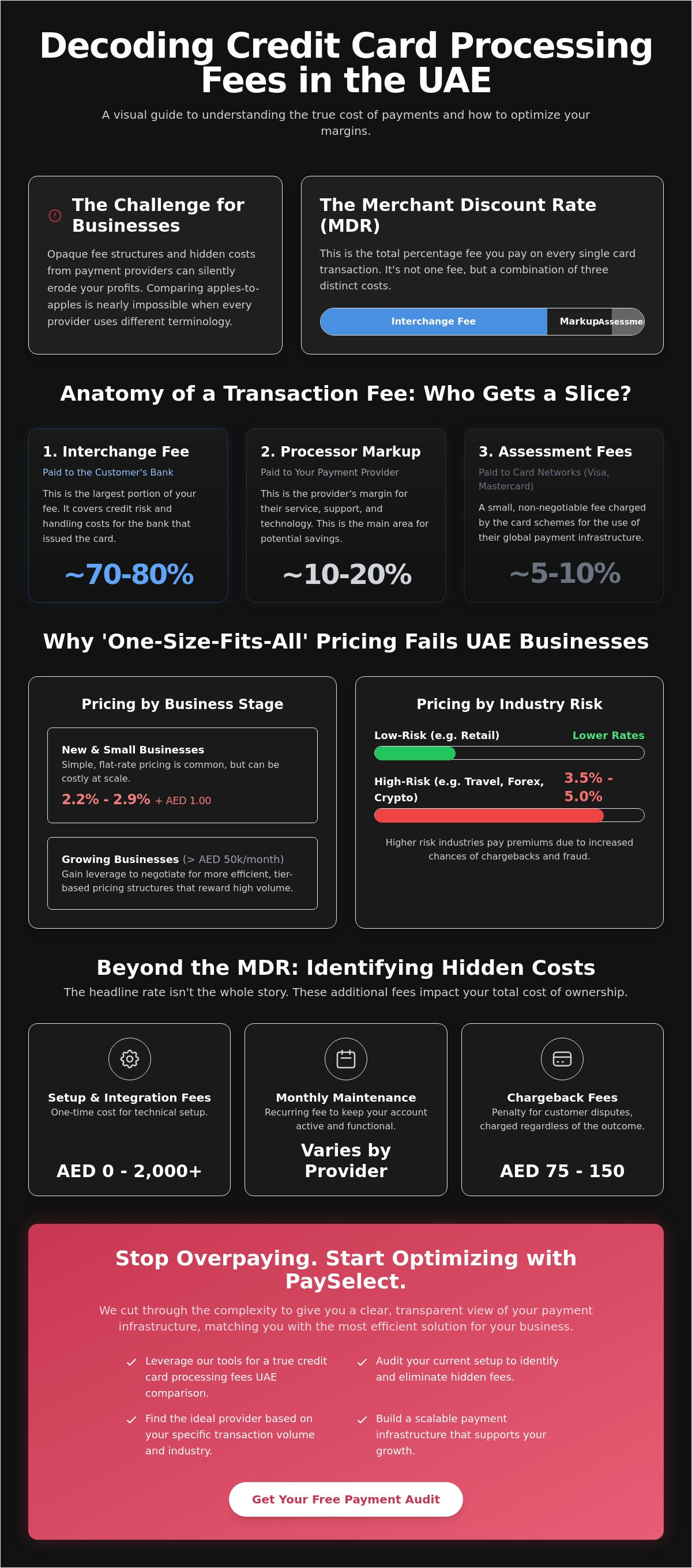

The Merchant Discount Rate (MDR) is the total percentage a business pays on every card transaction. In the UAE, this isn't just a cost of doing business; it's a strategic variable that directly impacts your bottom line. As Dubai targets a 90% cashless transaction rate by 2026, conducting a thorough credit card processing fees uae comparison is vital for maintaining healthy margins and operational agility.

The fee ecosystem relies on three core pillars. The acquirer settles the funds into your bank account; the network provides the global communication rails; and the gateway acts as the technical bridge for the data. Each player takes a slice of the transaction. UAE processing fees often differ from European or North American markets because of local regulatory frameworks and international settlement complexities. While the Federal Decree-Law No. 6 of 2025 is bringing stricter oversight and transparency to the region, the market remains unique in its pricing dynamics and regional requirements.

The Components of a Transaction Fee

Every digital payment involves three distinct cost layers that determine your final expense:

• Interchange fee: This is the largest portion of the fee, paid to the bank that issued the customer's card. It covers the costs of credit risk and transaction handling.

Assessment fees

These are non-negotiable costs paid directly to card networks like Visa and Mastercard for the use of their global payment systems.

Processor markup

This is the margin added by your payment provider. It covers their operational costs, customer support, and profit. This is the primary area where businesses can find savings through negotiation or comparison.

Why One-Size-Fits-All Pricing Fails

Generic pricing models often penalize growing businesses. New entities typically encounter rates between 2.2% and 2.9% plus a fixed AED 1.00 fee per transaction. While this offers simplicity for startups, it lacks the efficiency needed for scale. Once a merchant exceeds AED 50,000 in monthly volume, they gain the leverage to move toward more competitive, tier-based pricing structures that favor high-performance operations.

Industry risk profiles also create significant price gaps. High-risk sectors like travel, forex, or crypto often pay premiums of 3.5% to 5%, while low-risk retail enjoys much lower rates. Early-stage businesses require different payment gateways than established enterprises. Startups prioritize low setup fees and speed; enterprises focus on deep system connectivity and cost optimization. PaySelect solves the problem of opaque fee structures by offering a payment pricing comparison tool. This allows you to audit your current infrastructure and find a provider that matches your specific transaction profile, ensuring you don't overpay for services your business doesn't need.

The Anatomy of Merchant Service Charges

A comprehensive credit card processing fees uae comparison requires looking beyond the headline percentage. Total cost of ownership involves a mix of one-time, recurring, and event-driven expenses that impact your liquidity. Transparency is often lacking in traditional bank agreements; identifying these layers early prevents operational friction as your business scales.

Setup and integration fees represent your initial investment. In the UAE, these costs range from AED 0 to over AED 2,000 depending on the provider's technical complexity. Monthly maintenance fees are another standard; they ensure your account remains active and functional. Transaction-based fees are the most frequent cost. New businesses typically encounter rates between 2.2% and 2.9% plus a fixed amount of approximately AED 1.00 per sale. These small amounts compound into significant monthly overheads.

Customer disputes introduce unexpected financial strain. Chargeback fees in the local market generally fall between AED 75 and AED 150 per dispute. These are charged regardless of whether you win the case. A payment pricing comparison audit helps you identify where these small costs are leaking revenue and eroding your hard-earned margins.

Fixed vs. Variable Costs

Predictable costs like monthly subscriptions stay constant regardless of your performance. Variable costs scale directly with your success; these include transaction percentages and fixed per-item charges. Some providers enforce minimum monthly volume requirements, which can penalize businesses during slow seasons. Your effective rate is the total fees paid divided by your total sales volume. Monitoring this single metric ensures your payment infrastructure remains efficient as you grow.

Security and Compliance Fees

Maintaining PCI-DSS compliance is a fundamental requirement for any merchant operating in the UAE. Many providers bundle these compliance costs into their maintenance fees, while others charge them as annual assessments. Fraud prevention tools and tokenization services for recurring billing often carry additional surcharges. These technical utilities are strategic investments; they reduce the likelihood of expensive chargebacks and enhance the checkout experience for your customers. High-quality security layers act as a catalyst for growth by building consumer trust in a digital-first economy.

Comparing Pricing Models: Flat-Rate vs. Interchange-Plus

Selecting a pricing structure is a strategic decision that dictates your long-term operational efficiency. A standard credit card processing fees uae comparison usually highlights two primary paths: the simplicity of flat rates or the transparency of interchange-plus. While startups often prioritize predictability, established enterprises require a granular view of their transaction costs to protect their margins. Choosing the wrong model can lead to unnecessary overhead that scales alongside your success.

Tiered pricing is a common pitfall in the UAE market. Many traditional providers categorize transactions into "qualified," "mid-qualified," or "non-qualified" buckets. This structure is often opaque. It frequently pushes rewards cards or corporate cards into the most expensive "non-qualified" tier without clear justification. To evaluate your current setup, calculate your effective rate by dividing your total monthly fees by your total sales volume. This single figure reveals the true cost of your payment infrastructure.

When to Choose Flat-Rate Pricing

Flat-rate pricing is ideal for businesses with low monthly transaction volumes or those just entering the market. It offers absolute predictability; you know exactly what every AED 100 sale will cost regardless of the card type used. This model eliminates the need for complex reconciliations and protects you from the volatility of varying interchange rates. For early-stage ventures, the benefit of simplicity and ease of accounting often outweighs the slightly higher percentage compared to more complex models.

The Advantage of Interchange-Plus for Scaling

Interchange-plus, also known as pass-through pricing, provides total visibility into the actual costs charged by card networks. You pay the direct cost of the transaction plus a small, fixed markup to the processor. This model is highly efficient for high-volume merchants because it allows them to benefit from lower fees on domestic debit cards. In the UAE, interchange caps for domestic consumer debit cards are set at 0.75% for in-person sales and 1.00% for online transactions.

A data-driven credit card processing fees uae comparison shows that interchange-plus is the natural fit for businesses with complex cross-border payment needs. It ensures you aren't paying a generic high rate for transactions that should be processed at a lower domestic cost. PaySelect helps you navigate these models by providing a payment pricing comparison that identifies which structure aligns with your current volume and growth trajectory. This independent advisory ensures your payment setup acts as a catalyst for expansion rather than a financial barrier.

Beyond the MDR: Identifying Hidden Operational Costs

Focusing solely on the headline percentage is a common strategic mistake. A realistic credit card processing fees uae comparison requires auditing the secondary costs that drain your liquidity and slow your momentum. Payout and settlement fees often go unnoticed; these represent the cost of moving funds from your processor to your local bank account. Contract lock-ins and early termination fees also create significant operational barriers. These exit costs can trap businesses in inefficient structures, preventing them from migrating to more competitive solutions as they scale.

Physical retail introduces specific hardware considerations that impact your initial capital expenditure. Choosing between POS machine rentals or outright purchases depends on your long-term cash flow strategy. Rentals offer low upfront costs but higher monthly overhead; purchasing equipment provides asset ownership and removes recurring rental burdens. Using a POS system selection tool helps you evaluate these hardware models alongside your transaction profiles to find the most cost-effective balance for your storefront.

The Cost of International Sales

Cross-border transactions often double your processing expenses without warning. While domestic rates are stable, international card surcharges typically add between 1.5% and 3.9% to your base rate. Regional GCC cards sometimes carry different fee weights than cards issued in Europe or North America. Implementing multi-currency settlement strategies allows you to receive funds in the customer's native currency. This helps you avoid aggressive FX markups, preserve your international margins, and provide a frictionless experience for global shoppers.

Integration and Technical Support Fees

Technical connectivity isn't always included in the base price. Some providers charge for API access, specialized developer support, or specific shopping cart plugins for e-commerce platforms. These hidden technical fees can turn a "low-cost" gateway into an expensive infrastructure burden over time. Investing in a provider with localized technical support ensures fast resolution times, system reliability, and smooth transitions during updates. High-quality support acts as a strategic tool for business transformation rather than just a service cost.

To uncover these hidden drains on your revenue and streamline your international growth, use our Cross-border Payment Solution Matching tool to find a partner that matches your global ambitions.

How to Optimize Your Payment Infrastructure with PaySelect

Managing the financial intricacies of a growing business requires more than just a basic merchant account. It demands a strategic approach to infrastructure. PaySelect functions as an independent facilitator, providing the tools necessary to perform a comprehensive credit card processing fees uae comparison without the bias of traditional institutional providers. By moving away from a reactive "plug-and-play" mindset, you can transform your payment stack into a high-performance engine for business expansion.

Our "Take the Test" tool is designed to simplify the selection process by matching your specific transaction profile with the most efficient providers in the market. Whether you are evaluating POS machines for retail or digital gateways for e-commerce, our platform allows for side-by-side comparisons of fee structures, integration requirements, and technical capabilities. For larger organizations, our independent advisory services provide deep-dive insights into enterprise-scale fee optimization, ensuring that high-volume merchants capture every possible saving.

Data-driven decisions lead to measurable results. One national merchant recently utilized a Payment Cost Optimization Audit to identify overlapping service fees and misaligned pricing tiers. By restructuring their provider mix based on these objective insights, they achieved a verified 15% reduction in their total annual processing costs. This level of efficiency is only possible when you have total visibility into your effective rate and hidden operational surcharges.

Navigating the UAE Market with Confidence

Independence is a critical competitive advantage in a crowded fintech landscape. PaySelect simplifies the "fine print" of complex merchant agreements, highlighting the clauses that typically lead to unexpected costs or contract lock-ins. We provide a bridge between technical utility and your strategic business goals. This clarity ensures that you select a partner based on performance and transparency rather than just the lowest advertised headline rate.

Your Next Steps for Cost Reduction

Reducing your overhead begins with an honest assessment of your current infrastructure. You can leverage a credit card processing fees uae comparison to gain the data required to negotiate better rates with your existing provider or to identify a more suitable alternative. Our Payment Infrastructure Consulting team is available to help you audit your current setup and identify immediate opportunities for margin enhancement. Don't let opaque pricing models slow your momentum; take control of your financial rails today.

Ready to maximize your margins? Compare UAE payment gateway fees today and find the perfect match for your business volume.

Secure Your Strategic Advantage in the UAE Market

Mastering your transaction costs is a critical step toward scaling a profitable enterprise in the region. You now have the framework to distinguish between headline rates and the actual effective rate that impacts your daily liquidity. Identifying hidden operational drains and selecting the pricing model that aligns with your specific transaction volume removes the primary barriers to sustainable growth. This clarity allows you to focus on expansion rather than administrative friction.

Performing a regular credit card processing fees uae comparison ensures your business remains agile as regulatory frameworks evolve and the market matures toward a digital-first economy. PaySelect provides an independent and unbiased B2B comparison platform designed to help you navigate these complexities with expert advisory tailored for MENA enterprise payments. Our tools are fully optimized for the latest UAE regulatory frameworks; this ensures your infrastructure remains both compliant and cost-effective.

Take the next step in your operational evolution. Find the most cost-effective payment gateway for your business and transform your payment setup into a strategic asset for international expansion. It's time to build a leaner, more efficient foundation for your future success.

Frequently Asked Questions

What is the average credit card processing fee for merchants in the UAE?

New businesses in the UAE typically pay transaction fees ranging from 2.2% to 2.9% plus a fixed fee of approximately AED 1.00 per sale. Depending on your industry and transaction volume, the general Merchant Discount Rate (MDR) for Visa and Mastercard usually falls between 1.8% and 3.5%. High-risk sectors like travel or crypto can expect premium rates reaching up to 5%. Performing a credit card processing fees uae comparison helps you determine if your current rate aligns with these market standards.

Can I negotiate my merchant discount rate (MDR) with UAE banks?

You can negotiate your MDR once your business demonstrates consistent transaction volume and low risk profiles. Merchants with a monthly volume exceeding AED 50,000 generally have the leverage to request tier-based or volume-based pricing structures. Banks are often willing to adjust rates for established enterprises to secure long-term partnerships. Using data from a payment pricing comparison audit provides the objective evidence you need to strengthen your bargaining position during these discussions.

Are there different fees for accepting Visa vs. Mastercard in the UAE?

While Visa and Mastercard set their own specific interchange rates, most UAE processors consolidate these into a unified MDR for simplicity. The Central Bank of the UAE has mandated interchange caps for domestic consumer debit and prepaid cards at 0.75% for in-person sales and 1.00% for online transactions. These caps apply regardless of the network. Differences between providers usually emerge in their technical features and fraud prevention tools rather than the base network fees themselves.

What is the difference between a payment gateway fee and an acquirer fee?

A payment gateway fee is a technical charge for the secure transmission of transaction data, while an acquirer fee covers the financial processing and settlement of funds. The gateway acts as the digital bridge connecting your storefront to the banking network. The acquirer is the financial institution that assumes the risk and deposits the money into your account. Some providers bundle these costs into a single rate, while others itemize them based on your infrastructure requirements.

How much does a POS machine cost for a business in the UAE?

POS machine costs depend on whether you choose a rental model or an outright purchase of the hardware. Rental options provide low upfront costs and are ideal for preserving cash flow, while purchasing the equipment removes recurring monthly rental burdens. Setup fees for these physical systems can range from AED 0 to over AED 2,000. Selecting the right model requires balancing your initial capital expenditure against the long-term operational costs of your retail environment.

What are the hidden fees I should look for in a merchant agreement?

Hidden costs frequently include currency conversion (FX) markups, payout fees for fund transfers, and chargeback dispute fees. Chargeback disputes in the UAE typically cost between AED 75 and AED 150 per instance regardless of the outcome. You should also watch for early termination fees and monthly maintenance surcharges that can quietly inflate your effective rate. A detailed credit card processing fees uae comparison is the most effective way to identify these non-transparent expenses before they impact your margins.

Do I pay higher fees for international credit cards?

International card transactions usually carry an additional surcharge ranging from 1.5% to 3.9% on top of your standard domestic rate. These higher fees cover the increased technical complexity and cross-border risk associated with global settlements. If a significant portion of your revenue comes from international customers, implementing multi-currency settlement strategies is essential. Finding a partner through cross-border payment solution matching ensures you aren't overpaying for your global sales reach.

How long does it take for funds to be settled into my UAE bank account?

Funds are typically settled into your local bank account within T+1 to T+3 business days. The exact timeline depends on your provider's internal protocols, your industry risk category, and whether the transactions were domestic or international. High-risk sectors or businesses using international gateways may experience slightly longer settlement windows. Efficient infrastructure ensures smooth transitions of capital, which is vital for maintaining the liquidity and operational momentum needed for business expansion.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.