The UAE faces up to 200,000 cyber breach attempts every single day, turning payment security into a high-stakes strategic priority. For many entrepreneurs, the technical PCI DSS compliance requirements for sme in uae feel like an impenetrable maze of jargon and potential fines. You're likely balancing the 12 core requirements while trying to figure out exactly where your payment gateway's responsibility ends and your own merchant duties begin.

It's a complex challenge, but securing your transactions shouldn't stall your expansion. This guide helps you master the complexities of PCI DSS 4.0 and discover how to streamline your UAE business payment security for 2026. We'll provide a clear checklist of SME requirements, demonstrate how to reduce your compliance scope, and show you how identifying the right payment infrastructure can simplify the entire process. You'll learn to transform compliance from a technical burden into a competitive advantage for your business.

Key Takeaways

• Navigate the 2026 regulatory shift with confidence by understanding the Central Bank’s latest enforcement measures for UAE businesses.

• Master the 12 core PCI DSS compliance requirements for sme in uae through a simplified framework designed for non-technical business owners.

• Implement scope reduction strategies to minimize your security responsibilities and protect your bottom line from heavy non-compliance fines.

• Map your data flow to identify critical vulnerabilities and streamline the transition to the mandatory version 4.0 standards.

• Leverage specialized comparison tools to find payment infrastructure partners that proactively manage your compliance documentation and security audits.

Understanding PCI DSS Compliance in the UAE Landscape

The Payment Card Industry Data Security Standard (PCI DSS) serves as the global blueprint for protecting sensitive transaction data. It isn't just a technical hurdle; it's a foundational requirement for any business operating in the modern digital economy. In the United Arab Emirates, this standard is driven by the Central Bank to ensure the integrity of the national financial ecosystem. As we move through 2026, the transition to version 4.0 is complete, and acquisition banks are shifting from general education to strict enforcement.

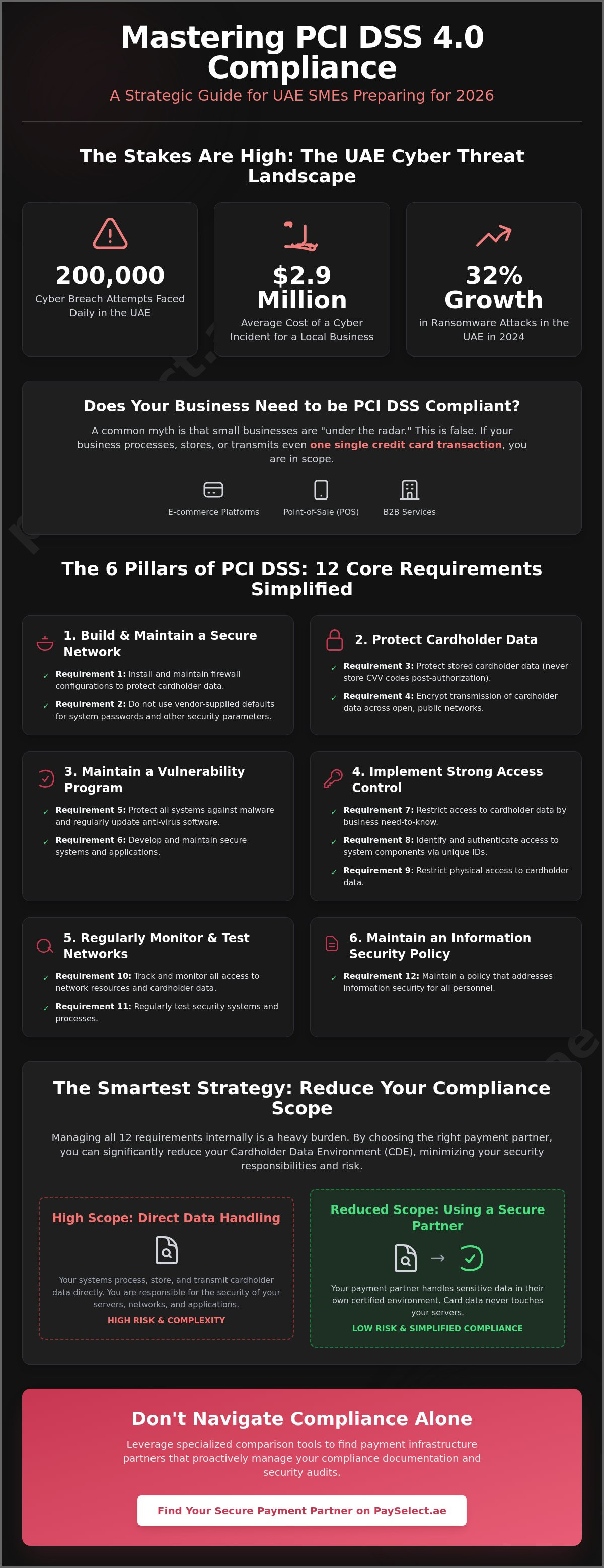

Ignoring these protocols carries massive risk. The UAE faces up to 200,000 cyber breach attempts every single day, and the average cost of a cyber incident for a local business has climbed to $2.9 million. Beyond the immediate financial hit, non-compliance can lead to revoked processing privileges and permanent reputational damage. Meeting the PCI DSS compliance requirements for sme in uae is no longer optional for those who want to scale. It's a strategic move to safeguard your growth and maintain consumer confidence in a high-speed market.

Who Exactly Needs to be Compliant?

A common misconception is that small businesses are "under the radar." This is a dangerous myth. If your business processes, stores, or transmits even a single credit card transaction, you're within the scope of PCI DSS. This applies to high-volume e-commerce platforms, local brick-and-mortar boutiques using POS machines, and B2B service providers. Threat actors don't discriminate based on company size; they look for vulnerabilities. With ransomware attacks in the UAE growing by 32% in 2024, every merchant must prove they've secured their data environment to avoid becoming a statistic.

The Role of the PCI Security Standards Council (PCI SSC)

The PCI SSC is the global body that develops and maintains the security standards. While they set the rules, they don't enforce them directly. In the UAE, that responsibility falls to the acquisition banks and the Central Bank. These institutions mandate that merchants adhere to the council's framework to mitigate systemic risk. It's also vital to distinguish between being compliant and being certified. Compliance means you're meeting the 12 core requirements in your daily operations. Certification involves a formal assessment or Self-Assessment Questionnaire (SAQ) to prove that compliance to your bank. Understanding this distinction is the first step toward building a frictionless, secure payment setup.

The 12 Core Requirements Simplified for UAE SMEs

The 12 requirements outlined by the PCI Security Standards Council (PCI SSC) act as a comprehensive shield for your revenue. These rules are designed to be robust yet adaptable, ensuring your digital and physical storefronts remain resilient against evolving threats. In the current landscape, meeting the PCI DSS compliance requirements for sme in uae is about establishing a culture of continuous security rather than completing a one-time audit.

The framework is built on six secure pillars. You must build and maintain a secure network by installing firewalls and changing all vendor-supplied default passwords. Protecting cardholder data is non-negotiable; this involves encrypting data during transmission and strictly limiting what you store. You also need a vulnerability management program that includes updated anti-virus software and secure system maintenance. Access control is equally vital, requiring you to restrict data access to "need-to-know" personnel and assign unique IDs to every user. Finally, you must regularly monitor and test your networks while maintaining a formal information security policy for all staff.

Achieving this level of oversight can feel overwhelming for a growing team. Many businesses find that the easiest way to manage these technical hurdles is to choose infrastructure that does the heavy lifting for them. You can use a payment gateway comparison tool to identify partners whose systems are already optimized for these 12 requirements, effectively reducing your internal workload.

Protecting the Cardholder Data Environment (CDE)

Your CDE is any part of your business where card data "touches" your systems. To keep this area secure, you must never store sensitive authentication data like CVV codes or full magnetic stripe details after authorization. It's a high-risk practice that makes you a prime target for breaches. Changing default passwords on routers and software is another critical step. Since early 2025, the UAE has recorded over 12,000 Wi-Fi breaches, many of which stemmed from easily guessable credentials. Simple hygiene prevents massive exposure.

Maintaining a Security Policy

A secure business needs an enforceable internal policy. This document shouldn't be a complex manual; it should be a clear set of rules for how your team handles data. Focus on phishing awareness and basic data handling. With ransomware attacks in the UAE growing by 32% in 2024, your employees are your first line of defense. Conduct annual reviews to ensure your protocols stay ahead of new threats and keep your business moving at the speed of the modern economy.

Compliance Levels and Reducing Your Security Scope

Merchant levels dictate your specific reporting obligations and the intensity of your annual validation. For most SMEs in the UAE processing fewer than 1 million transactions annually, Level 4 is the standard. While you won't need an expensive on-site audit by a Qualified Security Assessor, you must still prove you meet the PCI DSS compliance requirements for sme in uae through a Self-Assessment Questionnaire (SAQ). The goal is to move through this process with speed and precision, rather than getting bogged down in technical debt.

This is where the concept of "Scope Reduction" becomes your most valuable strategic tool. Scope refers to any person, process, or technology that touches cardholder data. If you can limit that contact, you limit your liability. By ensuring sensitive data never enters your local network, you drastically shrink the number of security controls you need to manage. It's a shift from defending an entire fortress to simply securing a single, well-protected gate. The PCI Security Standards Council (PCI SSC) provides different SAQ types based on how much of this data you handle, and choosing the right path is essential for operational fluidity.

SAQ A vs. SAQ D: Why the Difference Matters

The questionnaire you complete depends entirely on your integration method. SAQ A is the gold standard for SMEs because it applies when you outsource all data processing to a compliant third party. It’s concise and manageable. On the other hand, SAQ D is the most complex and rigorous version, required if you store or process data on your own servers. Selecting a high-performance payment gateway through a targeted comparison ensures you remain in the SAQ A category. This prevents your business from falling into the "high-scope" trap that demands massive technical resources.

The Benefit of Tokenization and Hosted Payment Pages

Modern infrastructure offers two primary routes to rapid compliance:

Hosted Payment Pages

These redirect your customers to a secure environment managed entirely by your provider. Your website never sees or "touches" the raw card data.

Tokenization

This technology replaces sensitive card numbers with secure digital keys called tokens. These tokens allow you to process recurring payments without the risk of storing actual card digits.

These technologies aren't just security features; they're the fastest route to compliance in the UAE. They remove operational barriers and allow you to focus on growth while your infrastructure handles the heavy lifting of data protection.Practical Steps to Achieving Compliance in 2026

Achieving compliance doesn't require a fleet of IT specialists. It requires a logical, step-by-step approach to visibility. Start by conducting a data flow audit. Map every point where card data enters your business environment. Whether it's an online checkout, a phone order, or a physical terminal, you must know exactly where the data goes. Visualizing this path reveals hidden vulnerabilities and helps you eliminate unnecessary data touchpoints.

Once you've mapped the flow, align your business with a PCI-compliant provider. This is the most effective way to meet PCI DSS compliance requirements for sme in uae without technical overwhelm. After your systems are secure, you'll need to complete your Self-Assessment Questionnaire (SAQ) and sign an Attestation of Compliance (AOC). These documents are your formal declaration that you've implemented the necessary safeguards. Finally, submit these to your acquiring bank to maintain your merchant status and avoid the heavy fines associated with non-compliance.

Finding the right infrastructure for your specific needs shouldn't be a guessing game. You can use our payment gateway comparison tool to identify partners that simplify these administrative hurdles and align with your growth goals.

Selecting Compliant Hardware

Physical security is the foundation of trust for retail and hospitality sectors. Ensure your POS machines are PCI PIN Transaction Security (PTS) approved. Legacy card readers are a major liability in 2026. They lack the sophisticated encryption standards required to block modern skimming techniques. Security isn't just digital; it's physical. You must regularly inspect terminals for tampering and ensure only authorized staff handle payment devices.

Quarterly Network Scans

If your systems are connected to the internet, you likely need quarterly scans by an Approved Scanning Vendor (ASV). These scans search for holes in your external-facing network. Don't panic if a scan returns "high-risk" vulnerabilities. Use the report as a precise roadmap to patch your systems and strengthen your perimeter. Keeping a clear, chronological log of these scans proves a history of diligence during bank audits. Since the deadline for all new PCI DSS 4.0 requirements passed on March 31, 2025, these scans are now a mandatory baseline for maintaining your certification status.

How PaySelect Facilitates Your Compliance Journey

Managing the PCI DSS compliance requirements for sme in uae shouldn't distract you from your core mission. PaySelect acts as an elite facilitator, bridging the gap between high-level regulatory frameworks and your daily operations. We remove operational barriers by matching you with compliance-heavy partners that take the technical burden off your shoulders. Our approach is rooted in efficiency; we help you identify, compare, and implement infrastructure that turns security into a frictionless asset for your brand.

Our platform provides access to a sophisticated payment gateway comparison tool and our "Take the Test" feature. These resources are designed to help you find gateways that handle the most demanding SAQ requirements automatically. For businesses scaling toward Level 2 or Level 1 compliance, we offer payment infrastructure consulting to navigate the transition with absolute confidence. We help you optimize your setup to reduce security overhead, minimize costs, and ensure your system is ready for the high-speed digital economy.

Comparing Gateways Based on Security Features

Not all providers offer the same level of compliance support. PaySelect allows you to filter partners based on robust tokenization tools and built-in assistance for UAE-specific regulations. You can balance cost optimization with high-tier security standards, ensuring you don't overpay for protection you don't need. Our payment cost optimization audit identifies where you can streamline your infrastructure without compromising on the 12 core requirements. Whether you are looking for a POS system selection tool or a payment links comparison, our data-driven insights ensure your technology stack remains both lean and rock-solid.

Strategic Facilitation for Growth

Expanding your brand beyond the local market requires a global perspective on data standards. Secure cross-border payments rely on specific compliance frameworks that vary by region. PaySelect helps you find the right match for international expansion, positioning your commitment to security as a competitive advantage. When your customers know their data is handled according to the highest international protocols, you build the trust necessary for rapid growth. We empower you to view compliance not as a technical hurdle, but as a strategic tool for business transformation that opens doors to new global markets.

Securing Your Future in the UAE Digital Economy

The transition to the latest security standards has transformed compliance from a technical hurdle into a strategic asset for growth. You now know that meeting the PCI DSS compliance requirements for sme in uae is most efficient when you prioritize scope reduction and smart infrastructure selection. By utilizing hosted environments and tokenization, you protect your revenue while focusing on your core operations.

Selecting a partner that matches your transaction volume and security needs is the final step toward total operational fluidity. PaySelect provides independent advisory from MENA payment experts and a transparent comparison of UAE gateway features. We help you find the right match without the administrative friction, allowing you to scale across borders with absolute confidence.

Don't let regulatory complexity slow your expansion. Find a PCI-compliant payment partner with PaySelect’s Comparison Tool today and secure your business for the digital landscape of 2026. Your success depends on reliable systems; we're ready to help you build them with confidence.

Frequently Asked Questions

Is PCI DSS compliance mandatory for small businesses in the UAE?

Yes, compliance is a mandatory requirement for every business in the Emirates that processes, stores, or transmits cardholder data. The Central Bank of the UAE enforces these standards across the entire financial ecosystem to protect national economic integrity. Regardless of your company size or transaction volume, you must adhere to the PCI DSS compliance requirements for sme in uae to legally accept card payments.

How much does PCI DSS compliance cost for an SME?

The total investment for compliance varies based on your merchant level and the complexity of your technical environment. Businesses that outsource their payment processing to high-security providers often face lower costs because they reduce their internal security scope. Your expenses typically include self-assessment fees, potential network scanning costs, and any infrastructure upgrades needed to meet the version 4.0 standards.

What happens if my UAE business fails a PCI DSS audit?

Non-compliance carries severe financial and operational penalties. You may face significant monthly fines from your acquiring bank and a mandatory increase in transaction processing fees. In extreme cases, banks can suspend your ability to accept credit cards entirely. Beyond these immediate costs, a failed audit or subsequent data breach can lead to permanent reputational damage and loss of consumer trust in the competitive local market.

Does my payment gateway make me 100% compliant automatically?

No, a compliant gateway does not grant you automatic 100% compliance. Security is a shared responsibility between the merchant and the service provider. While the gateway secures the data during transmission, your business remains responsible for internal protocols. You must still secure your local hardware, manage employee access levels, and ensure your office Wi-Fi networks meet the PCI DSS compliance requirements for sme in uae.

How often do I need to renew my PCI DSS certification?

You must validate your compliance status every 12 months. This annual renewal involves submitting a fresh Self-Assessment Questionnaire (SAQ) or a Report on Compliance (ROC) to your acquiring bank. Many SMEs also need to conduct quarterly network scans if they have internet-facing systems. Staying on a strict annual schedule ensures that your security measures evolve alongside new cyber threats and shifting regulatory demands.

What is the difference between PCI DSS and UAE Data Protection laws?

PCI DSS is a global industry standard specifically designed to protect credit card information. In contrast, the UAE Federal Decree-Law No. 45 of 2021 on the Protection of Personal Data is a broader legislative framework. It governs the privacy and processing of all personal data for residents within the UAE. While they overlap in their goal of data security, you must satisfy both frameworks to operate legally and securely.

Can I store customer credit card details for recurring billing?

You can facilitate recurring billing, but you should never store raw credit card numbers on your own local servers. The most efficient and secure method is using tokenization provided by your payment partner. This replaces sensitive data with a secure digital token that has no value to hackers. This approach allows you to process repeat transactions while keeping your business in a lower, more manageable compliance category.

What is a Self-Assessment Questionnaire (SAQ) and which one do I need?

The SAQ is a validation tool used by merchants to self-report their compliance with the PCI DSS standard. The specific version you need depends on how you handle card data. SAQ A is typically for e-commerce merchants who completely outsource all data entry to a third party. If you store data locally or use complex integrations, you might require SAQ D, which involves significantly more technical questions and rigorous security controls.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.