1. What Are Stablecoins — And Why Are They ‘Stable’?

Unlike Bitcoin or other cryptocurrencies that can fluctuate up to 5–10% in a single day, stablecoins are designed to maintain a fixed value, usually pegged 1:1 to a fiat currency such as the US Dollar.

Examples include:

- USDC (Circle)

- USDT (Tether)

- PYUSD (PayPal)

- EURC / EURe (Euro-pegged stablecoins)

These stablecoins are backed by real-world reserves held in:

- cash deposited in regulated banks

- short-term US Treasury bills

- high-quality liquid assets

Because of this reserve backing, 1 USDC = 1 USD, and does not behave like speculative assets such as BTC or ETH.

This stability makes stablecoins suitable for:

- B2B payments

- cross-border settlements

- treasury management

- liquidity operations for fintechs and PSPs

2. Traditional International Transfers: Digital… but Slow

When businesses send money across borders via banks, the behind-the-scenes process involves:

- SWIFT messages between institutions

- multiple correspondent banks

- different ledgers in different countries

- settlement delays from hours to days

- FX spreads and intermediary fees

Fintechs such as TerraPay, Verto, Wise, and Nium improve this by:

- holding prefunded local accounts in each market

- automating payouts

- offering better FX

But they still rely on:

- local banking hours

- central bank settlement systems

- the need to prefund liquidity across multiple countries

Prefunding is one of the largest operational costs for global payment companies.

3. Stablecoins: A Faster, 24/7, Globally Interoperable Rail

Stablecoins move value directly across a blockchain — allowing near-instant, low-cost transfers globally, 24/7.

Key advantages:

- real-time settlement

- low transaction cost

- no correspondent banks

- transparent audit trail

- global interoperability

Unlike fiat transfers, stablecoin transfers move the asset itself, not just a message requesting another bank to adjust balances.

4. A Major Advantage for Larger Businesses & Fintechs: No More Heavy Prefunding

This is one of the most powerful and often overlooked benefits.

Today, fintechs and PSPs need to lock capital in multiple countries to ensure instant payouts for customers. This ties up millions of dollars in liquidity that cannot be used elsewhere.

Stablecoins change this model.

How stablecoins reduce prefunding requirements:

- A payment company in UAE can hold treasury balances in USDC.

- When they need to settle funds with a partner in Kenya, India, or Europe, they can send USDC directly in seconds.

- The partner converts it locally into KES, INR, EUR — without both sides holding large prefunded balances across many markets.

This improves:

- capital efficiency

- working capital management

- speed of settlement across global partners

For large enterprises and high-volume fintechs, this can mean significant savings and more flexible liquidity operations.

5. On-Ramps & Off-Ramps: Connecting Blockchain to Local Currency

Stablecoins don’t eliminate the need for local bank accounts. To move into and out of blockchain rails, businesses use:

- On-ramps: Convert local currency → stablecoins

- Off-ramps: Convert stablecoins → local currency

These regulated providers act as bridges between blockchain and traditional finance.

They typically hold:

- a local bank account

- a blockchain wallet

This creates a smooth connection between the two systems.

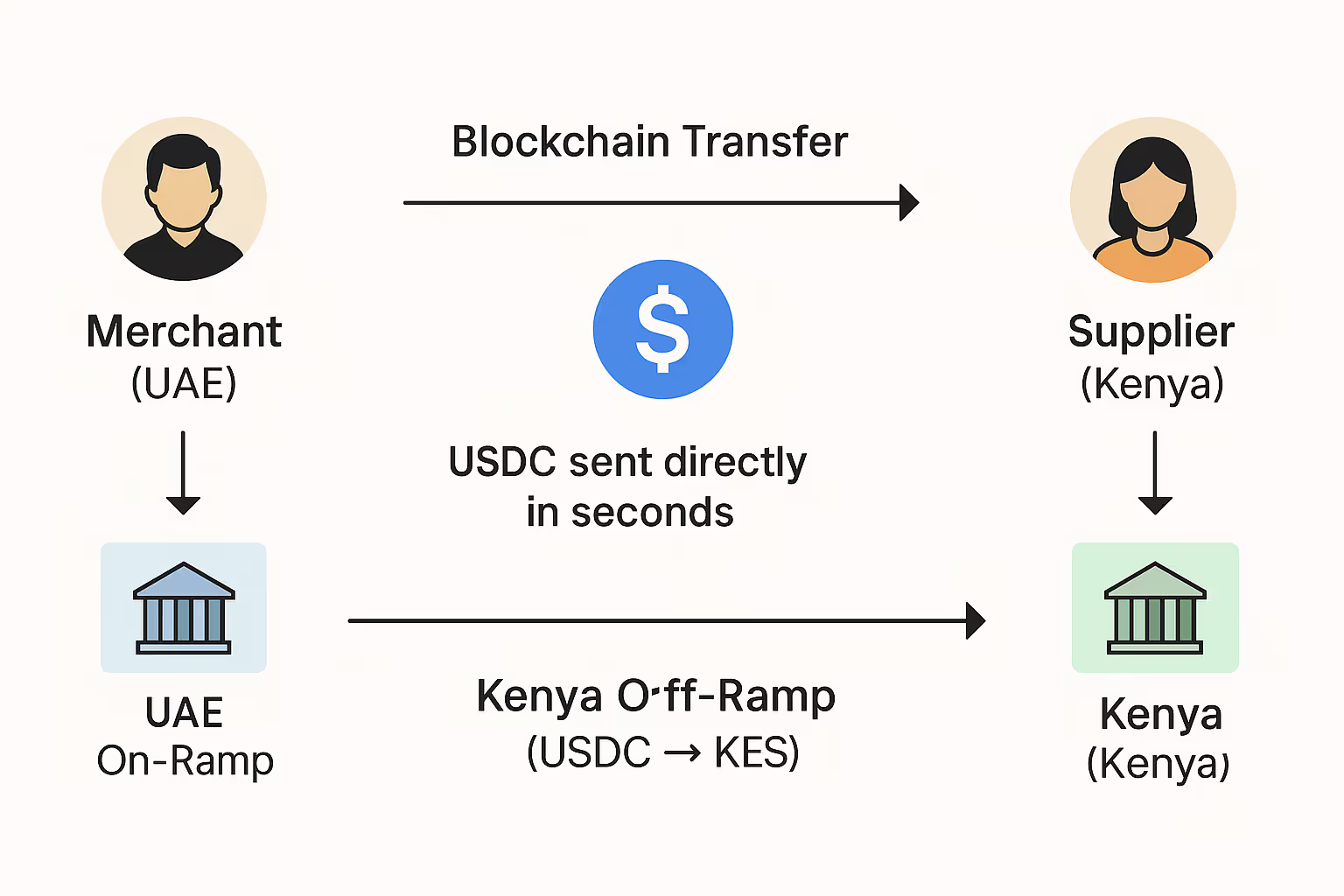

6. Example: UAE → Kenya Payment Using USDC

A UAE merchant wants to pay a supplier in Kenya:

Traditional method

UAE bank → SWIFT → correspondent banks → Kenya bank → Supplier

Time: 1–3 days

Fees: High

Liquidity: Requires prefunding across partners

Stablecoin-enhanced method

- Merchant sends AED to a UAE on-ramp.

- On-ramp converts AED → USDC.

- USDC moves on blockchain to Kenya off-ramp (5–20 seconds).

- Off-ramp converts USDC → KES.

- Supplier is paid locally via M-Pesa or bank.

Time: Seconds

Cost: Lower

Liquidity: No need for heavy prefunding

Control: Full visibility on settlement timing

Stablecoins make the cross-border leg instant while still relying on licensed local payout partners where needed.

7. Do Stablecoins Replace Fintechs? No — They Supercharge Them.

Stablecoins don’t eliminate the need for companies like Verto, TerraPay, Wise, or MFS Africa.

Instead, these companies increasingly use stablecoins inside their own settlement systems because they:

- reduce treasury costs

- decrease liquidity trapped in the system

- make payouts faster

- improve operational efficiency

The future of cross-border payments is hybrid:

local banking rails + blockchain-based global settlement.

8. What This Means for Merchants

Stablecoins offer:

- faster payments to international suppliers

- lower FX and settlement costs

- improved cash flow

- more predictable settlement times

- transparency and auditability

Businesses dealing with frequent international transfers — importers, exporters, software companies, logistics firms, marketplaces — stand to benefit significantly.

Conclusion

Stablecoins represent a major step forward in global payments.

They provide the stability of fiat, the speed of blockchain, and the capital efficiency that larger businesses and fintechs desperately need.

For merchants, this means:

- faster settlements

- lower costs

- better liquidity management

- more control over cash flow

The global payments landscape is evolving quickly — and stablecoins are shaping the next generation of cross-border finance.