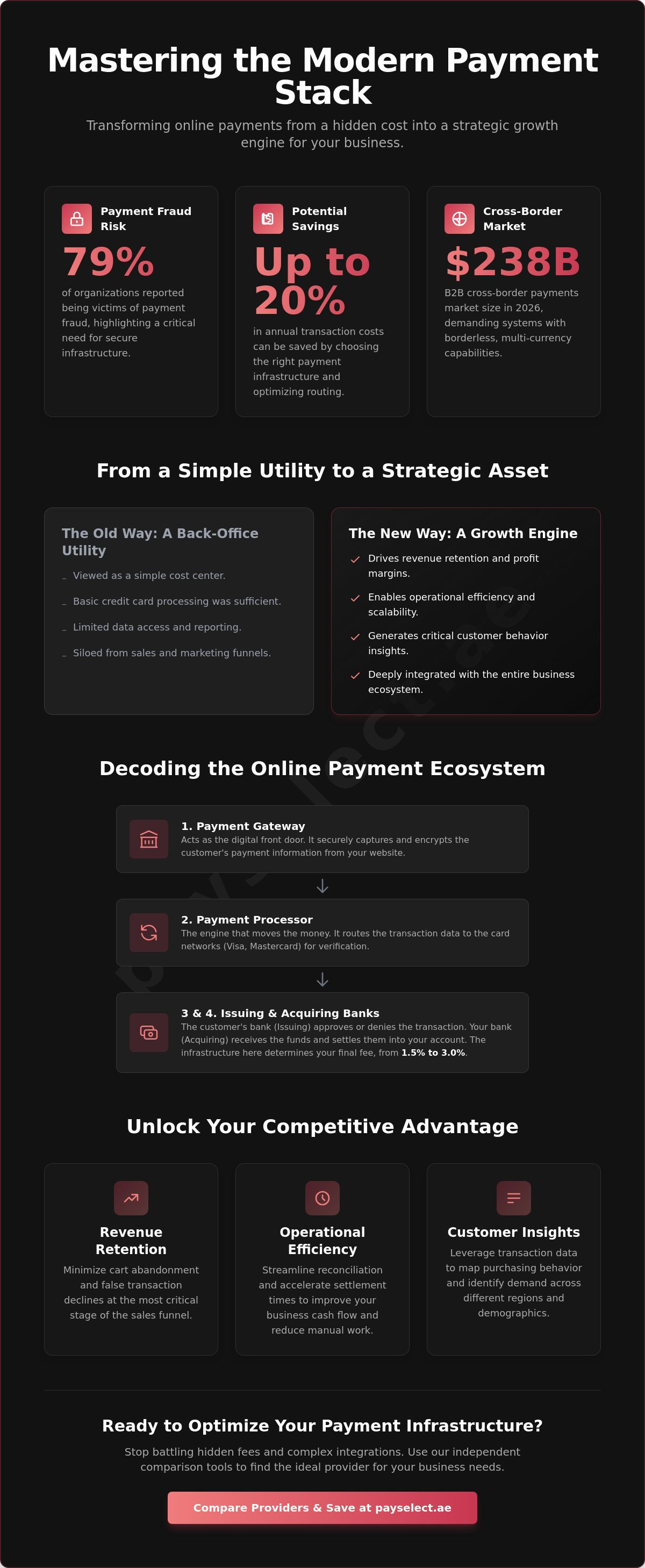

Did you know that 79% of organizations reported being victims of payment fraud by May 2026? This statistic proves that your strategy for online payment is no longer just a utility; it's a strategic asset that can save your business up to 20% in annual transaction costs. You likely find yourself battling hidden fees, struggling with complex technical integrations, and failing to find a clear way to compare different providers. It's a common friction point for entrepreneurs who want to scale without their margins being eroded by the payment stack.

This guide empowers you to master these complexities and build a cost-efficient, scalable payment infrastructure. You'll learn how to navigate the April 2026 interchange rates, implement PCI DSS 4.0.1 standards, and adapt to the latest Nacha ACH rule changes. We show you how to streamline operations, accelerate settlements, and scale your global reach. We'll break down the modern payment stack, analyze the impact of the 2026 PACE Act, and provide the clarity you need to optimize every transaction for a borderless economy.

Key Takeaways

• Understand the fundamental pillars of the online payment ecosystem to transform your transaction processing from a simple utility into a strategic growth engine.

• Identify and bypass the common "hidden fee" traps and technical integration hurdles that often inflate costs and delay market entry.

• Learn to evaluate infrastructure based on high-performance metrics like uptime reliability and user experience optimization to reduce checkout friction.

• Discover how independent, unbiased comparison tools empower you to select the ideal provider for your specific business needs without technical complexity.

The Evolution of Online Payment for Modern Commerce

Modern commerce doesn't treat online payment as a back-office utility. It's a strategic framework that integrates deeply with your sales funnel, customer experience, and accounting systems. Ten years ago, a digital credit card swipe was the ceiling. Today, sophisticated e-commerce payment systems handle multi-party settlements, automated compliance, and real-time fraud detection. This shift from simple transactions to comprehensive financial infrastructure allows businesses to operate with global ambition from day one.

The B2B cross-border payments market reached $238 billion in 2026, driven by a global appetite for frictionless trade. Businesses must now prioritize borderless, multi-currency capabilities to remain competitive. A seamless payment flow does more than just capture a sale. It builds trust, reduces cart abandonment, and increases lifetime customer value. When the checkout process is fast and intuitive, customers return. When it's clunky, lacks their preferred currency, or fails to support local payment methods, they vanish. In a world where 66% of US businesses now demand instant payments, speed is no longer a luxury. It's the baseline for entry.

From Utility to Strategic Business Asset

Your payment stack directly dictates your profit margins. Choosing the right infrastructure can save a business up to 20% in annual transaction costs by optimizing routing and reducing unnecessary fees. Beyond the money, every transaction generates a data point. High-end businesses treat their payment flow as a competitive advantage by focusing on three key areas:

Revenue Retention

Minimizing false declines and cart abandonment at the final hurdle.

Operational Efficiency

Streamlining reconciliation and reducing settlement times for better cash flow.

Customer Insights

Using transaction data to map purchasing behavior and demand across different regions.

Settling for a "good enough" setup means leaving revenue on the table and ignoring the vital data that drives intelligent growth. If your current provider lacks robust reporting or charges for data access, you're operating with a blind spot that competitors will exploit.

The Digital Economy Demands Scalability

Scaling requires more than just adding new products. It requires an online payment infrastructure that adapts to regional preferences instantly. The Asia-Pacific region is currently seeing a 9% compound annual growth rate in B2B cross-border payments through 2030. If your system can't handle diverse digital wallets or local settlement methods, you're locked out of the fastest-growing markets. Flexible systems allow you to pivot, enter new territories, and scale your global reach without rebuilding your technical foundation. PaySelect helps you navigate these choices by providing transparent comparisons, ensuring you don't get trapped by providers with limited geographic scope or rigid API structures. We empower you to streamline, accelerate, and scale your operations with absolute confidence.

Decoding the Online Payment Ecosystem

The machinery behind a single click is vast. Every online payment follows a high-speed relay involving four primary actors. First, the Gateway captures the data. Second, the Processor routes it. Third, the Issuing Bank (your customer's bank) approves the funds. Finally, the Acquiring Bank (your bank) receives the settlement. While this happens in under two seconds, the infrastructure behind it determines whether you pay a 1.5% fee or a 3.0% fee. Understanding these components is the first step toward reclaiming your margins.

Many businesses face a choice between a unified stack and a modular setup. A unified stack bundles the gateway and processor into one package. It's fast to set up, but it often hides costs and limits your ability to negotiate. A modular approach lets you pick the best-in-class provider for each role. This flexibility is vital for businesses scaling across borders, as it allows you to route transactions through local acquirers to avoid high cross-border fees. Identifying the right balance for your specific volume is where strategic planning pays off.

Gateways vs. Processors: Knowing the Difference

The gateway acts as your digital front door. It's responsible for the "handshake" between your website and the financial world, ensuring data is encrypted and secure. In contrast, the processor is the engine moving the money. It communicates with card networks to verify funds and manage the actual transfer. Many modern providers now bundle these services together to simplify the user experience. However, separating them can sometimes lead to lower transaction costs for high-volume merchants. You can explore how different payment gateways integrate with your existing tech stack to find the most efficient path.

The Role of Compliance and Security

Security is the foundation of digital trust. As of March 31, 2025, PCI DSS version 4.0.1 became the mandatory standard for any business handling cardholder data. Implementing secure online payment processing is no longer just about having an SSL certificate. It requires advanced tokenization, where sensitive card numbers are replaced with unique identifiers. This ensures that even if a breach occurs, the data is useless to hackers. Additionally, 3D Secure 2.0 has become the industry standard, balancing fraud protection with a frictionless checkout. It uses rich data to authenticate customers in the background, preventing the "abandoned cart" syndrome caused by clunky verification steps.

Choosing the right ecosystem partners doesn't have to be a guessing game. If you're looking to optimize your current setup, you can compare payment solutions to see which providers offer the best balance of security and cost-efficiency for your region.

Navigating Common Barriers in Payment Setup

Setting up an online payment structure often feels like walking through a minefield of opaque pricing and technical debt. Many providers lead with a low headline rate, only to bury additional costs in the fine print. Understanding the online payment lifecycle helps you see where these costs creep in, from initial authorization to final settlement. It's not just about the transaction fee; it's about how long your capital is locked away. With 66% of businesses surveyed in April 2026 indicating they'd use instant payments if offered, slow settlement times have become a major barrier to competitive growth.

Beyond the money, technical friction can stall your market entry. If your payment stack doesn't talk to your CRM and accounting software, you'll waste hours on manual reconciliation. This lack of integration creates a fragmented view of your business, making it impossible to scale with confidence. PaySelect helps you identify these hurdles early, providing a clear comparison of providers that prioritize seamless data flow and rapid settlements.

Understanding the Real Cost of Acceptance

You can't manage what you can't see. The Merchant Discount Rate (MDR) is only the surface. As of April 2026, Visa Credit CPS Retail interchange rates sit at 1.51% + $0.10, while MasterCard Credit Consumer is 1.65% + $0.10. If your provider's flat rate is significantly higher, you're paying for their convenience, not your growth. You must also account for setup fees, monthly minimums, and chargeback penalties that often exceed $20 per incident. International sales add another layer of complexity. Currency conversion markups often range from 1% to 3% above mid-market rates, quietly eroding your margins on borderless transactions.

Solving the Integration Puzzle

Technical stability is the backbone of your checkout experience. You face a choice between hosted checkout pages, which offer rapid deployment, and custom API integrations, which provide total brand control. Utilizing professional payment gateway integration services ensures your stack remains stable during high-traffic events and prevents technical debt. A well-integrated system automates the flow of information, allowing you to focus on strategy rather than troubleshooting broken connections.

Compliance is the final hurdle. New Nacha rules effective March 20, 2026, require standardized descriptions for ACH payments, such as "PAYROLL" or "PURCHASE." Additionally, the proposed PACE Act of 2026 may soon place large state-regulated payment companies under federal supervision. Keeping up with these shifts is exhausting. We empower you to navigate these regulations by identifying partners that automate compliance, helping you maintain a secure and borderless online payment environment.

Key Criteria for Selecting Your Payment Infrastructure

Selecting an online payment partner is a decision that dictates your business's trajectory for years. Reliability isn't just a technical metric; it's the heartbeat of your revenue. Uptime is revenue. A provider with 99.9% uptime still allows for nearly nine hours of downtime annually. For a high-volume merchant, those lost hours translate into thousands of dollars in unrecovered sales. You need a partner that offers redundant routing to ensure that if one processing path fails, your transactions still clear without a hitch.

Beyond uptime, your online payment infrastructure must scale. A system that works for 100 transactions a day might buckle at 10,000. Look for providers that offer tiered pricing and robust APIs that don't require a total rebuild as you expand. Localized customer support is equally critical. When a settlement fails or a regional bank blocks a transaction, you can't afford to wait 48 hours for a ticket response. You need immediate, expert intervention to keep your cash flow moving.

Balancing Security with Conversion

Strict fraud filters protect your business, but they can also be your worst enemy. Overly aggressive settings create "false positives," where legitimate customers are blocked. Friction kills sales. Modern systems use AI-driven transaction monitoring to distinguish between a fraudster and a high-value customer. Implementing one-click checkouts and saved card features reduces the "buy button" friction. By 2026, biometric authentication has become the gold standard for mobile commerce, providing high security without the need for complex passwords.

Evaluating Cross-Border Capabilities

Expanding your reach requires cross-border payment solutions that go beyond simple currency conversion. Real-time payment networks now operate in almost 80 countries, and your infrastructure must tap into these local rails. Accepting a customer's preferred local method can increase conversion by up to 30% in specific markets. You also need to manage multi-currency settlements strategically. If your provider converts every sale back to your base currency immediately, you're likely losing 1% to 3% on exchange rate markups. Look for systems that allow you to hold multiple currencies and settle when the rates are favorable.

Ready to find a partner that checks all these boxes? You can compare payment solutions to find the perfect fit for your growth strategy.

Streamlining Your Selection Process with PaySelect

Choosing an online payment provider shouldn't feel like a high-stakes gamble. In a market flooded with competing claims, finding the truth about fee structures and technical reliability is exhausting. Most ranking pages are built by providers trying to sell their own software, offering zero transparency on how they compare to the rest of the industry. PaySelect changes this dynamic. We act as an independent, results-oriented bridge between complex financial infrastructures and your business needs.

Our approach removes bias from the equation. We don't favor one provider over another; instead, we provide the insights you need to differentiate between them fairly. Whether you're dealing with the hidden transaction fees mentioned earlier or struggling with complex API integrations, we offer a structured path to clarity. Our matching process begins with a simple "Take the Test" assessment, leading to tailored advisory that aligns with your specific volume and growth goals.

Why Independence is Your Greatest Advantage

There's a fundamental difference between being sold a product and being guided to a solution. We analyze your industry-specific requirements, such as high-risk compliance or the need for multi-currency settlements, to find your perfect match. You save valuable time by bypassing the marketing fluff of individual providers. We focus on the ultimate business outcome: a payment stack that is simple, manageable, and ready for implementation. We empower you to streamline your operations, accelerate your settlements, and scale your global reach without the typical friction.

Next Steps: Moving from Complexity to Clarity

Transitioning to a superior infrastructure begins with data. You can use our comparison tool to find your ideal match based on your current volume and regional requirements. Preparing for a payment audit is the next logical move to uncover immediate cost savings and identify operational gaps in your current flow. A professionally optimized payment stack provides long-term benefits, ensuring your business remains agile and competitive in the fast-moving digital economy of the UAE. We lead you toward a clear decision point without hesitation, turning your technical processing into a strategic tool for transformation.

Secure Your Global Growth Strategy

The transition into 2026 has redefined the online payment landscape as a high-stakes arena for strategic efficiency. You now have the tools to decode complex ecosystems, bypass hidden fee traps, and implement infrastructure that balances robust security with high-conversion checkout flows. By prioritizing borderless capabilities and real-time settlement speeds, you position your business to capture a share of the $336 billion B2B cross-border market projected by 2031. Success in this digital economy requires moving beyond simple utility setups toward a professionally optimized payment stack.

PaySelect provides the independent and unbiased guidance needed to navigate these choices without the marketing noise. We offer expert payment infrastructure consulting tailored specifically for the unique demands of both SMEs and Enterprises. Whether you're streamlining local operations or scaling a global reach, our mission is to remove every barrier between your ambition and your revenue. Streamline your business payments with our independent comparison tool today. Your path to a frictionless, borderless future starts with a single, informed decision.

Frequently Asked Questions

What is the difference between an online payment gateway and a processor?

The gateway acts as the digital interface that encrypts transaction data during the initial handshake, while the processor is the back-end engine that routes funds between banks. Think of the gateway as the front-end security guard and the processor as the logistical network moving the money. Many modern platforms now bundle these two functions to create a more seamless integration for business owners.

How much does it typically cost to accept online payments in the UAE?

Accepting an online payment in the UAE typically involves a percentage-based fee plus a fixed per-transaction cost. Domestic card rates in 2026 often start around 2.0% to 2.2%, while international cards can reach 2.9% or higher depending on the provider. You'll also need to account for potential monthly maintenance fees and setup costs that vary based on your expected transaction volume.

Is it better to use a global payment provider or a local one?

Choosing between global and local providers depends on your primary customer base and scaling ambitions. Global providers offer a unified API that simplifies international expansion, but local providers often provide better domestic settlement rates and regional expertise. Many businesses now use a hybrid approach to optimize costs, often relying on an AWS partner Saudi Arabia SAMA compliant to ensure their cloud infrastructure meets strict regional financial regulations and high acceptance rates across different geographic territories.

What security certifications should I look for in a payment gateway?

PCI DSS Level 1 is the highest and most critical certification you should verify before selecting a partner. You also need to ensure the provider supports 3D Secure 2.0 and offers advanced tokenization to protect sensitive data. These standards ensure your business remains compliant with global regulations while maintaining a frictionless checkout flow for your customers.

How long does it take for online payments to reach my bank account?

Settlement times generally range from two to three business days, commonly referred to as T+2 or T+3. However, the 2026 market is seeing a surge in instant settlement options that move funds in real-time for an additional fee. Your specific industry, risk profile, and transaction volume often dictate the speed at which your bank account is credited.

Can I use the same system for online payments and in-person POS?

Yes, omnichannel platforms allow you to manage both digital and physical transactions through a single, unified dashboard. This approach simplifies your reconciliation process and gives you a holistic view of your customer's purchasing behavior across all channels. Integrating your online payment stack with physical POS hardware streamlines your financial operations and reduces technical overhead.

What are the most common reasons for online payment failures?

Insufficient funds and incorrect card details account for a high percentage of transaction failures. Technical timeouts or overly aggressive fraud filters also play a role in blocking legitimate sales, which can hurt your conversion rates. Monitoring your decline codes helps you identify whether a failure is technical or related to the customer's specific banking institution.

How can I reduce the risk of chargebacks for my business?

Clear billing descriptors and immediate digital receipts are the most effective ways to prevent customer confusion that leads to disputes. Implementing 3D Secure authentication provides an extra layer of protection by shifting the liability for certain fraud-related chargebacks back to the issuing bank. Consistent communication regarding shipping updates and delivery proof also helps reduce "item not received" claims.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.