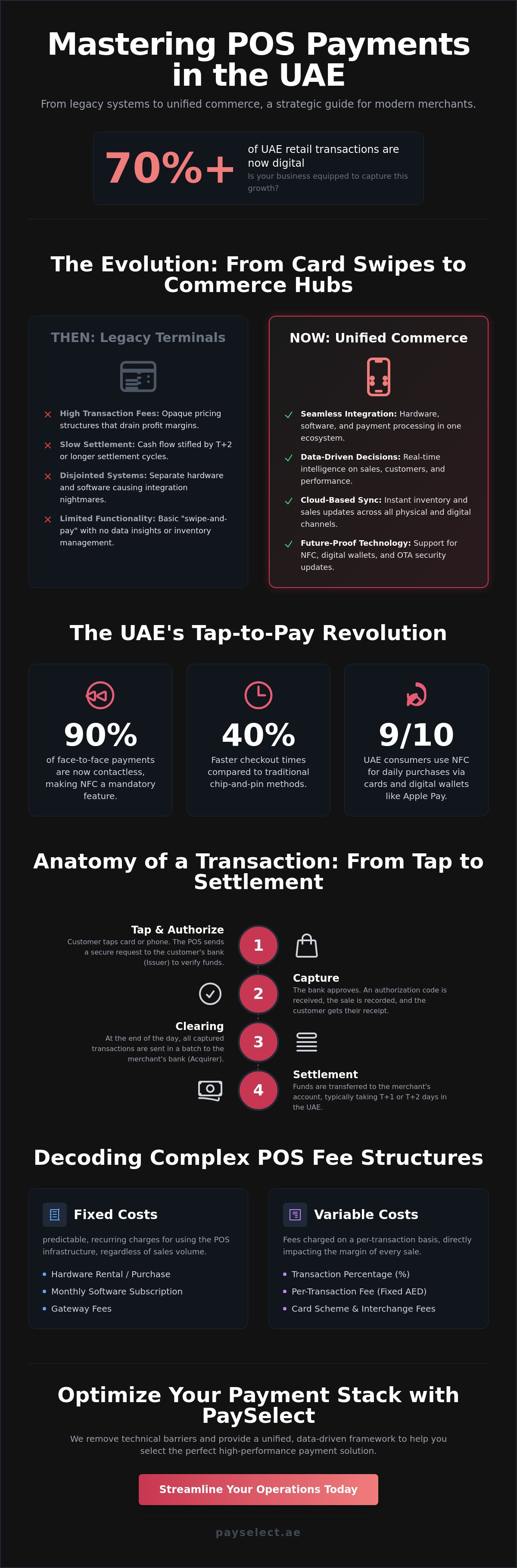

Central Bank data from 2024 reveals that digital transactions now represent over 70% of the UAE retail market, yet many merchants still lose thousands of AED every year to inefficient processing. If your current pos payment setup feels more like a drain on your margins than a tool for expansion, you aren't alone. It's frustrating to manage high transaction fees and opaque pricing while trying to scale a business in a competitive landscape. You deserve a financial infrastructure that works as hard as you do.

This guide empowers you to master the complexities of point of sale payments to maximize your efficiency and accelerate growth. You'll learn how to optimize your transaction infrastructure, reduce operational costs, and deploy reliable hardware that supports every modern payment method. We provide the strategic insights needed to streamline your operations and create a seamless, borderless checkout experience that converts customers into loyal advocates.

Key Takeaways

• Transition from basic card swiping to a unified commerce ecosystem that integrates hardware and software for seamless business scaling.

• Master the transaction lifecycle from authorization to settlement to ensure your pos payment infrastructure operates with maximum speed and reliability.

• Decode complex fee structures in the UAE market to differentiate between fixed and variable costs, protecting your margins on every AED processed.

• Identify the specific infrastructure requirements for your industry to leverage transaction volume and average value for better processing terms.

• Utilize an independent, data-driven framework to remove provider bias and streamline the selection of a high-performance payment stack.

The Evolution of POS Payment Systems in the Modern Economy

A modern pos payment system is no longer just a digital version of a cash register. It represents the strategic intersection of specialized hardware, cloud-based software, and high-speed financial processing. Merchants across the UAE are transitioning from legacy "swipe-and-pay" models toward "Unified Commerce" ecosystems. This shift merges physical and digital sales channels into a single, cohesive infrastructure. To understand the foundation of these tools, it's helpful to look at What is a POS System? and how its components have matured from simple calculators to data-driven hubs.

Seamlessness is the new standard for the customer journey. In 2024, approximately 67% of consumers expect their shopping experience to be consistent whether they're buying through a mobile app or at a physical counter in Dubai Mall. Beyond processing transactions, modern systems act as the brain of a business. They collect massive amounts of data, providing real-time intelligence on customer behavior, peak sales hours, and staff performance. This data allows owners to make decisions based on facts rather than intuition.

Beyond the Terminal: The Software Revolution

The transition from legacy "dumb" terminals to intelligent Android-based devices has changed how retailers operate. These modern pos machines run on flexible operating systems that support third-party apps and custom integrations. Cloud-based software ensures that inventory syncs across all locations instantly. If a product sells out in an Abu Dhabi branch, the system updates the central database in milliseconds. Security is managed through over-the-air (OTA) updates, which deploy the latest encryption standards and features without requiring a technician to visit the site.

The Rise of Contactless and NFC Technology

The UAE market currently leads the region in digital payment adoption. Contactless transactions now account for over 90% of all face-to-face payments in the country. This dominance makes "Tap-to-Pay" capability a mandatory feature for any merchant looking to scale. Supporting digital wallets like Apple Pay and Google Pay requires specific hardware certifications and secure NFC controllers.

NFC Technology

Near Field Communication is a short-range wireless connectivity standard that enables secure data exchange between a terminal and a mobile device within a 4cm range, currently utilized by 9 out of 10 UAE consumers for daily purchases.

Speed of Service

Contactless transactions reduce checkout times by up to 40% compared to traditional chip-and-pin methods.

Security

Tokenization ensures that actual card numbers are never shared during the transmission, protecting both the merchant and the buyer from fraud.

Merchants often face hurdles when setting up these systems, such as complex integration with existing accounting software or slow settlement cycles. PaySelect addresses these pain points by offering streamlined onboarding and unified reporting. By removing the technical barriers to entry, businesses can focus on growth while the infrastructure handles the complexities of modern commerce.

How POS Payment Processing Works: From Tap to Settlement

Every pos payment made in a Dubai boutique or an Abu Dhabi cafe triggers a sophisticated global relay. Within milliseconds, data travels across continents to ensure funds exist and the transaction is legitimate. This lifecycle involves four critical pillars: the merchant, the acquirer, the card scheme, and the issuing bank. The payment gateway acts as the secure digital courier, encrypting sensitive data to prevent interception during transit. This seamless coordination allows businesses to accept payments from customers worldwide without manual intervention.

The Anatomy of a Transaction

Processing happens in two distinct stages. The front-end starts the moment a customer taps their card or phone. The terminal captures the data and sends an authorization request to the issuing bank. If approved, the terminal receives a code, and the sale is complete. The back-end involves the actual transfer of funds. While authorization is instant, settlement usually takes T+1 or T+2 days in the UAE. This delay allows banks to verify transactions and clear batches. Business owners often face frustration with slow settlement cycles, which can stifle cash flow. Modern pos machines streamline this by optimizing the communication between these financial entities.

Authorization

The bank confirms the customer has sufficient AED balance and approves the request.

Capture

The merchant records the transaction in a batch for later processing.

Settlement

The acquirer deposits the funds into the merchant's account after deducting applicable fees.

Understanding the overhead is vital for budget planning. Beyond simple hardware, POS system costs include merchant service fees and software subscriptions that vary between providers. Transparency in these fee structures helps UAE merchants scale without hidden financial surprises. Many business owners struggle with complex fee breakdowns, so choosing a provider that simplifies these costs is a strategic advantage.

Security Protocols and Fraud Prevention

Security isn't optional; it's the foundation of trust. End-to-end encryption (E2EE) scrambles data from the point of entry until it reaches the processor. Tokenization goes further by replacing card numbers with unique digital identifiers. If a system is breached, the tokens are useless to hackers. EMV chips have largely eliminated counterfeit fraud in the UAE by creating a unique transaction code for every tap or dip. These layers of protection ensure that sensitive financial data remains shielded from external threats.

Compliance with PCI-DSS standards ensures that every link in the processing chain meets rigorous security benchmarks. Leading systems now integrate AI to monitor transactions in real-time. These algorithms identify suspicious patterns before they impact your bottom line. By removing these technical barriers, PaySelect empowers entrepreneurs to focus on growth rather than risk management. If you're ready to upgrade your infrastructure, you can explore our advanced terminal options to find the right fit for your business.

Navigating the Complexities of POS Costs and Hidden Fees

Many merchants in the UAE view processing costs as a primary barrier to growth. This perception often stems from a lack of transparency in traditional billing structures. To scale effectively, you must distinguish between fixed monthly costs and variable transaction fees. While fixed costs cover platform access and support, variable fees fluctuate based on your sales volume and the specific pos payment methods your customers choose. This distinction is vital for maintaining healthy margins and predicting cash flow.

The Merchant Discount Rate (MDR) represents the core of your processing costs. It's a percentage-based fee deducted from every transaction. In the UAE market, this rate is influenced by your business sector, monthly turnover, and the risk profile of your industry. Beyond the MDR, hidden fees often surprise unprepared businesses. Common examples include:

PCI Non-Compliance Fees

Penalties charged if your system doesn't meet security standards, often costing AED 75 to AED 150 monthly.

Statement Fees

Charges for providing digital or paper breakdowns of your monthly activity.

Minimum Monthly Volume Fees

Penalties applied if your total transaction volume falls below a pre-agreed threshold.

PaySelect helps merchants eliminate these surprises by providing clear, upfront fee structures. We focus on removing barriers so you can streamline operations, optimize revenue, and empower your business to reach its full potential.

Understanding Interchange and Scheme Fees

Every transaction involves a complex chain of stakeholders. Interchange fees are the largest component, paid directly to the bank that issued the customer's card. Scheme fees are separate costs paid to networks like Visa or Mastercard for the use of their global infrastructure. These rates aren't static; they vary based on card type, such as corporate versus consumer cards, and whether the transaction is local or international.

Most providers offer "Blended" pricing, which simplifies costs into one flat rate for all card types. While easy to understand, it often hides the potential savings of lower-cost local transactions. Conversely, "Interchange Plus" pricing passes the direct costs of interchange and scheme fees to you, plus a specific provider markup. This model offers the highest level of transparency, allowing you to see exactly where every fils is spent. Choosing the right model helps you accelerate growth by aligning costs with your specific customer base.

Total Cost of Ownership (TCO) for Hardware

Selecting hardware involves more than just the sticker price. You must evaluate the Total Cost of Ownership (TCO) to avoid unexpected drains on your budget. Buying terminals outright requires a higher initial investment, typically ranging from AED 1,200 to AED 2,500, but it eliminates monthly rental overhead. Rental models lower the entry barrier for new businesses but can become more expensive over a three-year period.

A comprehensive TCO calculation includes several recurring elements that keep your pos payment system operational. You must account for data SIM card subscriptions for mobile connectivity, thermal paper rolls for receipts, and dedicated technical support. Reliable hardware ensures a seamless checkout experience, which is a significant competitive advantage. When comparing POS machine costs and features, look for solutions that integrate these costs into a manageable, predictable framework. This strategic approach ensures your technology remains an asset rather than a liability as you scale.

Strategic Framework for Selecting Your POS Infrastructure

Selecting a POS payment system isn't just about swiping cards. It's a foundational decision that dictates how your business scales, operates, and retains customers in the UAE market. A misaligned system leads to checkout bottlenecks, reconciliation errors, and frustrated staff. You need a setup that's simple, manageable, and ready for implementation today.

Your transaction profile determines your leverage. Merchants processing over AED 50,000 monthly can often negotiate more competitive processing rates with providers. High average transaction values (ATV) require systems with advanced fraud detection and rapid settlement cycles to keep your cash flow healthy. Don't settle for a one-size-fits-all fee structure when your volume suggests you're a high-tier partner.

Hardware choice defines your customer's experience. High-traffic retail outlets in Dubai Mall require fixed, high-speed countertop units for stability. In contrast, delivery fleets and pop-up boutiques benefit from SoftPOS technology. This turns any NFC-enabled smartphone into a terminal, which helps micro-merchants reduce hardware overhead by up to 45% while maintaining professional standards.

Industry-Specific Feature Sets

Standard terminals don't solve sector-specific pain points. F&B operators require table management, split-billing, and kitchen display synchronization to maintain order. Retailers prioritize high-speed scanning and real-time inventory tracking across multiple UAE branches. Service-based businesses, like salons or consultancies, need integrated appointment scheduling and recurring billing. Look for a pos payment solution that eliminates manual work through native features rather than clunky add-ons.

Integration and Scalability

An integrated POS setup is your most valuable asset. It allows your terminal to talk directly to your cash register or ERP software. This synchronization saves staff roughly 20 minutes per shift in manual reconciliation and prevents costly entry errors. Modern APIs empower you to connect loyalty programs or sync offline sales with your e-commerce store. If you plan to expand your brand internationally, the importance of cross-border payment capabilities cannot be overstated. It ensures your infrastructure remains borderless as you grow.

Technical downtime is expensive. Every minute your system is offline in a busy market like Abu Dhabi or Dubai represents lost revenue. Verify that your provider offers 24/7 on-the-ground support with a guaranteed response time. A reliable partner provides more than just hardware; they offer a rock-solid financial bridge that keeps your business moving forward. Use these five criteria to evaluate your options:

• Industry-specific software compatibility.

• Direct ERP and accounting integration.

• Mobility requirements (Countertop vs. SoftPOS).

• Transaction volume and ATV negotiation power.

• Local, 24/7 technical support availability.

Ready to upgrade your business infrastructure? Explore high-performance POS machines tailored for UAE merchants.

Optimizing Your Payment Stack with PaySelect

PaySelect stands as the independent authority in a market saturated with conflicting offers and complex fee structures. Selecting a pos payment solution shouldn't involve guesswork or brand bias. Our "Take the Test" tool removes the noise from the selection process, providing a data-driven path to the provider that actually fits your volume. By leveraging an advisory service for large-scale infrastructure audits, you gain total transparency into your overhead. This clarity directly reduces long-term operational costs, ensuring every fils spent contributes to your bottom line rather than disappearing into hidden margins.

Many UAE merchants struggle with settlement delays that freeze their cash flow for days at a time. Others face integration hurdles that prevent their physical stores from syncing perfectly with their online sales platforms. PaySelect addresses these specific pain points by auditing your entire stack to find the most efficient path forward. We identify where you're overpaying for legacy systems and show you how to transition to modern, borderless solutions. This strategic approach transforms your payment processing from a simple utility into a powerful competitive advantage.

Why Independence Matters in Fintech

A bank-agnostic approach secures better pricing and superior technology for your business. We act as the bridge between complex financial tech and your specific operational needs. PaySelect doesn't process payments. Instead, we optimize your choice to ensure your pos payment setup is resilient and cost-effective. We focus on three core pillars: transparency, scalability, and technical excellence. This neutral stance allows us to highlight the genuine differences between providers without favoring one over another, helping you avoid the "lock-in" trap of proprietary bank hardware.

The UAE retail sector is moving toward a cashless future, driven by government initiatives and the 2026 digital transformation goals. Staying ahead means adopting a stack that supports every local and international payment method seamlessly. PaySelect helps you navigate these regulatory shifts without the stress of technical debt. We ensure your infrastructure is ready for the next wave of innovation, from biometric authentication to instant local settlements in AED.

Next Steps: Audit and Implement

Start by reviewing your current merchant statements for hidden inefficiencies. Many businesses in the Emirates lose between 0.5% and 1.5% of their total revenue to poorly optimized fee structures and unnecessary middleman costs. You can use the PaySelect comparison tool to benchmark your current rates against the latest market standards. This simple step often reveals significant opportunities for immediate savings.

• Identify high-fee transactions that can be routed more efficiently.

• Evaluate if your current hardware supports the latest contactless standards.

• Compare your settlement windows against the fastest available in the UAE market.

Empower your business with a payment stack designed for growth. It's time to streamline your operations, accelerate your settlements, and scale your reach across the Emirates. By choosing a partner that prioritizes your interests over a specific processor's targets, you build a foundation that is both high-end and deeply reliable.

Secure Your Competitive Edge in the UAE Market

The UAE payment landscape is moving fast. By 2026, the Central Bank of the UAE's Digital Payment Transformation initiative aims to make the Emirates a global leader in cashless commerce. Success requires more than just a terminal; it demands a strategic pos payment stack that minimizes hidden fees and maximizes transaction speed. You've learned how to decode complex fee structures and why independent infrastructure selection is the only way to protect your margins in a competitive market.

PaySelect removes the friction of finding the right partner. We provide an independent advisory service with zero provider bias, focusing exclusively on the unique MENA payment landscape. For enterprise clients, our expert cost-optimization audits identify where AED is being lost to inefficient processing. We don't represent the banks; we represent your business interests. Our goal is to streamline your operations while you focus on expansion.

Find the perfect POS system for your business with our independent comparison tool. Take control of your settlement cycles and hardware costs today. Your future growth depends on the technology you choose right now.

Frequently Asked Questions

What is the average MDR for POS payments in the UAE?

The average Merchant Discount Rate (MDR) for a pos payment in the UAE typically ranges between 1.5% and 2.5% for credit cards, while local debit cards often see rates between 0.5% and 1.0%. These figures fluctuate based on your business sector, transaction volume, and the specific card type used. High-risk sectors or premium international cards usually command the higher end of this spectrum. Merchants should review their monthly statements to identify hidden processing fees that can erode profit margins.

Can I use a POS machine without a local bank account?

You can't operate a POS terminal in the UAE without a local corporate bank account. Central Bank regulations require that all funds from card transactions settle into an account registered within the country to ensure compliance and anti-money laundering oversight. This requirement often creates a hurdle for new entrepreneurs who face delays in corporate bank account opening. PaySelect streamlines this transition by helping businesses navigate the documentation required to connect their payment infrastructure to their local accounts.

What is the difference between a POS system and a payment gateway?

A POS system facilitates physical, in-person transactions at a storefront, whereas a payment gateway handles online digital payments for e-commerce. While both process card data, the POS requires hardware like a terminal or card reader to capture chip or contactless information. Modern businesses often require an integrated approach where both systems sync data to a single dashboard. This synchronization eliminates the pain point of fragmented reporting and ensures a unified view of all sales channels.

How long does it take to settle funds from a POS transaction into my account?

Settlement for a pos payment in the UAE typically takes 1 to 2 business days, often referred to as T+1 or T+2. Some traditional providers may take up to 5 days during public holidays or weekends. Delayed access to capital is a common frustration for growing businesses that need immediate liquidity. We focus on optimizing these settlement cycles to ensure your cash flow remains consistent and your operations continue without financial bottlenecks.

Is it better to rent or buy a POS terminal for a new business?

Renting a POS terminal is generally better for new businesses looking to minimize upfront capital expenditure, with monthly fees starting around 50 AED to 150 AED. Buying the hardware outright reduces long-term monthly costs but requires an initial investment of 1,000 AED to 3,000 AED per unit. Many merchants choose the rental model because it often includes free maintenance and hardware upgrades. This flexibility allows you to scale your physical footprint without committing heavy resources to depreciating assets.

What happens if the internet goes down during a POS payment?

Modern POS terminals switch to an offline processing mode or store-and-forward capability if your internet connection fails. The device securely stores the encrypted transaction data and uploads it for authorization once the connection is restored. This prevents lost sales and reduces customer friction during peak hours. Merchants should be aware that offline transactions carry a slightly higher risk of chargebacks if the card has insufficient funds, so it's always best to use a backup 4G SIM card.

Do POS systems in the UAE support international cards and currency conversion?

Most UAE POS systems fully support international Visa, Mastercard, and Amex cards while offering Dynamic Currency Conversion. This feature allows tourists to pay in their home currency while you receive the settlement in AED. It provides transparency for the customer and can even generate additional revenue for the merchant through shared conversion commissions. Implementing borderless payment options is a strategic move for businesses located in high-traffic tourist hubs like Dubai or Abu Dhabi.

How can I lower my transaction fees for high-volume sales?

You can lower transaction fees by negotiating a volume-based pricing tier once your monthly turnover exceeds 100,000 AED. Many providers offer Interchange Plus pricing models which are more transparent and cost-effective for high-volume merchants than flat-rate plans. Another strategy involves encouraging the use of local debit cards, which carry lower processing costs than international credit cards. We help businesses analyze their transaction data to identify these optimization opportunities and reduce unnecessary overhead.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.