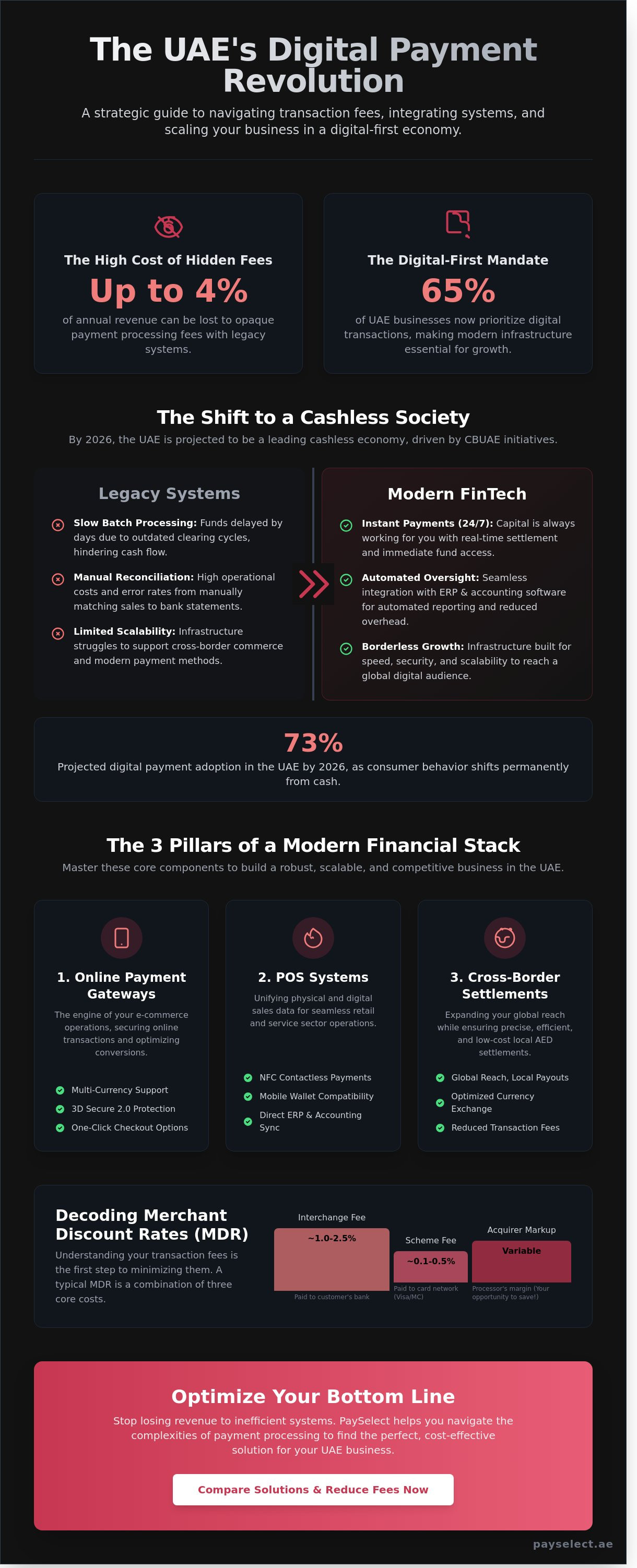

What if the hidden fees buried within your payment processing are quietly eroding 4% of your annual revenue? According to 2024 regional commerce reports, 65% of UAE businesses now prioritize digital-first transactions, meaning a legacy payment setup isn't just slow; it's expensive. You've likely felt the sting of opaque fee structures and the friction of trying to bridge the gap between international gateways and local AED settlements. Successfully managing money uae enterprises generate requires a strategy that balances global reach with local precision.

This guide provides a clear framework to compare payment solutions, reduce your merchant discount rates, and empower your growth. You'll discover how to integrate your POS and online systems into one seamless, high-performance infrastructure. We're breaking down the complexity of cross-border settlements so you can focus on scaling your brand with absolute confidence and speed.

Key Takeaways

• Master the shift to a cashless society and leverage the latest Central Bank initiatives to modernize your transaction flow.

• Build a robust financial stack that integrates seamless payment gateways to scale your operations across the borderless digital marketplace.

• Decode complex Merchant Discount Rates (MDR) to minimize high transaction fees and optimize the way you manage business money uae.

• Align your payment infrastructure with industry-specific needs and ensure technical compatibility with your current ERP for a frictionless integration.

• Streamline your provider selection process using independent tools that bridge the gap between complex infrastructure and your growth ambitions.

The Evolution of Money in the UAE: From Cash to Digital-First Commerce

The UAE financial landscape is undergoing a radical transition. By 2026, the nation is positioned to become a leading cashless society. This shift isn't just about convenience; it's a strategic pillar of the Economy of the United Arab Emirates as it diversifies away from oil. The Central Bank of the UAE (CBUAE) continues to drive this change through massive digital initiatives that modernize how businesses handle money uae. For merchants, the stable Dirham (AED) remains the foundation, but the way it moves has changed forever. Traditional banking models often struggle to keep pace with this velocity. Modern enterprises now require specialized fintech solutions to stay competitive and maintain liquidity.

Managing business money uae requires a shift in mindset from manual reconciliation to automated digital oversight. The government's Financial Infrastructure Transformation (FIT) program, launched in 2023, has already accelerated the adoption of instant payments. This environment rewards companies that prioritize digital integration. Businesses that cling to legacy systems risk facing higher operational costs and slower growth cycles. Success in this market demands a partner that understands the intersection of local regulations and global technology standards.

• Streamline daily operations through automated reporting.

• Accelerate growth by reaching a wider digital audience.

• Scale effortlessly with infrastructure built for the future.

Digital Transformation of the UAE Dirham

Physical cash is no longer the primary medium for commerce in the Emirates. The transition to instant digital settlements allows businesses to access funds immediately rather than waiting days for batch processing. Real-time payment systems now operate 24/7/365, removing the delays of legacy clearing cycles that once hindered cash flow. This constant availability ensures that capital is always working for the business. By 2026, digital payment adoption in the UAE is projected to reach 73% of all transaction volumes as consumer behavior shifts permanently away from physical currency.

The Rise of the Fintech Ecosystem

Independent platforms are redefining the standard for payment processing across the region. While traditional banks offer stability, fintech providers deliver the agility required for modern e-commerce and retail. These platforms focus on three core pillars: speed, security, and scalability. Navigating the regulatory requirements of authorities like the CBUAE or the Dubai Financial Services Authority is mandatory for any operator. Many businesses face significant pain points such as long onboarding times and high transaction fees when using older systems. Utilizing advanced payment gateways helps solve these issues by offering seamless, borderless, and optimized transaction flows. Efficiency is the new benchmark for success in the digital economy.

The Three Pillars of Business Money Management in the UAE

Scaling a company in the Emirates requires more than a traditional bank account. You need a robust financial stack that synchronizes digital transactions, physical sales, and international transfers. This infrastructure forms the backbone of how you manage money uae in a market that moves at the speed of light. To maintain a competitive edge, businesses must master three core pillars: digital gateways, physical terminals, and cross-border settlement systems.

Online Payment Gateways: Your Digital Cashier

The gateway is the engine of your e-commerce operations. It secures transactions through advanced tokenization and 3D Secure 2.0 protocols, ensuring merchant data remains protected from fraud. When selecting a provider, prioritize multi-currency support and integration with local card schemes. This flexibility allows you to accept payments in AED while catering to global customers without friction. You can explore the latest payment gateways in the UAE to identify which features align with your digital growth strategy.

• Reduce cart abandonment with one-click checkout options.

• Ensure compliance with Central Bank of the UAE regulations.

• Access real-time analytics to track conversion rates instantly.

POS Systems: Physical Transaction Excellence

Retail and service sectors require hardware that does more than just swipe cards. Modern POS machines must support NFC technology for Apple Pay, Google Pay, and mobile wallets. The real value lies in integration. Connecting your physical sales data directly to your digital accounting software eliminates manual entry errors and provides a unified view of your cash flow. If you're upgrading your storefront, evaluate the latest POS machines to find hardware that scales with your transaction volume.

Cross-Border Money Movement

Expanding across the GCC or sourcing goods from international suppliers introduces foreign exchange (FX) risks. A single shift in currency value can erode your profit margins if you don't have a plan. Efficient regional settlements allow you to move money between the UAE, Saudi Arabia, and other markets without the heavy burden of intermediary bank fees. It's about creating a borderless financial operation. You should optimize your strategy for cross-border payments to reduce hidden FX costs and accelerate your international expansion. Managing money uae effectively means looking beyond the borders of the Emirates to empower your global reach.

For businesses ready to streamline their operations, finding the right partner to integrate these financial tools is the first step toward total optimization.

Comparing Payment Costs: Understanding the Fine Print of UAE Transactions

UAE merchants frequently ask why their transaction fees seem high. It's the most common objection when setting up a payment stack. To manage money uae companies earn effectively, you must decode the Merchant Discount Rate (MDR). This isn't a single fee. It consists of the interchange fee for the issuing bank, the scheme fee for the card network, and the processor’s markup. Without a clear breakdown, you’re likely overpaying for basic processing services.

Beyond the MDR, hidden costs can erode your margins quickly. Many providers in the region implement setup charges ranging from 500 AED to 2,500 AED. Monthly minimum fees apply if your transaction volume fails to meet a specific threshold, penalizing you during slow business months. Refund penalties are particularly aggressive. Some processors retain the original processing fee even when you issue a full refund to the client, effectively doubling your cost on a failed sale.

Fixed vs. Variable Cost Models

Startups processing under 50,000 AED monthly often prefer flat-rate pricing. It offers predictability and simplifies accounting. However, as you scale toward enterprise levels, Interchange+ models become superior for your bottom line. This model passes the actual cost of the transaction directly to you with a transparent markup. While blended pricing appears simple, it often masks higher margins by applying a uniform rate to transactions that would otherwise qualify for lower interchange costs. Switching to a more transparent model can save a high-volume business thousands of dirhams annually.

Settlement Cycles and Liquidity

Cash flow is the lifeblood of your operation. A T+1 settlement means your funds arrive the next business day, while a T+3 cycle delays your liquidity by 72 hours. For a business doing 100,000 AED in daily sales, that two-day gap represents 200,000 AED in trapped capital that you can't use for inventory or payroll. PaySelect helps businesses overcome these hurdles by offering sophisticated payment gateways that prioritize speed and clarity.

Reserve Funds

Some providers hold 5% to 10% of your volume for 30 days to mitigate risk.

Reporting

Transparent, real-time dashboards are essential for daily reconciliation of money uae transactions.

Integration

Seamless API connections reduce the manual labor costs associated with financial tracking.

Operational efficiency depends on how quickly you can move your capital. Choosing a partner that offers clear reporting ensures you never lose track of a single dirham. By eliminating the friction in the settlement process, you empower your business to scale without the constraints of traditional, slow-moving banking structures.

Strategic Selection: How to Choose Your Financial Infrastructure

Selecting the right payment partner is a pivot point for your growth. In a market as dynamic as the Emirates, your infrastructure must do more than just process transactions. It must align with your specific industry model. A high-volume F&B outlet requires rapid, reliable hardware for face-to-face payments, while an e-commerce platform demands a gateway that converts international traffic into local revenue. Professional service firms often prioritize automated invoicing and recurring billing to manage their money uae and maintain healthy cash flows. Efficiency is the benchmark for success in 2026.

Technical compatibility remains a frequent bottleneck for expanding firms. Before committing, verify that the provider integrates directly with your existing ERP or website framework. Poorly documented APIs lead to delays, high development costs, and missed opportunities. Test the merchant dashboard and the customer checkout flow personally. A frictionless experience reduces cart abandonment, which averaged 75% in some regional sectors during 2024, and builds long-term loyalty. Local support is equally vital. When technical issues arise, waiting for a response from a different time zone isn't an option for a business operating in the fast-paced UAE market.

Matching Provider Capabilities to Business Scale

A startup's needs differ from an established hospitality group managing multiple venues. Startups require agility and low entry barriers. Large enterprises need a partner capable of handling sudden spikes during seasonal sales or major events like the Dubai Shopping Festival. Scalability ensures your system won't crash when volume triples overnight. Look for robust API documentation that allows your team to build custom integrations. This flexibility allows you to streamline operations, accelerate settlements, and scale your reach without technical friction. Managing money uae effectively requires a system that grows alongside your transaction volume.

Security and Compliance Standards

Security is the foundation of digital commerce. In the UAE, PCI-DSS compliance is a non-negotiable standard for protecting sensitive data. Modern infrastructure must include 3D Secure 2.0 to verify identities and reduce chargebacks. Advanced fraud prevention tools analyze patterns in real time to block suspicious activity before it impacts your bottom line. Tokenization is another essential feature. It replaces card details with unique identifiers, protecting your recurring revenue and customer trust. These layers of defense empower you to focus on expansion while your provider secures every dirham (AED).

Choosing the right partner solves common pain points like delayed settlements and complex setup processes. PaySelect simplifies this journey by offering high-end solutions tailored to the local market. Ready to optimize your setup? Explore our payment gateways to find your perfect fit.

Optimizing Your Bottom Line with PaySelect

Managing business money uae efficiently is the difference between a scaling enterprise and a stagnant one. Many merchants lose 2% to 5% of their revenue to inefficient payment routing and opaque fee structures. PaySelect acts as an independent bridge. It removes the guesswork by connecting businesses with the infrastructure that fits their specific volume and sector. This independence ensures that your choice is based on performance metrics rather than aggressive marketing or biased incentives.

The PaySelect Advantage: Transparency First

Independence is critical in the UAE's competitive payment market. Many providers offer solutions that bundle interchange costs and processing markups into a single, confusing rate. PaySelect doesn't favor one provider over another. It empowers you to negotiate from a position of strength using unbiased comparison data. This transparency allows you to see the real cost of acceptance across different digital channels.

'Data-driven selection is the only way to ensure your payment stack is an asset, not a liability.'

By analyzing raw data, you can choose a partner that supports your 2026 growth targets. This prevents you from overpaying for features your business hasn't reached yet. It also ensures you don't outgrow your provider within six months as your transaction volume increases.

Accelerate Your Business Growth

Speed is a competitive advantage. Traditional onboarding for merchant accounts in the region can take weeks of back and forth documentation. PaySelect streamlines this process. We match you with partners whose compliance requirements and risk appetites align with your business profile. This reduces friction and gets your checkout live in a fraction of the usual time.

For larger organizations, we provide enterprise-scale infrastructure audits. These audits identify leaks in your payment funnel where transactions fail or costs spike. We look at settlement times, currency conversion fees, and local card scheme support. Continuous optimization ensures your setup remains lean as you scale globally.

Take the test today to find the ideal payment partner for your UAE business. Finding the right match takes minutes, but the impact on your money uae strategy is permanent. Our platform simplifies complex financial decisions into actionable steps. Stop guessing and start optimizing.

Master the Future of Commerce in the Emirates

The landscape of managing money uae businesses handle is shifting rapidly toward a digital-first reality. Success in 2026 requires more than just accepting payments; it demands a strategic alignment with infrastructure that minimizes hidden costs and maximizes settlement speed. You've seen how the right pillars of financial management can transform your bottom line from a cost center into a competitive advantage. Selecting a partner shouldn't be a guessing game based on fragmented data or outdated processes.

PaySelect provides the clarity you need to scale with confidence. As specialists in the MENA region, we offer an independent and unbiased comparison of the market's leading solutions. Our expert advisory services are designed for enterprise optimization, ensuring your setup is lean, compliant, and ready for borderless growth. Don't let complex fee structures or legacy systems stall your momentum. It's time to streamline your operations and secure your margins with a partner that understands the local landscape.

Compare UAE Payment Gateways and Save on Fees

Your business deserves a financial foundation built for the next decade of digital trade in the Middle East.

Frequently Asked Questions

What is the average transaction fee for businesses in the UAE?

Transaction fees for businesses in the UAE typically range from 2.0% to 3.0% for domestic credit cards, plus a fixed fee of AED 1.00 per transaction. International card processing often incurs higher rates, sometimes reaching 3.9%. These costs directly impact how you manage money uae operations, so selecting a provider with transparent settlement structures is vital to protect your profit margins.

Can I accept international payments in the UAE Dirham (AED)?

You can accept international payments in UAE Dirham (AED) through most modern payment gateways. This allows global customers to pay in their own currency while you receive the settlement in AED. It eliminates currency conversion friction, improves checkout conversion rates, and simplifies your local accounting. This borderless approach ensures your business remains competitive in a global marketplace while maintaining local financial clarity.

How long does it take to set up a payment gateway for a new business?

Setting up a payment gateway for a new business generally takes between 2 and 7 working days. This timeline depends on the speed of your documentation review and the complexity of your technical integration. PaySelect streamlines this process by offering unified APIs and clear compliance guidance. This allows you to launch, integrate, and scale without the traditional delays associated with legacy banking systems.

Is it better to use a local UAE bank or a specialized fintech provider?

Local UAE banks offer high security and established regional roots, while fintech providers prioritize rapid integration and superior user experiences. Fintechs often provide more agile API documentation and faster onboarding compared to traditional institutions. Your choice depends on whether you value a long term banking relationship or the technical flexibility needed to optimize your digital sales funnel and accelerate growth.

What are the requirements to get a POS machine for my business?

To obtain a POS machine, you must provide a valid UAE trade license, a corporate bank account statement, and proof of a physical business location. Providers also require copies of the owner's Emirates ID and passport. These requirements ensure compliance with Central Bank regulations. Having the right hardware allows you to accept face to face payments, sync your inventory, and provide a seamless customer experience.

How do I reduce the cost of cross-border money transfers?

You can reduce cross-border costs by using payment providers that offer local settlement accounts and competitive exchange rates. Traditional wire transfers often include hidden fees, but modern infrastructure uses smart routing to bypass intermediary banks. This optimization ensures more revenue stays in your business, making it easier to manage money uae entities send to international suppliers or global headquarters.

What happens if my business transaction volume suddenly increases?

If your transaction volume suddenly increases, a scalable payment infrastructure will automatically handle the load without service interruptions. Legacy systems might trigger manual fraud reviews or temporary account freezes during unexpected peaks. PaySelect helps businesses navigate these transitions by providing robust risk management tools. This ensures your checkout remains active, your revenue flows uninterrupted, and your customer trust stays intact.

Are digital wallet payments like Apple Pay and Google Pay standard in the UAE?

Digital wallet payments like Apple Pay and Google Pay are now a standard expectation for consumers in the UAE. Recent market data indicates that over 50% of online transactions in the region are completed using mobile wallets. Integrating these options into your payment flow reduces checkout friction, increases security through biometric authentication, and empowers your business to meet the demands of a tech savvy audience.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.