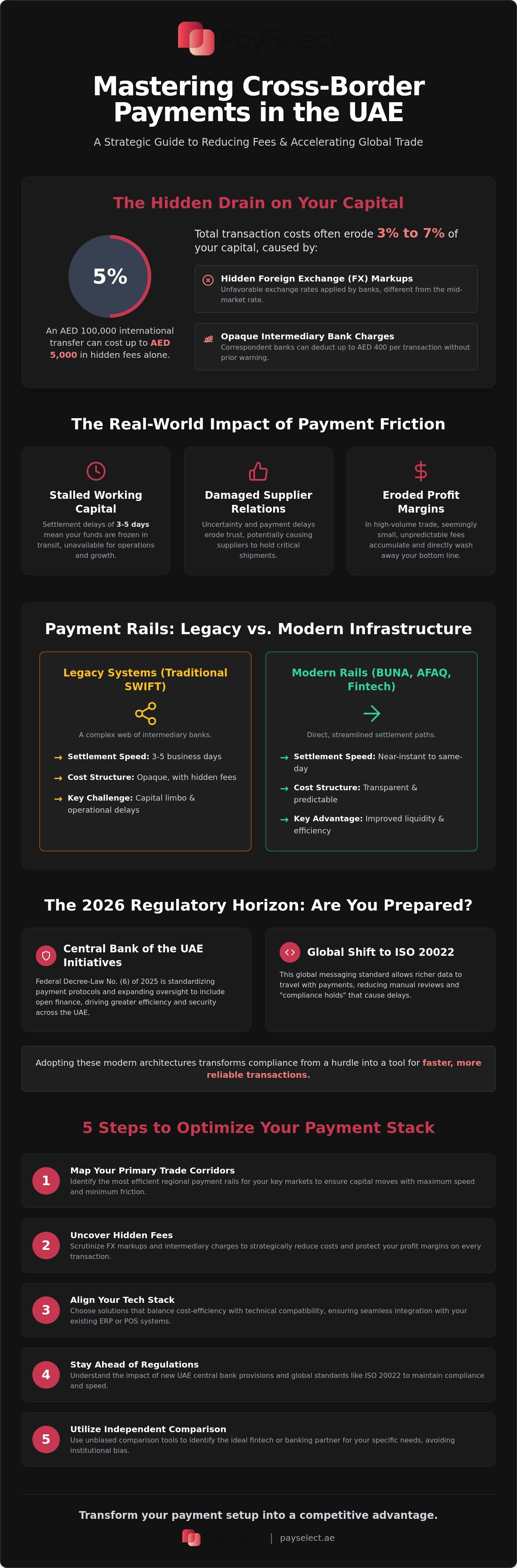

A single AED 100,000 international transfer can drain your business of AED 5,000 in hidden foreign exchange markups alone. For many enterprises, the urgent need to reduce cross border transaction fees uae is often blocked by opaque intermediary bank charges and settlement delays that stall supplier relations. You've likely experienced the frustration of seeing capital eroded by 3% to 7% in total transaction costs while waiting days for funds to clear. It's a friction point that slows your international ambition and complicates your cash flow management.

This strategic guide empowers you to master these complexities through a comprehensive breakdown of regional payment rails and cost structures. We'll provide a clear framework for comparing fintech innovations against institutional bank solutions to ensure you achieve faster settlement cycles and transparent fee structures. You'll discover how to navigate the 2026 regulatory landscape, optimize your infrastructure, and transform your payment setup into a competitive advantage for global expansion. By the end of this breakdown, you'll have the tools to eliminate operational barriers and drive performance across every border.

Key Takeaways

• Map your primary trade corridors to the most efficient regional payment rails, ensuring your capital moves with maximum speed and minimum friction.

• Uncover hidden FX markups and intermediary charges to strategically reduce cross border transaction fees uae and protect your profit margins.

• Master a selection framework that balances technical compatibility with cost-efficiency, aligning your payment stack with your existing ERP or POS systems.

• Stay ahead of the 2026 regulatory curve by understanding the impact of new UAE central bank provisions and global messaging standards like ISO 20022.

• Utilize independent comparison tools to identify the ideal fintech or bank partner without the bias of traditional processing institutions.

Navigating the Complexities of International Payment Friction

The UAE sits at the heart of global commerce. It's currently the world’s second-largest hub for outbound remittances, reflecting its status as a premier trade gateway. Despite this, many local firms remain tethered to a legacy banking infrastructure that feels stuck in the past. Traditional correspondent banking was built for an era of slower trade. It relies on multiple intermediary institutions to move money across borders. Each "hop" in this chain introduces new costs and potential for error. If you want to reduce cross border transaction fees uae, you have to look beyond the basic transfer fee. The real cost lies in the friction of the SWIFT payment network when it’s not properly managed. This friction isn't just a cost center; it's a direct threat to your trade competitiveness.

The Operational Impact of Settlement Delays

Capital that isn't moving is capital that isn't earning. Settlement delays of three to five days can severely impact your working capital. While your funds are "in transit," they're effectively useless to your operations. Opaque fee structures make this worse. Intermediary banks can deduct up to AED 400 per transaction without warning. In high-volume trade, these small leaks become a flood that washes away your profit margins. There's also a human element to consider. Uncertainty in international vendor relations leads to broken trust. If your payment is late due to a banking delay, your supplier might hold your next shipment. Using a comparison framework for cross-border payments helps you avoid these pitfalls by matching your needs with providers that offer predictable settlement cycles.

Regulatory Evolution and Compliance Standards

Compliance is no longer just about checking boxes. It’s about operational efficiency. The Central Bank of the UAE is driving this change through Federal Decree-Law No. (6) of 2025. This law standardizes payment protocols and expands oversight to include open finance. The shift to the ISO 20022 messaging standard is equally critical. This global standard allows for more detailed data to be sent with every payment. It reduces the chance of a transaction being flagged for manual review or "compliance holds" that often delay funds. By adopting these modern architectures, businesses can reduce cross border transaction fees uae while staying fully compliant. Compliance becomes a tool for speed rather than a reason for a delay. You're moving from legacy systems to agile, data-rich payment structures that reflect the speed of the 2026 digital economy.

Understanding Modern Payment Rails: SWIFT, BUNA, and Beyond

Think of a payment rail as the digital infrastructure that carries your funds from point A to point B. Your choice of rail determines your settlement speed, the transparency of your transfer, and the final cost. To reduce cross border transaction fees uae, you must understand that not all highways are built the same. While the traditional SWIFT network remains the global standard, its modern Global Payment Innovation (gpi) enhancement has added much-needed tracking and speed. However, even with gpi, you are often still moving through a chain of correspondent banks, each taking a small cut of your capital.

Regional initiatives like BUNA and AFAQ offer a faster alternative for trade within the Arab world. BUNA, operated by the Arab Monetary Fund, facilitates cross-border payments in multiple currencies, including the UAE Dirham. AFAQ connects the real-time gross settlement systems of GCC countries. These rails allow for direct settlement between banks, bypassing the complex web of international intermediaries that often inflate costs. This alignment follows the G20 roadmap for enhancing cross-border payments, which prioritizes lower costs and higher speed for global commerce.

Legacy Systems vs. Real-Time Regional Rails

Traditional correspondent banking can leave your capital in limbo for three to five business days. In contrast, regional rails like BUNA aim for near-instant settlement. This isn't just about speed; it's about liquidity. When you settle in real-time, you eliminate the risk of currency fluctuations during the transit period. You also avoid the hidden fees often tucked away by intermediary banks. Fintech-led rails take this a step further by using proprietary networks to settle funds almost instantly, often at a fraction of the cost of a traditional wire. Finding the right balance between these options is easier when you use a dedicated cross-border payment matching tool to audit your current routes.

The Strategic Value of ISO 20022 Data

The transition to ISO 20022 is a fundamental shift in how financial data is structured. Unlike older messaging formats that were limited in character count, ISO 20022 allows for rich, structured data to accompany every payment. This means your ERP can automatically reconcile payments without manual intervention. It reduces the need for expensive amendment fees that occur when a payment is sent with insufficient details. ISO 20022 is a standardized financial messaging format that provides granular data for every transaction, significantly lowering the risk of payment rejections and manual errors. By adopting this standard, you ensure your business remains compatible with the future of global trade.

Deconstructing the Total Cost of International Transactions

Most UAE businesses focus on the visible sticker price of a wire transfer. They see a SWIFT fee ranging from AED 50 to AED 100 and assume that's the primary expense. This narrow view is a mistake. To truly reduce cross border transaction fees uae, you must account for the "all-in" cost of capital movement. Traditional banking routes often carry a total transaction cost between 3% and 7% of the total payment value. This includes the upfront fee, the foreign exchange markup, and the silent deductions made by intermediary banks along the way. Understanding these layers is the first step toward reclaiming your profit margins.

The amount you send is rarely the amount your supplier receives. This discrepancy is caused by the correspondent banking system. If your bank doesn't have a direct relationship with the receiving institution, it uses a middleman. These intermediary banks can charge "lifting fees" or correspondent commissions as high as AED 400 per transaction. These charges are often deducted from the principal amount without prior notice. When you add amendment fees for minor data errors and rejection fees for failed transfers, the total cost of ownership for a single payment stack can become unsustainable for high-growth enterprises.

Identifying Hidden FX Markups and Intermediary Fees

Foreign exchange markups represent the largest hidden cost in international trade. While specialized fintech platforms offer total costs between 0.4% and 0.8%, traditional banks often apply FX markups as high as 5% above the mid-market rate. To identify these spreads and explore competitive rates, you can visit Ellicash to see how a modern fintech app handles international transfers and global investments with transparent pricing. High-volume merchants shouldn't accept retail pricing; you have the leverage to negotiate better rates, move toward volume-based pricing, and eliminate the unpredictable lifting fees that erode your vendor trust.

The Role of Payment Cost Optimization Audits

Efficiency is born from visibility. Many organizations carry redundant steps in their payment infrastructure, paying for legacy services they no longer need. A professional payment cost optimization audit provides a deep-dive analysis of your current leaks. It identifies where you're overpaying for FX, which corridors are unnecessarily expensive, and how to shift from fixed-fee models to dynamic pricing. This audit acts as a catalyst for growth, removing operational barriers and ensuring your infrastructure is lean, fast, and ready for expansion. By refining these processes, you don't just reduce cross border transaction fees uae; you transform your entire financial operations into a strategic tool for business transformation.

Five Steps to Optimising Your Cross-Border Payment Stack

Building a resilient payment infrastructure requires more than just choosing a bank. It’s about creating a system that balances speed, cost, and technical agility. To reduce cross border transaction fees uae, you must move beyond reactive decision-making. A strategic stack allows your business to pivot between different payment rails as market conditions or regulations change. This flexibility ensures that your capital remains fluid and your supplier relationships stay strong. Follow these five steps to audit and refine your current setup for 2026.

Define your primary corridors

Identify exactly where your suppliers and customers are located. A provider that offers excellent rates to Europe might be inefficient for trade with the GCC or South Asia.

Assess technical compatibility

Ensure any new solution integrates directly with your existing ERP or POS system. Manual data entry is a primary driver of amendment fees and reconciliation errors.

Evaluate compliance and security

Verify that your partners comply with the latest Central Bank of the UAE provisions before the September 16, 2026 deadline. Security isn't just a hurdle; it’s a facilitator of trust.

Compare Total Cost of Ownership (TCO)

Look past the headline transaction rate. Factor in FX markups, intermediary "lifting" fees, and the cost of delayed liquidity.

Test for scalability

Choose a partner that can handle your projected 2026 volumes without a degradation in service speed or a sudden spike in per-transaction costs.

Corridor Mapping and Provider Specialisation

Not all providers are created equal. Some excel in regional trade by leveraging direct clearing access to systems like BUNA, while others dominate global routes through sophisticated treasury networks. If your business focuses on regional expansion, you need a partner with deep roots in the Middle Eastern regulatory environment. This specialisation allows you to bypass the traditional correspondent banking chain, which is the most effective way to reduce cross border transaction fees uae. Direct routes mean fewer middlemen, lower costs, and faster settlement. For those incorporating digital asset solutions into their regional operations, Pallapay provides a regulated framework for managing these modern payment flows.

Technical Integration and API Connectivity

The days of manual portal entries are over. Modern commerce demands API-first solutions that allow for real-time data exchange. This connectivity reduces the risk of human error and ensures that your accounting remains accurate. When you use cross-border payment solution matching, you can filter for providers that offer the specific technical fit your business requires. High-quality API integration also improves your ability to resolve exceptions quickly, as data richness allows for faster troubleshooting by customer support teams. Find your ideal payment match today to ensure your technical infrastructure is ready for the future of global trade.

Enhancing Infrastructure with Independent Advisory and Comparison

The UAE payment market is saturated with providers claiming to be the fastest and cheapest. Without an independent lens, businesses often end up with mismatched solutions that fail to reduce cross border transaction fees uae effectively. PaySelect acts as a neutral bridge between merchants and providers, offering the structural clarity needed to make informed choices. We don't process payments; we optimize how you process them. By removing operational barriers and focusing on transparency, we ensure that your infrastructure selection is based on data rather than sales pitches.

Our "Take the Test" tool provides a streamlined starting point for this transformation. It matches your specific business requirements with the right provider based on your trade corridors, technical needs, and volume projections. This matching process ensures that you aren't just choosing a service, but a strategic tool that aligns with your international ambition. It brings a sense of completeness and momentum to your financial planning, allowing you to scale with absolute confidence.

The Advantage of Unbiased Comparison Tools

Unbiased data is the foundation of a rock-solid financial strategy. When you compare payment gateways and cross-border solutions in a single, comprehensive view, you eliminate the guesswork that leads to high-end leaks. Expert guidance is essential in a digital economy that moves at breakneck speed. It ensures you don't commit to legacy systems that hinder your growth. Accessing independent comparison data allows you to identify performance gaps, evaluate technical utility, and select partners that truly understand the UAE's unique regulatory landscape.

Strategic Scaling Through Bespoke Advisory

For enterprise organizations and large-scale hotel groups, a generic solution is rarely sufficient. These entities require bespoke payment infrastructure consulting to manage complex multi-currency flows and high-frequency transactions across diverse locations. You can initiate a payment infrastructure audit today to identify where your current stack is losing speed, where you lack transparency, and where you are overpaying for capital movement. Leveraging independent advisory helps you reduce cross border transaction fees uae while enhancing system connectivity across your entire organization. PaySelect acts as a sophisticated catalyst for growth by distilling complex global infrastructures into intuitive, manageable choices for modern entrepreneurs.

For platform-based businesses and marketplaces seeking to integrate branded financial services into their ecosystem, you can visit Gemba to explore specialized banking infrastructure solutions for non-banks.

For organizations looking to build on decentralized protocols, you can visit Crypto Chief to access a unified Web3 infrastructure platform that supports developers in creating modern financial solutions.

Securing Your Global Trade Competitive Advantage

The landscape of international commerce is evolving rapidly; staying competitive in 2026 requires more than just a functional bank account. You've seen how the strategic choice of payment rails and a clear understanding of hidden FX markups can protect your capital. By auditing your infrastructure and mapping your specific trade corridors, you can effectively reduce cross border transaction fees uae and reclaim your profit margins. This isn't just about saving money; it's about building a friction-less engine for growth.

PaySelect provides the independent and unbiased advisory you need to navigate these choices without the pressure of a processor's sales pitch. Our expert-led cost optimization audits and national coverage across the UAE ensure your business is equipped with the most efficient tools for expansion. Whether you're a large-scale enterprise or a growing entrepreneur, removing operational barriers is the ultimate catalyst for your international success. Your technical utility should be a strategic asset, not a burden.

Ready to optimize your financial operations? Take the Test to find your perfect cross-border payment partner and transform your payment stack into a high-performance tool for business transformation. Your future in global commerce starts with a single, data-driven decision.

Frequently Asked Questions

How do I choose the best cross-border payment provider for my business?

Select a provider by analyzing your primary trade corridors, evaluating technical compatibility, and comparing the total cost of ownership. You should prioritize partners that offer direct clearing access to your most frequent markets and integrate seamlessly with your existing ERP. Using an independent comparison tool ensures you find a match based on data rather than marketing claims.

What are the typical fees associated with international payments in the Middle East?

International payments typically involve SWIFT initiation fees between AED 50 and AED 100, but the hidden costs are often much higher. Intermediary bank commissions can add AED 400 per transfer, while traditional foreign exchange markups can reach 5% above mid-market rates. These layered charges can drive the total cost of a transaction to between 3% and 7% of the payment value.

How long does a cross-border transaction usually take to settle?

Settlement times vary significantly depending on the payment rail used for the transaction. Traditional correspondent banking often takes three to five business days due to the multiple "hops" between institutions. Modern regional systems and specialized fintech networks aim for near-instant or same-day delivery, significantly improving your business liquidity and vendor trust.

Is it better to use a traditional bank or a fintech for international transfers?

Traditional banks offer rock-solid institutional security, while fintech platforms prioritize speed, transparency, and lower FX markups. Your decision should align with your volume requirements and the level of technical integration your ERP demands. PaySelect provides the neutral insights needed to compare these different provider types without bias.

What is BUNA and how does it affect my business payments?

BUNA is a multi-currency payment system that streamlines cross-border transfers within the Arab region and with key global partners. It reduces your reliance on complex international intermediary chains, allowing your business to settle payments in AED or other regional currencies with greater speed. This regional infrastructure is a key tool for enhancing trade efficiency across the Middle East.

Can I integrate cross-border payment solutions with my existing POS system?

Modern cross-border solutions integrate seamlessly with POS systems through robust API connectivity. This connectivity allows for automated reconciliation, reduces manual data entry errors, and ensures your financial records remain accurate across all international trade activities. Choosing a technically compatible partner is essential for maintaining a frictionless back-office operation.

How does PaySelect help me save money on my payment infrastructure?

PaySelect helps you reduce cross border transaction fees uae by offering an independent comparison of providers and bespoke infrastructure audits. We identify hidden FX markups and redundant intermediary charges to ensure you select the most cost-effective partner for your specific operations. Our platform removes operational barriers by providing the transparency traditional institutions often lack.

What compliance standards should I look for in a payment partner?

Look for partners that hold valid Central Bank of the UAE licenses and comply with the latest ISO 20022 messaging standards. Ensuring your provider meets the requirements of Federal Decree-Law No. (6) of 2025 is essential for maintaining operational continuity. These standards guarantee that your transactions are secure, data-rich, and compliant with the evolving regional regulatory landscape.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.