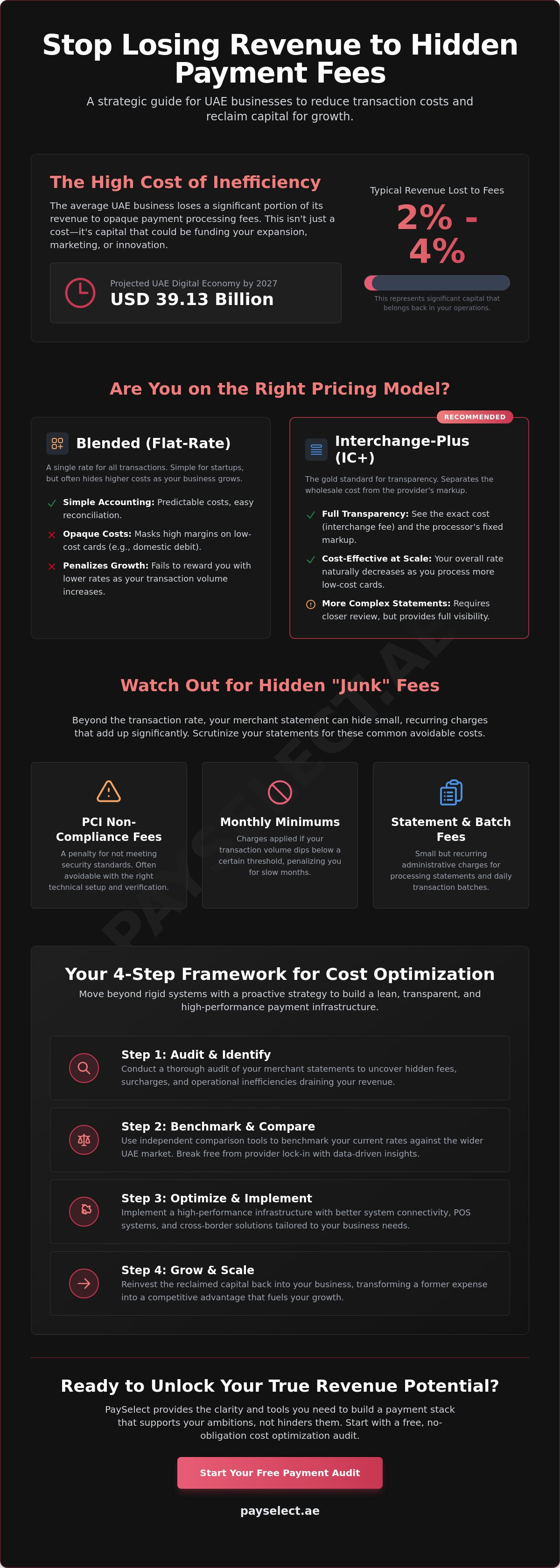

The average UAE business loses between 2% and 4% of its total revenue to payment processing fees. In a digital economy projected to reach USD 39.13 billion by 2027, these margins represent significant capital that belongs back in your operations. You likely struggle with opaque fee structures that are difficult to reconcile or feel trapped by high cross-border costs that limit your international reach. It is frustrating to feel locked into a specific provider simply because the infrastructure seems too complex to change.

We believe your payment setup should be a catalyst for growth, not a barrier. This guide provides a professional strategy on how to reduce payment transaction fees by auditing your current stack and benchmarking against the latest industry standards. You will learn a clear framework for comparing providers independently and reclaiming lost revenue through better system connectivity. PaySelect facilitates this transition through payment pricing comparison tools and cost optimization audits. We help you match with the right cross-border solutions and POS systems to ensure your infrastructure is lean, transparent, and ready for expansion. It is time to move beyond rigid systems and optimize for performance.

Key Takeaways

• Audit your merchant statements to identify hidden costs and operational inefficiencies that drain your annual revenue.

• Discover how to reduce payment transaction fees by shifting from flat-rate pricing to more transparent, data-driven fee structures.

• Implement advanced verification protocols to lower risk-based surcharges and improve the performance of your B2B sales.

• Break free from provider lock-in by using independent comparison tools to benchmark your current rates against the wider UAE market.

• Build a high-performance infrastructure that prioritizes system connectivity and long-term cost optimization over simple setup speed.

The Impact of Transaction Fees on Business Scalability

Transaction fees are frequently dismissed as a static utility cost. This perspective is a strategic oversight. While a fee of 2.8% might seem manageable on a single invoice, it compounds into a heavy drain on your annual liquidity. For an expanding enterprise, these percentage points represent the difference between stagnant growth and aggressive reinvestment. Understanding how to reduce payment transaction fees is not just about cutting costs; it is about reclaiming capital to fund your next expansion. When you treat payment processing as a variable growth lever, you unlock significant resources that were previously lost to the system.

The Hidden Cost of Revenue Leakage

Revenue leakage extends beyond the headline transaction rate. It includes the hidden costs of failed payments, manual reconciliation hours, and the high churn rates associated with poor gateway performance. Many business owners view these inefficiencies as an unavoidable reality of doing business. They aren't. By evaluating POS systems and digital interfaces, you can identify where technical friction is eroding your margins. High-performance infrastructure ensures that more of your gross revenue reaches your bank account, reducing the operational overhead required to manage your cash flow. This shift in mindset transforms a passive expense into a managed asset.

Why Traditional Fee Models Often Penalize Growth

Standard flat-rate models provide a simple entry point for startups, but they quickly become a liability as volume increases. These models bundle various underlying costs, such as interchange fees, into a single high rate that ignores your specific business profile. Tiered pricing structures can be equally problematic. They often hide expensive surcharges behind a low "qualified" rate, penalizing you for accepting corporate or international cards. As your business matures, shifting toward a more transparent infrastructure allows for better cost control. A Payment Cost Optimization Audit identifies these discrepancies, moving you away from "plug-and-play" solutions that no longer serve your scale.

Adopting a strategy for how to reduce payment transaction fees transforms a passive expense into a competitive advantage. This proactive approach ensures your financial foundation remains agile. PaySelect bridges the gap between complex global systems and your specific needs, providing the clarity required to scale without unnecessary friction. By benchmarking your current rates against the wider market, you can ensure your payment stack supports your international ambitions rather than hindering them.

Decoding Your Merchant Statement: Identifying Hidden Fees

A merchant statement often feels like a puzzle designed to obscure the actual cost of doing business. For UAE entrepreneurs, deciphering these documents is the first critical step in learning how to reduce payment transaction fees. Most providers present costs in a way that makes direct comparison difficult, mixing essential network costs with arbitrary markups. Identifying these discrepancies allows you to negotiate from a position of strength and reclaim lost margins. It's about moving from a state of confusion to one of absolute financial clarity.

Interchange-Plus vs. Blended Pricing

Transparency begins with your pricing model. Interchange-Plus is the gold standard for established businesses. It separates the actual cost of the transaction from the processor's markup. This clarity allows you to see exactly what the card networks charge and what your provider adds on top. Conversely, Blended pricing offers a single, flat rate for all transactions. While this simplifies accounting for startups, it often masks significantly higher margins on low-cost domestic debit cards. You end up paying a premium for simplicity that your business might no longer require.

To ensure you aren't overpaying, check your merchant service agreement for these common junk fees:

PCI Non-Compliance Fees

Charges applied if your system isn't verified, which are often avoidable with the right technical setup.

Monthly Minimums

Penalties applied if your transaction volume falls below a specific threshold during a slow month.

Statement and Batch Fees

Small, recurring administrative charges that add up over a fiscal year.

The Anatomy of a Cross-Border Transaction

International expansion introduces a new layer of complexity. When a customer pays with a card issued outside the UAE, you face regional surcharges and currency conversion margins. These FX spreads are rarely disclosed as a transparent line item. Instead, they are baked into the conversion rate, often costing businesses an additional 1% to 3% per sale. Understanding these dynamics is essential for any brand targeting global markets. Regional banking regulations also play a role, as they can impact both the cost and the speed of your settlements.

Optimizing these costs requires more than just a standard gateway. Effective cross-border payment solutions utilize local acquiring and smart routing to bypass international surcharges. This reduces settlement times and keeps more revenue in your account. If you're unsure if your current provider is giving you the best market rate, a payment pricing comparison can highlight exactly where your capital is leaking. Recent updates from the Central Bank of the UAE regarding Merchant Discount Rates make this the ideal time to re-evaluate your infrastructure and ensure your provider remains competitive in a fast-moving landscape.

Strategic Methods to Lower Payment Processing Expenses

Active management is the cornerstone of cost control. Once you identify where your revenue is leaking, you must implement technical and commercial adjustments to plug those gaps. Learning how to reduce payment transaction fees requires a move away from passive acceptance of bank rates. It involves a strategic combination of data optimization, risk management, and vendor negotiation. By treating your payment infrastructure as a dynamic system, you can consistently drive down the cost of every dirham processed.

Your transaction volume is your most powerful negotiating tool. Merchants with monthly processing volumes exceeding AED 50,000 possess the leverage to move away from standard rates toward more competitive, tier-based pricing. When you approach providers with clear growth projections, you position your business as a high-value partner rather than a generic client. Don't settle for the first offer. Use a Payment Cost Optimization Audit to benchmark your current expenses and present a data-backed case for lower margins. This proactive stance often results in immediate savings that scale alongside your business.

Diversifying your payment methods also provides a path to lower costs. While credit cards are essential, they are often the most expensive way to receive funds. Direct bank transfers and local digital wallets frequently offer lower processing overhead. By offering these alternatives alongside traditional cards, you give customers choice while steering high-value transactions toward more cost-effective rails. This approach reduces your overall blended rate without impacting the user experience.

Reducing Risk to Lower Surcharges

Card networks penalize high-risk behavior with transaction "downgrades," which carry significantly higher fees. Implementing 3D Secure protocols shifts the liability for fraudulent chargebacks away from your business and onto the card issuer, protecting your bottom line. Address Verification Service (AVS) validates the cardholder's billing address to reduce the likelihood of fraudulent surcharges and secure lower processing fees. These security measures do more than prevent fraud; they signal to processors that your transactions are low-risk, allowing you to qualify for the most favorable rates available.

B2B Optimization: Level 2 and Level 3 Data

For companies operating in the B2B sector, transmitting enhanced transaction data is a primary strategy for how to reduce payment transaction fees. Level 2 and Level 3 processing require additional fields such as tax IDs, freight amounts, and commodity codes. Because this data provides a higher level of transaction transparency, card networks reward merchants with significantly lower interchange rates. To capitalize on this, you must select payment gateways that support advanced data transmission. This technical shift can reduce your processing costs by up to 1% on corporate and government card transactions, providing a substantial competitive advantage in high-ticket industries.

The Power of Independent Benchmarking and Comparison

Relying on a single bank’s proprietary gateway often leads to price stagnation. Without a competitive benchmark, providers have little incentive to lower your rates as your volume grows. Developing a strategy for how to reduce payment transaction fees requires looking beyond your current provider’s dashboard. True cost optimization happens when you compare your current setup against the wider market using unbiased data. This independent approach ensures you aren't overpaying for legacy systems that no longer match your scale.

When evaluating new providers, focus on the Total Cost of Ownership (TCO) rather than just the headline transaction rate. A low percentage can be quickly offset by high monthly maintenance fees, integration costs, and hidden payout charges. A professional tender process involves gathering data on setup time, system connectivity, and technical support. This comprehensive view prevents the common mistake of choosing a provider based on a single metric only to lose those savings through operational friction later. High-end businesses prioritize efficiency and reliability alongside cost.

Breaking the "Bank-Locked" Cycle

Decoupling your merchant account from your primary business bank is a strategic move for long-term agility. While keeping everything under one roof seems convenient, it creates a "lock-in" effect that limits your negotiating power. Gateway-agnostic solutions allow you to route transactions through multiple providers based on cost and performance. This setup requires robust system connectivity, but the benefit is absolute leverage. If one provider raises their margins, you have the infrastructure ready to shift volume to a more competitive alternative. It transforms your payment stack from a fixed utility into a strategic tool for business transformation.

Using Comparison Tools for Market Transparency

Market transparency is the enemy of high fees. PaySelect’s "Take the Test" tool matches your specific business needs with provider capabilities, ensuring you only pay for the features you actually use. In a fluctuating financial landscape, real-time pricing data is essential for maintaining lean operations. Independent audits reveal savings that internal teams often miss by identifying redundant services and misclassified transactions. These audits provide the clarity needed to make informed decisions without the bias of a traditional salesperson. Use our Payment Gateway Comparison Tool to instantly benchmark your current rates against the industry standard and identify immediate opportunities for optimization.

Implementing a High-Performance Payment Infrastructure

A "plug-and-play" mindset is sufficient for startups, but it becomes a bottleneck for scaling UAE enterprises. Realizing how to reduce payment transaction fees at scale requires a shift toward a strategic infrastructure approach. This means viewing your payment stack not as a series of isolated tools, but as a unified ecosystem. High-performance infrastructure ensures seamless system connectivity across your POS, e-commerce platforms, and ERP systems. When these components communicate effectively, you eliminate the manual reconciliation errors and technical redundancies that silently inflate your operational costs.

Efficiency is not a one-time achievement. It requires a disciplined schedule of quarterly payment cost audits to ensure your providers remain competitive. The financial landscape moves quickly. Rates that were industry-standard six months ago may now be outdated. By establishing a regular review cycle, you maintain constant pressure on your margins and ensure your infrastructure remains lean. This proactive management prevents "fee creep" and keeps your business agile in a fast-moving digital economy.

The Role of Professional Payment Advisory

There comes a point where DIY comparison tools reach their limit. For businesses managing complex multi-entity structures or high-volume international flows, Payment Infrastructure Consulting becomes essential. This move from self-service to a fixed-fee advisory model allows for a deeper, more comprehensive payment infrastructure audit. These elite-level transitions focus on optimizing the entire lifecycle of a transaction, from the initial swipe to the final bank settlement. PaySelect facilitates these sophisticated migrations, ensuring that your transition to a new provider is frictionless and data-driven.

Future-Proofing Your Payment Stack

The global payment landscape is shifting toward open banking and real-time account-to-account transfers. These emerging technologies have the potential to disrupt traditional fee models by bypassing expensive card networks entirely. To stay ahead, you must build a stack that is flexible enough to adopt these new, lower-cost payment rails as they gain mainstream traction. A rigid system is a costly system. Future-proofing ensures your business is always positioned to take advantage of the most efficient technology available. It is time to stop reacting to fee increases and start leading your industry with a superior financial foundation. You can begin your payment optimization journey today and transform your payment setup into a strategic asset for growth.

Optimize Your Financial Foundation for Future Growth

Optimizing your payment stack is a continuous strategic process rather than a one-time task. You've learned that deciphering merchant statements and implementing advanced data protocols are essential steps in how to reduce payment transaction fees. By shifting from a rigid, bank-locked setup to a fluid, high-performance infrastructure, you reclaim capital that fuels your expansion. Maintaining this efficiency requires regular audits and a commitment to independent benchmarking within the local market.

PaySelect provides the specialized focus on the UAE and MENA market that modern entrepreneurs require. Our platform offers independent and unbiased comparison data alongside expert advisory for enterprise-scale organizations. We bridge the gap between complex global infrastructure and your specific operational needs. Take the PaySelect Test to find your ideal payment partner and ensure your business remains agile, transparent, and ready for international commerce. Your revenue belongs in your business; it's time to secure it.

Frequently Asked Questions

How much can a typical business save by optimizing payment fees?

Savings often range from 0.5% to 1.5% of total processing volume depending on your current pricing model. For a high-volume UAE merchant, this translates into tens of thousands of dirhams reclaimed annually. The exact figure depends on your transaction mix, industry risk profile, and current use of legacy flat-rate pricing. A Payment Cost Optimization Audit identifies these specific gaps and quantifies the potential return on investment.

Is it difficult to switch payment gateways without losing transaction data?

Switching is a structured process that doesn't require losing customer vault data if managed correctly. Most modern providers support secure data migrations using industry-standard protocols to move card tokens between environments. It is essential to verify that your current setup allows for portable tokenization. This ensures a smooth transition and maintains the continuity of your recurring billing cycles without requiring customers to re-enter their details.

What is the difference between an acquirer and a payment gateway?

An acquirer is the financial institution that processes the payment and settles funds into your bank account. A payment gateway is the technical interface that captures and encrypts credit card information at the point of sale. While some companies provide both services, understanding the distinction helps you identify how to reduce payment transaction fees by negotiating with each entity separately. Decoupling these services can often lead to better technical flexibility and lower margins.

Can I negotiate my credit card processing rates even if I have a contract?

Yes, merchant contracts are often negotiable, particularly if your transaction volume has increased significantly since the initial signing. Providers are usually willing to review terms to retain high-growth clients in a competitive landscape. Presenting independent benchmarking data from a pricing comparison tool provides the leverage needed to secure more favorable margins mid-contract. It is a standard business practice to request a rate review annually as your enterprise scales.

How do cross-border payment fees differ from domestic transaction fees?

Cross-border fees include additional regional surcharges and currency conversion margins that do not apply to domestic sales. These costs can be 2% to 3% higher than local transactions due to the involvement of international card networks. Optimizing these expenses requires specialized Cross-border Payment Solution Matching to access local acquiring networks. This strategy allows you to bypass international markups and settle funds in your local currency with minimal friction.

What are Level 2 and Level 3 processing data, and how do they save money?

These are enhanced data fields, such as tax IDs and commodity codes, required for B2B and government transactions. Providing this extra information reduces the perceived risk of the sale for the card issuer. In return, card networks offer lower interchange rates, which is a primary method for how to reduce payment transaction fees in the corporate sector. Utilizing a gateway that supports these data-rich transactions can significantly lower your processing overhead.

Why do some providers charge a monthly fee in addition to transaction percentages?

Monthly fees often cover administrative costs, PCI compliance tools, and access to premium technical support. While some providers offer "no monthly fee" models, they frequently compensate by charging higher transaction percentages on every sale. A Payment pricing comparison is necessary to determine which model results in a lower total cost based on your specific volume. For high-volume merchants, a fixed monthly fee with lower transaction margins is usually the most efficient choice.

How does PaySelect maintain independence when comparing providers?

PaySelect operates as an independent facilitator rather than a processing service. We utilize a data-driven comparison tool to match business requirements with provider capabilities based on objective technical and commercial criteria. Our methodology focuses on market transparency, ensuring businesses find the right infrastructure without the bias of a traditional sales representative. We provide the data and the framework, but the final decision always remains with the business owner.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.