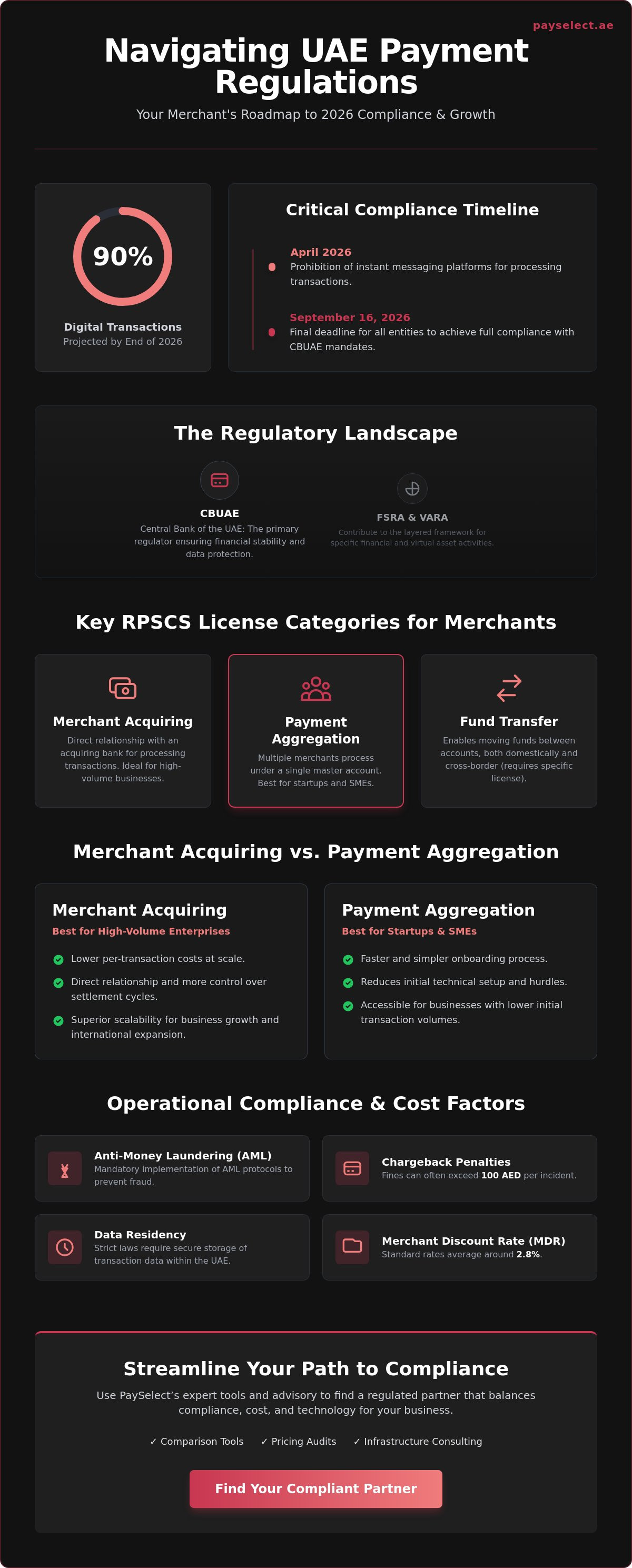

By the end of 2026, 90% of all transactions in the UAE will be digital, leaving no room for error in your financial infrastructure. You're likely feeling the pressure of the September 16, 2026, compliance deadline while trying to decode the complex differences between RPSCS and SVF licenses. It's frustrating when updates like the April 2026 prohibition of instant messaging for transactions feel like hurdles rather than help. Understanding the latest payment gateway regulations uae isn't just a legal necessity; it's a strategic move to protect your revenue and scale your operations.

We agree that the layered framework of CBUAE, FSRA, and VARA can feel overwhelming for any merchant. This guide provides a clear roadmap to ensure you remain compliant, secure, and ready for expansion. You'll learn how to manage AML requirements, optimize the standard 2.8% MDR, and avoid chargeback penalties that often exceed 100 AED. We'll break down the essential licensing tiers and show you how PaySelect's comparison tools, pricing audits, and infrastructure consulting help you choose a regulated partner that streamlines your path to a borderless economy.

Key Takeaways

• Master the architecture of the UAE Payment Gateway System (UAEPGS) to align with the Central Bank’s mandate for domestic digital transactions.

• Identify which of the nine retail payment service categories fits your business model. This helps you navigate payment gateway regulations uae without the risk of non-compliance penalties.

• Protect your business by implementing mandatory Anti-Money Laundering (AML) protocols and adhering to data residency laws for secure transaction storage.

• Learn how to verify a provider’s license status through official portals and evaluate technical resilience as a critical compliance factor.

• Streamline your search for a compliant partner. Use PaySelect’s comparison tools to find solutions that balance regulatory excellence with cost optimization.

The UAE Payment Gateway Regulatory Landscape in 2026

The UAE's financial sector has undergone a massive transformation, positioning itself as a global leader in digital commerce. By 2026, the UAE Payment Gateway System (UAEPGS) has become the definitive national backbone for all online transactions. This system ensures that payments are fast, secure, and settled with absolute precision across the Emirates. The shift from traditional banking laws to modern, fintech-first payment gateway regulations uae reflects the nation's ambition to facilitate a truly borderless economy.

This regulatory evolution isn't just about oversight; it's about creating a foundation for instant settlements and high-volume scaling. All entities must achieve full compliance with the updated Central Bank mandates by September 16, 2026. This deadline marks a milestone where the UAE moves beyond legacy frameworks into a real-time, transparent financial ecosystem. For merchants, this means the choice of a payment partner now carries significant legal and operational weight.

The Authority of the CBUAE

The Central Bank of the UAE (CBUAE) serves as the primary regulator, wielding a mandate to ensure financial stability and protect consumer data. Its role has shifted from periodic auditing to proactive, real-time supervision. The CBUAE now monitors digital payment flows and participant behavior through sophisticated reporting interfaces. This transition helps prevent fraud and ensures that every licensed provider maintains the liquidity and security standards required to operate in the UAE's high-growth market.

Key Regulatory Milestones for Merchants

Two critical frameworks define the current landscape for any business accepting digital dirhams. The Retail Payment Services and Card Schemes (RPSCS) Regulation provides a structured breakdown of nine primary service categories. This ensures that payment providers operate within specific boundaries, whether they handle merchant acquiring or simple payment processing. Additionally, the Stored Value Facilities (SVF) framework governs digital wallets, ensuring that funds are backed by secure reserves.

These regulations are the driving force behind the Dubai Cashless Strategy, which targets a 90% digital transaction rate by the end of 2026. Adhering to these standards protects your business from heavy non-compliance fines and builds trust with a tech-savvy customer base. PaySelect streamlines this process by offering a payment gateway comparison tool that filters providers based on their specific CBUAE license type. We act as your strategic partner, helping you identify infrastructure that turns regulatory compliance into a competitive advantage for your business.

Licensing Categories and Compliance Standards

Success in the Emirates requires a deep understanding of the 2026 Retail Payment Services and Card Schemes (RPSCS) Regulation. This framework divides the industry into nine distinct categories, ensuring every participant operates with maximum transparency. For merchants, the most critical categories include Merchant Acquiring Services, Payment Aggregation Services, and Fund Transfer Services. These payment gateway regulations uae dictate how your provider handles your money, how quickly you receive settlements, and the level of risk your business carries.

Choosing a provider without verifying their specific category can lead to operational bottlenecks. For instance, a provider licensed only for domestic fund transfers cannot legally facilitate your international expansion. If you're looking to scale beyond borders, you must partner with an entity licensed for Cross-border Fund Transfer Services. This ensures your transactions remain compliant with both local mandates and international standards, protecting your business from sudden service interruptions.

Merchant Acquiring vs. Payment Aggregation

High-volume enterprises typically thrive with a direct Merchant Acquiring model. This setup provides a direct relationship with the acquiring bank, often resulting in lower per-transaction costs and more control over settlement cycles. Startups and SMEs, however, frequently find the Payment Aggregation model more accessible. Aggregators allow multiple merchants to process payments under a single master account, which simplifies the onboarding process and reduces initial technical hurdles. While aggregation is faster to set up, direct acquiring offers superior scalability and lower long-term costs as your volume grows.

Capital and Governance Requirements

The CBUAE has implemented strict financial cushions to ensure the stability of the digital economy. As of February 2026, licensed providers must meet rigorous capital requirements to prove their resilience. For Virtual Asset Service Providers (VASPs), these capital thresholds range from AED 500,000 to AED 4 million, depending on the scope of their services. Beyond capital, providers must maintain robust corporate governance and risk management frameworks to identify and mitigate potential financial threats in real-time.

Aggregate Capital Funds represent the permanent, unimpaired paid-up capital that a licensed provider must maintain at all times to absorb potential operational losses. This requirement ensures that your chosen provider remains a rock-solid partner even during market volatility. To ensure your infrastructure aligns with these high standards, you can use our payment gateway comparison tool to evaluate providers based on their regulatory standing and capital stability. This helps you avoid the pain of migrating platforms later due to a provider's failure to meet evolving CBUAE benchmarks.

Operational Impact: Security, Data, and AML

Compliance is the engine of your business, not just a checkbox. In 2026, payment gateway regulations uae mandate a zero-tolerance approach to digital security. The Federal Decree-Law No. 20 of 2018 remains the primary legislation for Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT). You must ensure your provider uses real-time screening to flag suspicious activities instantly. This protects your revenue from being tied to illicit transactions and avoids the heavy fines associated with non-compliance.

Data residency is another non-negotiable pillar. Under the UAE Federal Decree-Law No. 45 of 2021 (PDPL), sensitive financial data must be stored within the UAE. Your gateway must prove that transaction data doesn't leave the country without specific authorization. The integration of PCI-DSS v4.0 into national law means that advanced encryption and tokenization are now baseline requirements. These technologies replace card data with unique digital identifiers, ensuring that even if a breach occurs, the information is useless to hackers.

Know Your Customer (KYC) and Onboarding

Onboarding in 2026 is faster but more rigorous. You'll need a valid UAE trade license, proof of physical address, and corporate bank account details. The integration of the UAE PASS digital ID system has streamlined this, allowing for instant identity verification while meeting payment gateway regulations uae standards. If your business operates in a high-risk sector, expect "enhanced due diligence." This involves deeper scrutiny of your source of funds and transaction patterns to ensure complete transparency within the UAE financial ecosystem.

Consumer Protection and Dispute Resolution

Transparency is the cornerstone of the CBUAE's consumer protection framework. You must provide clear fee disclosures to your customers at the point of sale. This includes any surcharges or processing fees, keeping in mind that the standard MDR is approximately 2.8% plus 1.00 AED per transaction. When disputes arise, the process is strictly regulated. Chargeback penalties can exceed 100 AED, making it vital to have a clear refund policy. The Financial Ombudsman serves as the final authority, ensuring that both merchants and consumers are treated fairly under the law.

Managing these operational requirements doesn't have to slow you down. PaySelect's payment gateway comparison tool helps you filter providers by their security certifications and data residency status. We simplify the selection process so you can focus on scaling your business with confidence.

Criteria for Selecting a Compliant Payment Partner

Selecting a payment partner in the Emirates requires a shift from price-focused to compliance-first thinking. Your gateway is the bridge between your revenue and the CBUAE's oversight. To ensure your business isn't disrupted, you must verify that your chosen provider holds the correct license for their specific service tier. This verification isn't optional; it's a fundamental step in adhering to payment gateway regulations uae and protecting your brand's reputation.

A compliant partner provides more than just a checkout page. They offer technical resilience, ensuring uptime that meets the Central Bank’s rigorous standards for financial participants. You need a provider that offers automated settlement reporting and transparent fund disbursement timelines. In a market where digital transactions are becoming the norm, any delay in settlement can cripple your liquidity and hinder your ability to scale.

The Merchant Due Diligence Framework

Start by checking the CBUAE official portal to confirm a provider's status. A valid license is the only guarantee that the entity is authorized to handle your funds. Use this checklist during your vetting process:

• Confirm the license type matches your business model, such as SVF for digital wallets or RPSCS for standard acquiring.

• Request their latest PCI-DSS v4.0 certification and SOC2 audit reports to verify data security.

• Ensure they host data within the UAE to comply with PDPL residency laws.

• Review contracts for "regulatory surcharge" clauses that might hide costs or fees.

Watch for red flags like a lack of clear documentation on AML protocols or an inability to explain how they handle the April 2026 prohibition on using instant messaging for transactions.Integration and Scalability

Modern infrastructure relies on API-led compliance. This technical approach allows your gateway to implement regulatory updates, such as the 2026 PTSR stablecoin standards, without requiring you to rewrite your code. It's about maintaining a seamless user experience while implementing mandatory security friction. For example, 3D Secure (3DS) is a requirement for fraud prevention, but a sophisticated partner will use frictionless 3DS to minimize cart abandonment. By comparing payment gateways through a strategic lens, you can find a partner that balances technical excellence with rock-solid reliability.

Ready to optimize your infrastructure? Use our Payment Gateway Comparison Tool to find a partner that meets every regulatory benchmark while accelerating your growth.

Optimizing Compliance with PaySelect’s Advisory

Navigating the intricate payment gateway regulations uae requires more than just a list of licensed providers. It demands an independent perspective that prioritizes your business's specific growth trajectory. PaySelect serves as that essential bridge, translating complex Central Bank mandates into actionable infrastructure choices. We don't process your payments; we empower you to choose the partner that does it best. This independence ensures you receive unbiased data, allowing you to bypass biased sales pitches and focus on technical resilience.

Our "Take the Test" tool is designed to eliminate the guesswork. By inputting your business model, transaction volume, and expansion goals, you're matched with providers that satisfy 2026's rigorous standards. For enterprise-scale operations, our fixed-fee advisory services offer deep-dive infrastructure audits. These audits identify hidden costs and compliance gaps, ensuring your stack is ready for the September 16, 2026, compliance deadline. This structured approach significantly reduces time-to-market, letting you launch new ventures with the confidence that your payments are secure and scalable.

Independent Comparison and Transparency

In a market where 90% of transactions in Dubai will be digital by the end of 2026, transparency is your greatest asset. PaySelect provides the clarity you need to avoid providers with inconsistent service records or outdated security protocols. We analyze the differences in MDR, settlement speeds, and technical support across the industry. If your roadmap includes international markets, our payment infrastructure consulting ensures you meet the payment gateway regulations uae and international requirements for every jurisdiction you enter.

The Path to Borderless Growth

Scaling across the GCC requires a payment stack that's both flexible and compliant. By leveraging PaySelect’s comparison tools, you can optimize your costs without sacrificing the elite security standards mandated by the CBUAE. We help you find solutions that integrate local schemes while maintaining the robust AML/CFT protocols required for global trade. Don't let regulatory complexity stall your ambition. It's time to build a frictionless, high-performance financial foundation that turns compliance into a strategic advantage. Optimize your payment infrastructure today and secure your place in the UAE's digital future.

Secure Your Future in the UAE Digital Economy

The roadmap to 2026 is clear. The September 16 compliance deadline isn't just a regulatory hurdle; it's an opportunity to build a rock-solid foundation for your brand. Success requires mastering the nuances of licensing tiers and ensuring your data residency aligns with the latest PDPL mandates. By adapting to the evolving payment gateway regulations uae, you protect your revenue and gain the trust of a market aiming for 90% digital transaction adoption by the end of the year.

You don't have to navigate this complex landscape alone. PaySelect provides the independent advisory enterprise-scale organizations need to scale with confidence. Our expert-led payment cost optimization audits and deep expertise in MENA fintech regulations ensure your infrastructure remains efficient and compliant. We bridge the gap between technical requirements and strategic business outcomes. Match with the most compliant UAE payment gateways now and accelerate your journey toward borderless growth. Your ambition deserves a partner that values security as much as speed. Let's build your global reach together.

Frequently Asked Questions

Who is the main regulator for payment gateways in the UAE?

The Central Bank of the UAE (CBUAE) is the primary regulator for the mainland financial sector. It mandates that all entities achieve full compliance with the new Central Bank law by September 16, 2026. While the CBUAE handles national oversight, specialized zones like the DIFC and ADGM have their own authorities, the DFSA and FSRA. Dubai's Virtual Asset Regulatory Authority (VARA) manages virtual asset service providers under Rulebook 2.0.

Do I need a specific license to accept online payments for my UAE business?

You must possess a valid UAE trade license to integrate a payment gateway and process local transactions. While your business doesn't need a financial service license, your gateway provider must be authorized by the CBUAE. This setup ensures your operations align with anti-money laundering mandates and national security standards. Without a local license, you'll struggle to find a regulated partner willing to facilitate AED settlements.

What is the RPSCS Regulation and how does it affect small businesses?

The Retail Payment Services and Card Schemes (RPSCS) Regulation defines nine primary categories of payment services. For small businesses, this framework ensures that your chosen aggregator or gateway operates with sufficient capital reserves and robust governance. It protects you from provider insolvency and ensures that transaction processing remains transparent. This regulation is a cornerstone of the payment gateway regulations uae that merchants must understand to scale securely.

Is it mandatory for payment data to be stored within the UAE?

Sensitive financial and personal data must be stored within the UAE to comply with data localization rules. Federal Decree-Law No. 45 of 2021 on the Protection of Personal Data (PDPL) requires explicit consent for data processing. While some data can move across borders, your payment provider must prove that they implement the high security measures required to keep Emirati consumer information safe from international breaches.

What happens if a payment gateway provider loses its CBUAE license?

If a provider loses its CBUAE license, it must immediately stop processing payments and handling merchant funds. This results in frozen settlements and a complete halt to your online checkout process. It's a significant operational risk that can cripple your liquidity. To avoid this, use PaySelect's comparison tools to verify that your partner meets the capital requirements, which range from AED 500,000 to AED 4 million.

How often do UAE payment regulations change?

UAE regulations evolve rapidly to mirror the fast-paced digital economy. Significant updates occur whenever new technologies like stablecoins or open finance emerge. In 2026 alone, we've seen the April prohibition on using WhatsApp for transactions and the September 16 deadline for full law compliance. Staying updated is vital as the Dubai Cashless Strategy pushes toward a 90% digital transaction goal by the end of 2026.

Can I use an international payment gateway for my UAE-based company?

You can use an international gateway, but it must be licensed or partnered with a local bank to process AED transactions legally. Many international providers struggle with local payment gateway regulations uae, leading to high currency conversion costs and settlement delays. Merchants often find that localized gateways offer more cost-effective options, especially when integrating local schemes like Jaywan to avoid the standard 2.8% MDR on domestic payments.

What are the AML requirements for UAE e-commerce merchants?

Merchants must adhere to Federal Decree-Law No. 20 of 2018 regarding Anti-Money Laundering (AML). This requires you to implement Know Your Customer (KYC) protocols, report suspicious activities, and maintain detailed transaction records. Your gateway partner facilitates this by providing automated screening tools. Compliance isn't just about avoiding fines; it's about ensuring your business isn't used as a conduit for illicit financial flows in a borderless economy.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.