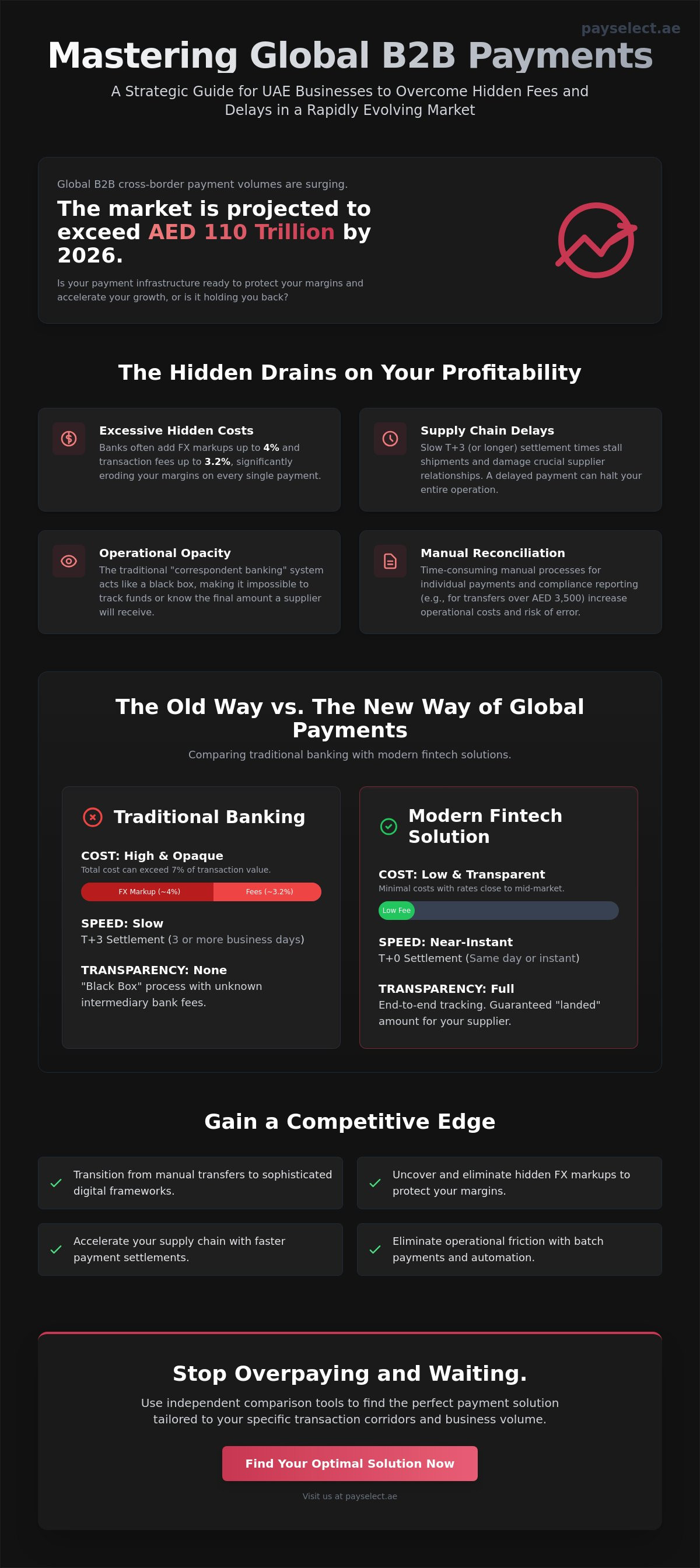

Global B2B cross-border payment volumes are forecasted to exceed AED 110 trillion by 2026, according to PaySelect's April 2026 report, yet many UAE firms still struggle with hidden foreign exchange markups as high as 4%. You likely recognize the frustration of seeing a supplier receive less than expected due to unexpected intermediary bank fees or watching payment delays stall your supply chain. When you need to pay overseas suppliers, the traditional banking route often feels like a black box of costs and manual reconciliation. It's time to shift from basic transfers to a strategic payment framework that protects your margins and strengthens your vendor relationships.

This guide helps you master the complexities of international B2B payments and discover how to choose the most efficient cross-border solutions for your specific needs. We'll examine the 2026 infrastructure options to show you how to streamline, accelerate, and scale your global operations while securing lower costs and faster settlement times. You'll learn how to integrate these tools into your existing accounting stack for seamless currency management and total visibility on every transaction you initiate.

Key Takeaways

• Transition from manual bank transfers to sophisticated digital frameworks that protect your margins and accelerate your supply chain.

• Discover the most cost-effective way to pay overseas suppliers by uncovering hidden FX markups and identifying the right fee structures.

• Evaluate the performance of traditional wire transfers against specialized fintech networks to optimize for speed, cost, and reliability.

• Eliminate operational friction by implementing batch payments and managing currency volatility with strategic forward contracts.

• Use independent comparison tools to find the perfect payment solution tailored to your specific transaction corridors and business volume.

The Strategic Importance of Efficient Overseas Supplier Payments

Overseas supplier payments are cross-border B2B transactions used to settle invoices with international vendors. For a growing business in the UAE, the ability to pay overseas suppliers isn't just a back-office task; it's a competitive lever. As global B2B payment volumes head toward AED 110 trillion by late 2026, the speed and cost of these transfers directly dictate your profit margins. Traditional manual bank transfers are becoming a strategic liability. They're slow, opaque, and increasingly incompatible with the Dubai Cashless Strategy, which aims for 90% digital transactions by the end of 2026. Understanding different methods of payment in international trade is essential for any firm looking to optimize its supply chain and maintain vendor trust.

Common Pain Points in UAE Cross-Border Commerce

Traditional banking routes often hide significant costs that many business owners overlook. Hidden foreign exchange markups can reach as high as 4% of the transaction value, while additional fees often climb to 3.2%. These costs eat into your bottom line without warning. Beyond the expense, the frustration of payments getting "lost" or delayed within the correspondent banking network erodes supplier relationships. A stalled payment can stop a shipment, damaging your reputation as a reliable partner. Compliance also adds friction. The UAE Central Bank requires detailed reporting for all international wire transfers exceeding AED 3,500. This regulation, combined with the new Central Bank law compliance deadline on September 16, 2026, makes manual processes too risky and slow for high-volume traders.

The Shift Toward Digital Payment Infrastructure

By 2026, technology has decentralized international settlements, moving them away from rigid legacy systems. Transparency is now the baseline expectation for every finance team. You need to know exactly what your vendor receives at the moment you hit send. This evolution has transformed payments from a simple utility into a tool for strategic cash flow management. Modern businesses looking to pay overseas suppliers must now look beyond their local branch. High-end fintech solutions offer borderless capabilities that provide the global reach necessary for modern UAE entrepreneurs. To solve these issues, many businesses use cross-border payment solution matching to identify providers that offer better transparency and faster settlement times. This shift empowers you to streamline operations, accelerate growth, and scale your business with absolute confidence.

Evaluating Cross-Border Payment Solutions: Key Performance Indicators

Selecting a partner to pay overseas suppliers requires more than a glance at a mobile app interface. You must analyze specific performance indicators that impact your liquidity and vendor relations. While the UAE Central Bank base rate sits at 3.65% as of May 8, 2026, the rates offered by individual providers vary wildly. The most critical KPIs include foreign exchange (FX) rates, transaction fees, and settlement speed. Each factor influences your bottom line differently depending on your transaction corridor.

Most traditional banks and some fintechs offer rates that deviate significantly from the mid-market exchange rate. This markup can reach 4% of the transaction value. When you add transaction fees that often hit 3.2%, a single transfer becomes prohibitively expensive. Speed is the next factor. In 2026, T+0 (same day) settlement is the gold standard, yet many legacy systems still rely on T+3 cycles. These delays often stem from the correspondent banking network; funds pass through multiple intermediary banks, each adding a fee and a delay. Understanding various international payment methods helps you identify which models prioritize direct settlement over these convoluted legacy paths.

Decoding the Real Cost of International Transfers

The final "landed" amount your supplier receives is often lower than your initial calculation due to intermediary bank "cable charges." The FX spread is the primary hidden cost in UAE banking, representing the difference between the wholesale market rate and the rate your provider gives you. To find your total cost of ownership (TCO), you must aggregate the FX markup, the outward transfer fee, and any potential recipient bank charges. If you're unsure which structure fits your volume, a cross-border payment solution matching service can provide the necessary clarity to optimize your spend.

Security Protocols and Fund Safety

Security is non-negotiable for high-end commerce. Elite providers use segregated client accounts, ensuring your business capital is never co-mingled with the provider’s operational funds. This structure provides a critical safety net. You should also evaluate two-factor authentication (2FA) and API security to prevent unauthorized access. With the new Central Bank law compliance deadline approaching on September 16, 2026, your chosen platform must strictly adhere to UAE AML and CTF regulations. Choosing a partner regulated by the Central Bank of the UAE ensures your transfers meet all legal reporting thresholds, such as the AED 3,500 reporting requirement, while protecting your global reach.

Comparing International Payment Methods for UAE Businesses

Choosing the right channel to pay overseas suppliers depends on your transaction volume, frequency, and urgency. No single provider fits every business model; instead, the "best" option is usually determined by your specific trade corridors. While traditional banks remain a staple for large-scale capital transfers, specialized fintech platforms have captured a significant share of the market by offering more transparent structures. In 2026, the global B2B payment landscape is more diverse than ever, providing UAE businesses with a variety of tools to manage their international obligations with absolute confidence.

Traditional wire transfers through the SWIFT network are the legacy standard. They're highly reliable but often carry heavy costs. Although the transition to the ISO 20022 standard was completed in November 2025 to improve data transparency, SWIFT payments still pass through multiple intermediary banks. This process often triggers high transaction fees and hidden FX markups. Conversely, specialized fintechs use proprietary digital networks to bypass these intermediaries, offering faster settlement and lower margins. For businesses managing hundreds of small transactions, digital wallets and multi-currency accounts provide a more agile alternative than standard corporate banking. Corporate credit and virtual cards have also become essential for immediate vendor payments and SaaS subscriptions, offering instant settlement and simplified expense tracking.

SWIFT vs. Local Clearing Networks

Local clearing networks like SEPA in Europe or ACH in the United States offer a way to bypass the expensive SWIFT route. When you access these via a UAE partner, you can settle invoices as if you were a local business. This drastically reduces the fees associated with being an "international" sender. While SWIFT's reliability justifies the cost for multi-million dirham capital transfers, most operational expenses are better served by cross-border payment solutions that tap into these local clearing systems. Finding the right balance between speed and cost is easier when you use cross-border payment solutions comparison tools to audit your current provider's performance.

The Rise of Multi-Currency IBANs

Holding local currency accounts abroad is a game-changer for UAE trading houses. Multi-currency IBANs allow you to receive funds and pay overseas suppliers in their local currency, such as EUR, GBP, or CNY, without triggering a conversion at every step. This "Receive and Pay" ecosystem eliminates the double-conversion trap where your Dirhams are converted to Dollars and then into the supplier's currency. It streamlines your accounting and makes you a preferred partner for international vendors who want to avoid their own local bank's conversion fees. This borderless approach ensures your capital moves as fast as your ambition.

Eliminating Friction in Global Supply Chain Transactions

Efficiency in 2026 is defined by the removal of manual barriers. When you pay overseas suppliers, the friction isn't just in the cost; it's in the hours your finance team spends on data entry and error correction. Moving toward a borderless operation requires standardizing your supplier onboarding process. By validating IBAN and SWIFT codes at the point of entry, you eliminate the risk of "lost" payments that often plague traditional banking routes. This structural clarity ensures that your capital moves with the same speed as your digital orders.

Currency volatility management is another critical pillar of a frictionless supply chain. While the UAE Dirham remains pegged to the US Dollar, your obligations in EUR, GBP, or CNY are subject to constant market shifts. Forward contracts allow you to lock in exchange rates for future supplier obligations, protecting your profit margins from sudden devaluations. This strategic foresight transforms your payment infrastructure from a simple cost center into a tool for financial stability. For businesses managing high volumes, batch payments allow you to execute hundreds of international transfers with a single file upload, drastically reducing the administrative load.

Integration with your existing ERP and accounting software, such as Xero, QuickBooks, or Oracle, ensures a seamless data flow. Modern platforms allow for direct synchronization, meaning your ledger updates the moment a settlement is confirmed. This connectivity is essential for maintaining clear visibility on your global reach. If your current setup still requires manual exports and imports, it's time to compare cross-border payment solutions that offer native API integrations to empower your growth.

Automating the Accounts Payable Workflow

API-driven payments reduce manual entry errors and save finance teams approximately 15 to 20 hours per month. By implementing multi-level approval workflows, you maintain strict internal controls over large overseas transfers without slowing down the process. Payment Reconciliation is the final step in a frictionless supply chain, ensuring that every outgoing transfer matches the corresponding invoice in your ledger without manual intervention. This automation allows your team to focus on scaling rather than troubleshooting.

Managing Regulatory Reporting Requirements

The UAE Central Bank mandates the use of Purpose of Payment (PoP) codes for all international transfers to ensure transparency. Additionally, any transfer equal to or exceeding AED 3,500 must be accompanied by detailed originator and beneficiary information as of May 2026. Modern digital platforms handle this reporting automatically, ensuring you stay compliant with national regulations and the 5% standard VAT rate on imported services. This automated compliance is vital for businesses looking to pay overseas suppliers while meeting the strict September 16, 2026, Central Bank law compliance deadline.

Optimising Your Global Reach with PaySelect

In an era where global B2B payment volumes exceed AED 110 trillion, the cost of inefficiency is too high to ignore. You've seen how hidden FX markups of up to 4% and complex correspondent banking fees can erode your margins. Finding the most efficient way to pay overseas suppliers shouldn't involve hours of manual spreadsheet comparisons or guesswork. PaySelect acts as your strategic partner, providing the structural clarity needed to navigate the crowded fintech market. We don't process your payments; instead, we empower you to choose the provider that offers the best rates for your specific transaction corridors.

PaySelect’s 'Take the Test' tool is designed for speed and precision. It matches your unique business volume and currency needs to the most effective cross-border solutions available in May 2026. For larger enterprise groups, our payment infrastructure consulting and cost optimization audits provide a deep dive into your current stack. We identify exactly where you're overpaying and show you how to streamline your global reach. This independent approach ensures you aren't just following a provider's marketing but are making decisions based on real transaction data and success rates.

Unbiased Insights for Modern Merchants

Comparing multiple payment gateways and cross-border solutions in one centralized location saves you days of research. PaySelect maintains strict independence, delivering transparent market data that moves beyond provider claims. We help you see the real performance behind transaction success rates and settlement speeds. This transparency is the baseline for any UAE finance team looking to scale without the burden of legacy banking fees or opaque pricing models. By choosing a solution tailored to your needs, you ensure your capital moves as fast as your ambition.

Next Steps for Your Business

Optimizing your payment stack starts with a clear view of your current expenses. Conduct a 15-minute audit of your international payment costs by aggregating your last three months of FX markups and wire fees. Once you've identified the gaps, prepare your corporate documentation to ensure a seamless transition to a specialized provider. For a bespoke review of your global financial infrastructure, you can reach out for cross-border payment solution matching. It's time to remove the barriers to your growth and secure a borderless future for your enterprise. Every Dirham saved on transaction fees is a Dirham you can reinvest in your company's expansion. Start your journey toward cost optimization today and ensure you pay overseas suppliers with absolute confidence.

Scale Your Global Operations with Absolute Confidence

Transitioning your international B2B payments from a legacy banking utility to a strategic asset is essential for UAE businesses in 2026. You now have the tools to bypass hidden 4% FX markups and eliminate the friction of correspondent banking delays. By prioritizing T+0 settlements and seamless ERP integrations, you protect your margins and strengthen your global vendor relationships. The ability to pay overseas suppliers with speed and transparency ensures your capital is always working to scale your reach rather than being eroded by unnecessary transaction fees.

Efficiency in the digital economy requires a partner that values your time and security. PaySelect offers independent and unbiased comparison data, MENA-focused payment expertise, and expert advisory for high-volume merchants. We help you cut through the marketing noise to find the most cost-effective infrastructure for your specific trade corridors. Take the PaySelect test to find your ideal cross-border payment partner and start optimizing your international settlements today. Your path to a borderless, high-performance finance function starts here.

Frequently Asked Questions

What is the cheapest way to pay overseas suppliers from the UAE?

Specialized fintech networks are generally the most cost-effective option as they provide rates closer to the mid-market exchange rate. Traditional banking routes often include hidden FX markups of up to 4% and transaction fees reaching 3.2% of the value. By using an independent comparison tool, you can identify providers that tap into local clearing networks to reduce these overheads significantly.

How long do international business payments usually take to settle?

Settlement times range from instant (T+0) to three business days (T+3) depending on the chosen network and destination. While the SWIFT network has improved with ISO 20022 standards as of late 2025, payments can still be delayed by intermediary banks. Specialized cross-border solutions often offer same-day settlement by using local payout accounts in the supplier's home country.

Are fintech payment platforms as safe as traditional UAE banks?

Regulated fintech platforms are as safe as traditional banks because they must comply with strict UAE Central Bank oversight and reporting standards. These providers use segregated client accounts to ensure your business capital is never co-mingled with their operational funds. Look for platforms that implement two-factor authentication and meet the new Central Bank law compliance deadline of September 16, 2026.

What information do I need from my supplier to initiate a cross-border payment?

To pay overseas suppliers, you need their full legal name, IBAN or account number, and the SWIFT/BIC code of their bank. For UAE-based businesses, you must also provide a Purpose of Payment (PoP) code for every international transfer to stay compliant. For transactions exceeding AED 3,500, additional originator and beneficiary details are required by law as of May 2026.

Can I pay international suppliers in their local currency to avoid FX markups?

Yes, paying suppliers in their local currency is a highly effective strategy to eliminate double-conversion costs and improve vendor trust. Using multi-currency IBANs allows you to hold and send currencies like EUR, GBP, or CNY directly from your digital wallet. This approach ensures your vendor receives the exact invoice amount while you avoid the high FX markups typically charged by traditional retail banks.

What are intermediary bank fees and how can I avoid them?

Intermediary bank fees are charges taken by "correspondent" banks that move money between the sender's bank and the receiver's bank. You can avoid these by choosing payment solutions that use local clearing systems like SEPA in Europe or ACH in the United States. This bypasses the traditional SWIFT chain, ensuring the final amount received by your supplier is not reduced by unexpected "cable charges."

Do I need a special license to use a digital cross-border payment solution in the UAE?

Business owners don't need a special license to use digital cross-border payment solutions; you only need to meet standard KYC and AML requirements. The responsibility for licensing lies with the payment provider, which must be authorized by the Central Bank of the UAE or an equivalent global regulator. Ensure your chosen partner is fully compliant with the new remuneration regulations starting October 11, 2026.

How does the AED/USD peg affect my international payment strategy?

The AED/USD peg provides exchange rate stability for payments made in US Dollars, but it exposes you to volatility in other currency pairs. Since the Dirham follows the Dollar, your costs to pay overseas suppliers in Euro or Yen will fluctuate based on global market shifts. Strategic firms use forward contracts to lock in rates and mitigate this risk for future supplier obligations.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.