A headline rate of 1.9% sounds like a victory until hidden monthly minimums and cross-border surcharges erode your margins. This payment gateway cost comparison uae guide reveals why the cheapest sticker price often hides the most expensive infrastructure. You've likely felt the frustration of opaque Merchant Discount Rates, setup fees that drain capital, and settlement cycles that stall your cash flow. It's a common hurdle for businesses aiming to scale in the Emirates, where the digital economy moves faster than the fine print.

We know that making sense of fragmented fee structures is a full-time job you didn't sign up for. PaySelect provides the clarity you need by offering an independent look at the market, helping you identify the right fit without the bias of a direct processor. You'll master the complexities of transactional fees and discover how to optimize your payment infrastructure through our expert-led comparison. This guide provides a clear breakdown of potential costs and a framework to compare provider models. You will learn to reduce friction, improve margins, and prepare your business for the critical regulatory shifts arriving in 2026.

Key Takeaways

• Learn to decode the Merchant Discount Rate (MDR) and identify how hidden fees impact your total cost of ownership.

• Compare the rapid onboarding of aggregator models against the long-term margin benefits of direct bank integrations.

• Execute a comprehensive payment gateway cost comparison uae to mitigate the impact of cross-border fees and FX margins.

• Understand how different settlement cycles affect your business liquidity and discover strategies to accelerate cash flow.

• Utilize independent, data-driven matching tools to remove provider bias and select the optimal infrastructure for your specific needs.

The UAE Payment Landscape: Why Cost Comparison is Critical in 2026

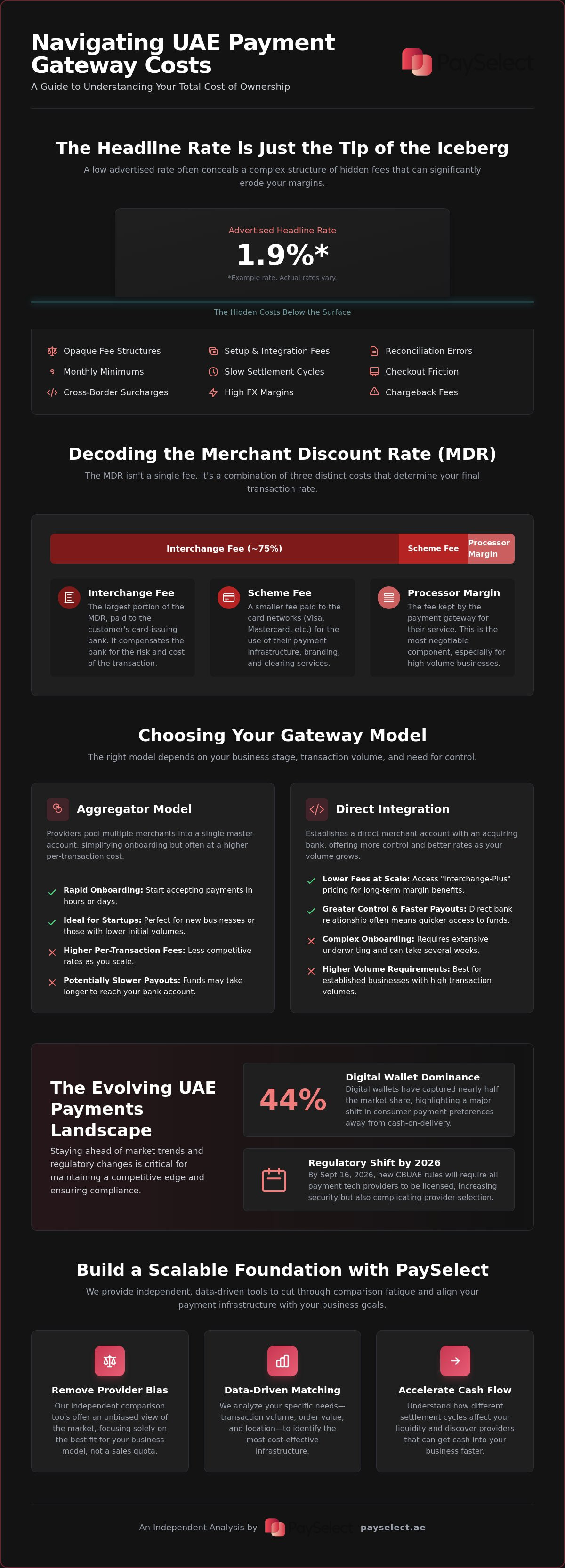

The UAE digital economy has transitioned from a rapid growth phase to a period of sophisticated maturity. Over the last three years, digital wallets have captured nearly 44% of the market share, while traditional cash-on-delivery continues its steady decline. By September 16, 2026, new Central Bank of the UAE (CBUAE) regulations will mandate that every technology provider in the space holds a specific license. This regulatory shift ensures security, but it also complicates the pricing models businesses must navigate. Understanding What is a Payment Gateway? and how its cost structure integrates with your specific business model is no longer optional; it's a requirement for survival.

Relying on a "one-size-fits-all" gateway is a primary driver of margin leakage. Many merchants accept a standard rate without realizing that their specific transaction volume, average order value, and customer location could qualify them for significantly better terms. A thorough payment gateway cost comparison uae allows you to move beyond simple transaction processing. Modern infrastructure now functions as an integrated financial ecosystem that handles automated reconciliation, multi-currency support, and complex cross-border settlements. Transparency in these costs acts as a direct catalyst for your business expansion.

The High Cost of Inefficiency

Inefficiency in your payment stack creates silent drains on your capital. Fragmented systems lead to three major bottlenecks: increased administrative manual work, reconciliation errors that hide losses, and checkout friction that kills conversion rates. When a system isn't optimized for the local market, you don't just lose money on fees. You lose customers who expect seamless, instant transactions through platforms like Aani or local digital wallets. High friction at the final stage of the journey is the fastest way to erode your marketing ROI and impact customer retention.

Strategic Facilitation: The Role of Independent Data

Most information in the payments sector comes directly from the providers themselves. This naturally includes a bias toward their own fee structures. Breaking free from brand loyalty requires a shift toward data-driven infrastructure decisions. At PaySelect, we act as an independent facilitator, providing the tools needed to audit your current stack without the pressure of a sales pitch. By using our "Take the Test" tool, you can cut through comparison fatigue and align your payment strategy with your broader business transformation goals. Moving to an optimized payment gateway setup isn't just about saving a few fils per transaction; it's about building a scalable foundation for international ambition.

Decoding the Fee Structure: Understanding Your Total Cost of Ownership

The Merchant Discount Rate (MDR) is the percentage-based fee charged by acquirers for processing debit and credit card transactions. While this is the most visible number, it's merely the surface of a multi-layered cost engine. To optimize your margins, you must dissect the three primary components: interchange fees paid to the card-issuing bank, scheme fees paid to the card networks, and the processor’s own margin. As highlighted in the UAE e-commerce market overview, the surge in digital transactions means even a 0.1% variance in these layers can translate to thousands of dirhams in annual leakage.

Negotiating competitive rates depends heavily on your transaction volume. Providers often offer tiered pricing models where the MDR decreases as your monthly processing value hits specific milestones. High-volume merchants can often move from a flat-rate model to an "interchange-plus" structure, which offers greater transparency and lower overall costs. Conducting a thorough payment gateway cost comparison uae allows you to identify which tier your business currently occupies and where you have leverage to reduce overhead.

Transactional and Recurring Costs

Fixed costs can be as impactful as variable ones. Many providers charge a flat per-transaction fee, often ranging from AED 0.25 to AED 1.00. For businesses with low average order values, such as digital content creators or quick-service kiosks, these fixed fees can consume a disproportionate share of the profit. Conversely, for high-value retailers—for example, if you visit Budget Gamer UAE to look at high-performance gaming PCs—the percentage-based MDR is the more critical factor to negotiate. You must also weigh the benefits of monthly subscription models against pay-as-you-go structures. A monthly fee of AED 200 might seem like a burden, but it often unlocks lower transaction percentages that save money once you surpass a specific revenue threshold. Setup fees, while less common in 2026, are still used by some institutional partners to cover the technical rigors of direct integration and compliance onboarding.

The Fine Print: Refunds and Chargebacks

The true cost of ownership extends to how a provider handles unsuccessful or reversed sales. Most gateways do not return the original transaction fee when you issue a refund. Some even charge an additional administrative fee to process the reversal. Chargebacks are even more costly. Beyond losing the sale value, you face administrative penalties that can range from AED 50 to AED 100 per instance. These costs are often omitted from marketing materials but are vital for risk management. You can learn more about optimizing your payment gateway selection to ensure these factors don't derail your growth. If you're unsure where your current stack stands, a payment pricing comparison can help identify immediate saving opportunities.

Comparing Payment Gateway Models: Aggregators vs. Direct Integration

Establishing a merchant infrastructure requires a strategic choice between two primary operational models. Your decision dictates your speed to market, your technical overhead, and your long-term profitability. In the Emirates, businesses typically choose between the agility of an aggregator or the deep efficiency of a direct bank integration. A comprehensive payment gateway cost comparison uae must look beyond the individual fees to the structural impact each model has on your balance sheet. Choosing the wrong path early on can lead to expensive migrations as your transaction volume scales.

Hybrid solutions have also emerged to bridge this gap. These providers offer the intuitive interfaces of an aggregator while allowing you to bring your own merchant account from a local bank. This flexibility allows for enterprise-grade scalability without sacrificing the user experience. Evaluating the technical stack requirements is essential. You must consider whether your team can manage custom API integrations or if you require a hosted checkout page that handles the heavy lifting of security and compliance.

Aggregators: The Speed-to-Market Choice

Startups and SMEs favor the aggregator model for its rapid deployment. You don't need a separate merchant account at a local bank; instead, you process transactions under the provider's umbrella. This allows for onboarding in days rather than weeks. For specialized organizations, such as those using music service management software to manage performing arts services, this agility is crucial. The trade-off is a higher transaction fee, often structured as a flat percentage plus a fixed AED amount. However, this model includes built-in fraud protection, hosted checkout pages, and immediate support for digital wallets. It's the ideal choice for businesses prioritizing speed and low upfront complexity over the absolute lowest transaction rate.

Direct Integration: The Enterprise Path

As your revenue grows, the higher fees of an aggregator become a significant cost center. This is when a transition to a direct relationship with an acquiring bank becomes a strategic necessity. Direct integration offers the lowest possible rates because you bypass the aggregator's margin. However, the technical and regulatory complexity is much higher. You must manage your own PCI DSS v4.0 compliance and often utilize a payment switch to manage multiple direct connections. This model provides superior control over your settlement cycles and data. It's also worth considering how your physical POS systems integrate with your online gateway to create a unified view of your commerce. For a tailored look at which model fits your current volume, you can compare provider models through our independent platform.

Beyond the Headline Rate: Hidden Costs and Optimization

Focusing solely on the advertised transaction rate is a strategic oversight that often leads to unexpected overhead. A comprehensive payment gateway cost comparison uae must account for the secondary layers of the payment stack that quietly erode profitability. These costs include currency conversion spreads, international card surcharges, and the technical debt associated with maintaining security standards. For a business processing millions in AED, a 1% margin on foreign exchange (FX) is far more damaging than a slightly higher monthly subscription fee.

Security compliance also carries a price tag. Maintaining PCI DSS v4.0 standards is mandatory for merchants handling sensitive data, and the cost of regular audits or secure data residency can be substantial. Additionally, the retirement of SMS-based One-Time Passwords (OTPs) by March 2026 requires providers to shift toward biometric authentication. This transition involves technical updates that may be passed down as "service enhancement" fees. True optimization requires looking past the surface to see how these variables interact with your specific business model.

Optimizing Cross-Border Transactions

International sales introduce a layer of complexity known as the FX margin. When a customer pays in a foreign currency, gateways often apply a conversion spread that can range from 1% to 3% above the mid-market rate. If your business targets the wider GCC, you must ensure your provider supports local card schemes like Mada in Saudi Arabia or KNET in Kuwait. Processing these through regional channels is significantly more cost-effective than routing them as international credit card transactions. You can discover strategies for cross-border payments optimization that minimize these hidden surcharges and improve your global competitiveness.

Operational Efficiency and Cash Flow

Settlement speed is the engine of your business liquidity. Settlement cycles represent the duration between a successful customer transaction and the actual deposit of those funds into your business bank account. While some providers offer T+1 (next day) cycles, others may hold funds for T+7 or longer, effectively trapping your working capital. This delay creates a cash flow gap that can hinder your ability to restock inventory or fund marketing campaigns. Automating your reconciliation process is another critical step. By choosing a provider that integrates directly with your accounting software, you reduce the manual overhead and errors associated with fragmented data. If you are ready to identify these leaks in your current infrastructure, you can request a payment cost optimization audit to secure your margins.

Executing Your Strategy: How PaySelect Facilitates Optimal Selection

Execution requires more than just data; it requires a framework for decision-making. PaySelect provides this through an independent lens that prioritizes merchant needs over provider margins. The "Take the Test" tool is the primary entry point for merchants seeking to bypass comparison fatigue. By inputting specific business metrics, you receive a curated match that aligns with your operational goals. This data-driven approach removes the bias inherent in provider-led content, ensuring that your payment gateway cost comparison uae results in a stack that actually enhances your bottom line. We act as the bridge between technical complexity and commercial success.

For large-scale organizations, cost leakage is often systemic rather than isolated. It's not just about a single transaction rate; it's about the interaction between multiple providers and legacy systems. Our bespoke infrastructure audits identify these overlaps and redundancies. We focus on the concept of fluidity. Your payment stack shouldn't be a static cost center that limits your potential. It should be a dynamic tool that scales as you move into new markets or adopt new sales channels like POS systems or social commerce links. Removing these operational barriers is the first step toward international expansion.

Tailored Solutions for Every Scale

SMEs often struggle with the sheer volume of fragmented data in the UAE market. We simplify this landscape by presenting transparent, side-by-side comparisons that highlight the total cost of ownership. At the enterprise level, the focus shifts to optimization and negotiation. Our independent advisory helps you leverage your transaction volume to secure better terms from acquiring banks. PaySelect maintains a commitment to worldly, results-oriented guidance that prioritizes your business outcome over provider relationships. We ensure that every dirham spent on processing is an investment in your growth.

Start Your Optimization Journey

Before you begin an audit, gather your core transactional data. You need your average monthly volume, your average order value (AOV), and a breakdown of local versus international transactions. This information allows PaySelect to bridge the gap between complex global infrastructures and your intuitive business needs. Our independent platform ensures your payment gateway cost comparison uae is based on reality, not marketing promises. Join the sophisticated businesses that are already using our payment gateway comparison tool to remove operational barriers. Start your journey toward a frictionless financial future today.

Future-Proof Your Payment Infrastructure

Success in the national digital economy depends on moving beyond headline rates to optimize every layer of your transaction flow. We've explored how opaque fee structures and the 2026 regulatory shifts demand a more sophisticated approach to merchant services. Protecting your liquidity requires a rigorous payment gateway cost comparison uae that accounts for settlement cycles, FX margins, and the technical demands of local compliance. Your payment stack should act as a catalyst for growth, not a silent drain on your margins.

PaySelect provides the clarity you need through independent, unbiased comparisons and expert infrastructure advisory. We specialize in the unique conditions of the UAE market, helping you bridge the gap between complex global systems and your intuitive business needs. Take the Test and optimize your payment costs to ensure your technology stack is ready for international expansion. The digital landscape is moving fast. Secure your position as a market leader with a payment strategy built for performance and scale.

Frequently Asked Questions

How much does a payment gateway typically cost in the UAE?

Costs depend on your business model and transaction volume. Most providers charge a Merchant Discount Rate (MDR) between 2.0% and 3.0%, often paired with a fixed fee of AED 0.50 to AED 1.00 per transaction. Some models include monthly maintenance fees starting from AED 100, while others offer pay-as-you-go structures. A thorough payment gateway cost comparison uae is essential to identify the most efficient total cost of ownership for your specific profile.

What is the difference between an aggregator and an acquiring bank?

Aggregators allow you to process payments under their umbrella without a separate merchant account, offering rapid onboarding and simple pricing. Acquiring banks provide a direct relationship with the financial institution, which typically results in lower transaction rates but requires higher technical integration and stricter regulatory compliance. While aggregators suit startups looking for speed, established enterprises often prefer direct bank integration to maximize their long-term profit margins and control over funds.

Are there hidden fees associated with international credit cards?

International transactions often carry additional surcharges and foreign exchange (FX) margins that aren't always transparent. Most gateways add 1% to 2% on top of the standard local rate for cards issued outside the UAE. You may also encounter FX conversion spreads when settling funds in AED from a foreign currency transaction. These costs are rarely highlighted in headline rates, making it vital to audit your cross-border processing fees to prevent margin erosion.

How long does it take for funds to be settled into my UAE bank account?

Settlement cycles in the UAE typically range from T+1 (next business day) to T+7 (seven days after the transaction). The speed depends on your provider's risk assessment, your business industry, and the type of integration you use. Faster cycles improve your business liquidity but may come with higher service fees or stricter eligibility requirements. Understanding these timelines is critical for managing your working capital and ensuring a smooth operational flow.

Do I need a special license to accept online payments in the UAE?

You need a valid UAE trade license to operate an e-commerce business and accept payments. While the merchant doesn't need a specific "payment license," your chosen provider must be licensed by the Central Bank of the UAE. By September 16, 2026, all technology providers in this space must comply with updated CBUAE licensing frameworks. Ensuring your infrastructure partners meet these regulatory standards is essential for long-term operational security and maintaining consumer trust.

What is MDR and how is it calculated for my business?

The Merchant Discount Rate (MDR) is the percentage fee charged on every successful transaction processed through your gateway. It's calculated based on three components: interchange fees, scheme fees, and the processor's margin. Your specific rate is often determined by your industry risk profile, average order value, and monthly processing volume. Performing a payment gateway cost comparison uae helps you understand how these variables influence your final rate and where you have leverage to negotiate.

Can I negotiate my transaction fees as my volume increases?

Negotiation is common once your business reaches significant transaction milestones. Most providers offer tiered pricing where the MDR decreases as your monthly processing volume increases. High-growth businesses can often move from flat-rate aggregator models to customized interchange-plus pricing. This transition allows you to capture more value from your scale and significantly reduce your annual processing overhead. Professional audits and data-driven insights are key to securing these improved terms effectively.

How does PaySelect help me choose the right provider without bias?

PaySelect operates as an independent digital platform that doesn't provide processing services, removing any conflict of interest. We use a data-driven approach, including our specialized matching tool, to align your business with the most efficient providers in the MENA landscape. Our focus is on providing bespoke infrastructure audits and strategy development that prioritize your business outcomes. We act as a worldly facilitator, ensuring your payment stack is optimized for both performance and expansion.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.