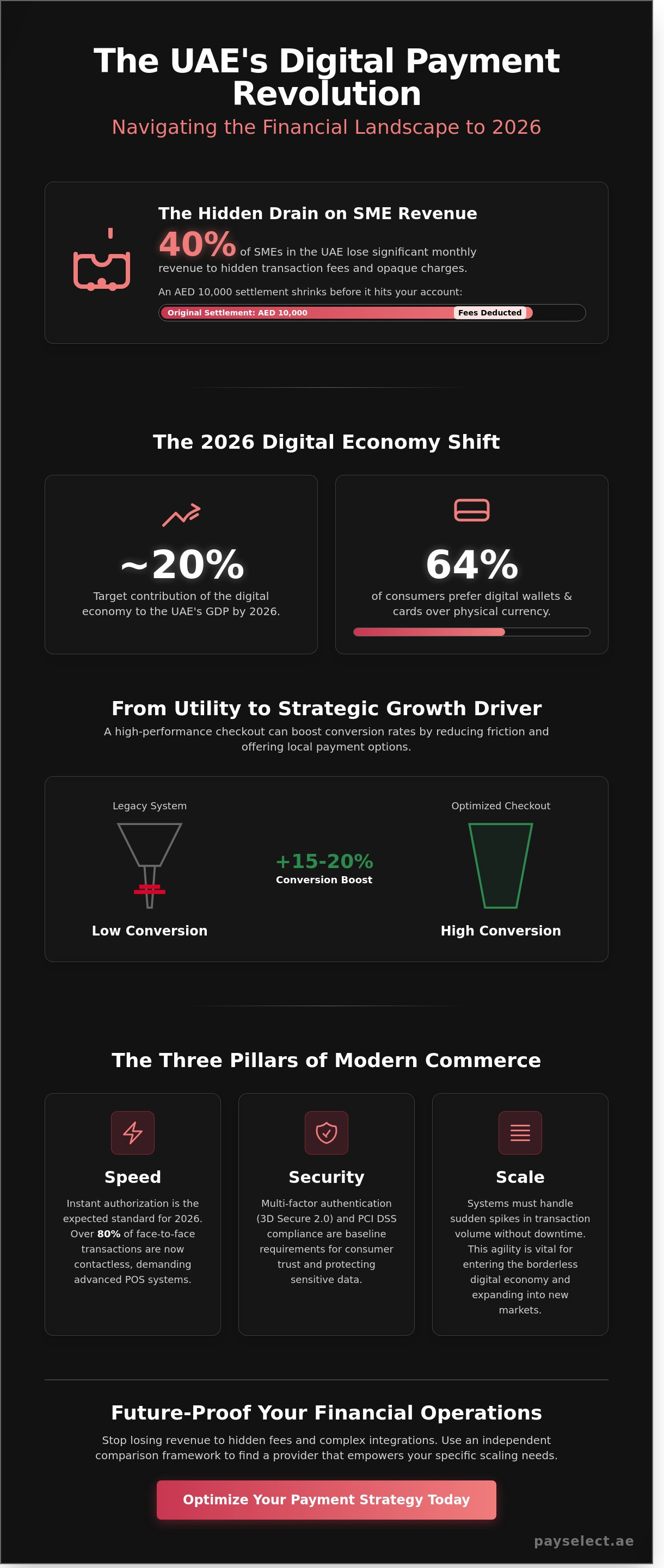

Did you know that 40% of SMEs in the UAE lose a significant portion of their monthly revenue to hidden transaction fees and opaque processing charges? You've likely felt the frustration of seeing your hard earned AED 10,000 settlement shrink before it even hits your bank account. Managing a modern payment stack often feels like a constant trade-off between speed and transparency. We know you want to scale your business without the friction of complex financial hurdles or long integration delays that keep your products off the market.

This guide will help you master the complexities of the UAE financial ecosystem so you can build a scalable, cost-effective infrastructure. You'll discover how to slash transaction fees and eliminate the hurdles of cross-border commerce that drain your resources. We'll break down the 2026 landscape, compare provider fee structures, and show you how to future-proof your financial operations. It's time to empower your business with a seamless, borderless strategy that turns your checkout process into a competitive advantage.

Key Takeaways

• Navigate the UAE’s rapid transition to a digital-first economy and understand how upcoming regulatory shifts will redefine your transaction environment by 2026.

• Master the core components of a modern payment stack to create a seamless, unified commerce experience across both digital gateways and physical POS systems.

• Protect your profit margins by identifying hidden fees and decoding complex Merchant Discount Rates (MDR) to ensure every AED is accurately accounted for.

• Streamline your infrastructure setup by overcoming common hurdles in merchant account approvals and resolving technical integration challenges across diverse platforms.

• Accelerate your business growth using an independent comparison framework to find a provider that empowers your specific scaling needs without bias.

The Evolving Landscape of Digital Payment Systems in the UAE

The UAE digital economy is accelerating at an unprecedented pace. By 2026, the nation aims to double the digital economy's contribution to the GDP to approximately 20%. This shift is powered by a robust infrastructure and the UAE's E-Government initiatives, which have laid the groundwork for a cashless society. Business owners face a landscape where 64% of consumers now prefer digital wallets and cards over physical currency. Accepting a simple credit card isn't enough. You need a strategy that handles high-volume traffic and complex settlement cycles.

Regulatory changes are the primary drivers of this evolution. The Central Bank of the UAE's Retail Payment Services and Card Schemes Regulation has modernized the legal framework, ensuring every transaction meets global security standards. This creates a safer environment but also increases the technical requirements for merchants. Many businesses struggle with high decline rates or slow settlement cycles when using generic, legacy systems. These pain points often emerge because a "one-size-fits-all" approach fails to account for the specific risk profiles and volume needs of a scaling enterprise. A tailored payment setup is now a requirement for survival.

From Utility to Strategic Growth Driver

Payments aren't just back-office tasks anymore. They're growth engines. A high-performance checkout can boost conversion rates by 15% to 20% by reducing friction and offering local currency options. Efficient processing also stabilizes cash flow. When your business scales, you need funds settled quickly to reinvest in inventory or marketing. This agility is vital for those entering the borderless digital economy. Expanding into new markets requires cross-border payments that avoid hidden fees and long delays. PaySelect helps by streamlining these complex integrations, allowing you to focus on expansion rather than technical hurdles.

National Trends Influencing Business Decisions

Modern commerce in Dubai and Abu Dhabi is defined by speed. Contactless preferences account for over 80% of face-to-face transactions, making advanced POS machines essential for physical retail. Security has moved from a feature to a foundational requirement. Merchants now prioritize systems that offer real-time fraud detection and robust data encryption. Beyond security, data analytics is changing how businesses operate. Transaction history provides insights into peak shopping hours and customer spending habits. This intelligence allows you to optimize staffing and stock levels with precision.

Speed

Instant authorization is the expected standard for 2026.

Security

Multi-factor authentication is now a baseline for consumer trust.

Scale

Systems must handle sudden spikes in transaction volume without downtime.

The difference between payment providers often comes down to their ability to integrate with existing software and the speed at which they settle funds. Some providers offer lower entry fees but charge more for international cards or have longer holding periods. Others provide comprehensive data dashboards that turn every transaction into a piece of market research. Choosing the right partner means looking beyond the transaction fee to see the total value of the integration.

Understanding the Core Components of a Modern Payment Stack

Modern commerce in the UAE requires more than a simple cash drawer. It demands a synchronized stack of technologies that communicate in real-time. This infrastructure empowers businesses to accept payments across every channel, from a luxury boutique in Downtown Dubai to a global e-commerce platform. A robust payment stack doesn't just move money. It builds trust, protects data, and accelerates growth.

The Digital Gateway: More Than Just a Checkout

The gateway serves as the digital bridge between your storefront and the banking network. High-performing payment gateways prioritize speed and uptime to ensure every transaction is frictionless. Security protocols are non-negotiable in this environment. Every merchant must implement PCI DSS compliance and 3D Secure 2.0 to safeguard customer details and prevent fraud. API flexibility is another critical factor. It allows your developers to integrate the checkout experience directly into your custom app or website. This customization streamlines the user journey and reduces the likelihood of dropped carts. It's about making the transaction feel like a natural part of the brand experience.

Omnichannel POS Solutions for the National Market

The boundary between physical and digital sales continues to blur. Modern POS machines must do more than print receipts. They act as central hubs for unified commerce. These systems link your physical storefront directly to your online inventory management. When a customer makes a purchase in-store, your digital stock levels update instantly. Recent UAE payments market analysis shows that contactless adoption has surged, with over 80% of consumers now preferring to tap-to-pay. Your hardware must support NFC technology, mobile wallets, and QR code payments to meet this demand. Integrated software also captures vital data. You can monitor peak sales periods and track customer loyalty without manual entry.

Managing international transactions often involves navigating high fees and complex conversion rates. Modern solutions allow you to accept global currencies while settling your funds in AED. This transparency removes barriers for international shoppers and simplifies your accounting. When these components integrate perfectly, they create a borderless experience for the user. A customer can browse on their phone, pay via a secure link, or visit your warehouse and use a card. The technology stays invisible. This allows you to optimize your payment strategy and focus on reaching new markets with total confidence.

Deciphering Merchant Costs: Fees, MDRs, and Hidden Charges

Managing a successful business in the UAE requires a sharp eye on the bottom line. The Merchant Discount Rate (MDR) isn't a single, flat fee. It's a complex bundle of costs that covers the processing of every transaction. This rate typically includes interchange fees paid to the card-issuing bank and scheme fees paid to networks like Visa or Mastercard. While a provider might quote a low headline rate, the total cost of ownership often tells a different story. Many businesses find that the "lowest rate" masks secondary layers of expense that erode profit margins over time.

Hidden charges frequently surprise entrepreneurs during their first settlement cycle. Setup fees in the Dubai and Abu Dhabi markets can range from AED 500 to AED 2,500 depending on the complexity of the integration. Monthly maintenance fees often add another AED 100 to AED 300 to your overhead. Withdrawal charges are another common pain point; some providers charge a flat fee or a small percentage just to move settled funds into your local AED business account. These small leaks can drain thousands of Dirhams from your annual revenue if left unchecked.

The cost of international sales presents a significant hurdle for growing brands. Currency conversion markups are often invisible but highly impactful. If you sell to a customer in the UK but settle in AED, you might lose 3% to 5% of the transaction value through unfavorable exchange rates. This makes a simple payment comparison difficult without looking at the full lifecycle of the money.

The True Cost of a Transaction

Interchange fees are set by card networks and vary based on the card type. Premium rewards cards usually cost more to process than standard debit cards. Scheme fees are the fixed cut taken by the network itself. Merchants processing over AED 1,000,000 annually gain the leverage needed to move toward more transparent pricing models. It's vital to check your contract for "minimum monthly volume" penalties. These fees trigger if your sales dip below a certain threshold, penalizing your business during slow months.

Strategies for Cost Optimization

Optimization starts with data. You should negotiate your rates once your transaction history shows consistent growth over a six-month period. Implementing multi-currency settlement for cross-border payments allows you to avoid unnecessary conversion fees by holding funds in the original currency. Routine audits of your statements can reveal systemic overspending on surcharges that many business owners overlook. This proactive approach ensures your financial infrastructure scales as efficiently as your sales.

Overcoming Common Hurdles in Payment Infrastructure Setup

Establishing a robust payment framework in the Emirates requires a clear strategy to bypass bureaucratic and technical bottlenecks. Merchants often struggle with the rigid requirements of legacy financial institutions. These entities frequently demand exhaustive documentation and high minimum balances that can stifle a startup's cash flow. PaySelect removes these barriers by offering a streamlined path to integration, ensuring that your business stays agile and competitive.

Technical integration presents another significant hurdle. Bridging the gap between your website's checkout and a secure processor requires precision. Many businesses face "code bloat" or slow load times when using poorly optimized APIs. This technical friction leads to a 20% increase in cart abandonment rates across the Gulf region. PaySelect provides optimized integration tools that prioritize speed and security, allowing you to focus on scaling your operations rather than troubleshooting code.

Streamlining the Onboarding Process

Efficiency starts with preparation. To secure a merchant account, you need your valid UAE Trade License, Memorandum of Association, and Emirates IDs for all shareholders. According to 2024 industry benchmarks, 45% of delays in the UAE are caused by inconsistent address proof or outdated licenses. PaySelect automates the vetting process to identify these gaps early. This proactive approach reduces the average go-live time from several weeks to just a few business days. Setting realistic timelines is vital; while some providers promise instant setup, the reality of Central Bank compliance usually necessitates a 48 to 72-hour window for full approval.

Maintaining a Secure and Reliable System

Security is a non-negotiable requirement for survival. With the UAE eCommerce market projected to hit 33.8 billion AED by 2026, the target for digital fraud grows larger every year. Implementing 3D Secure 2.0 is your first line of defense. It provides a frictionless experience for the customer while shifting the liability of chargebacks away from the merchant. Systems must maintain 99.9% uptime to prevent revenue leakage. A brief 15-minute outage during a peak shopping period like White Friday can result in tens of thousands of AED in abandoned carts. PaySelect ensures your payment infrastructure remains resilient against both technical failures and sophisticated fraud attempts.

Ready to eliminate the friction in your financial operations? Optimize your payment gateway with a partner built for the UAE market.

Optimising Your Strategy with the PaySelect Comparison Framework

Success in the UAE's digital economy requires more than just a functional checkout. It demands a strategic alignment between your operational needs and the specific capabilities of your payment provider. Many businesses in Dubai and the Northern Emirates operate with fragmented systems that lead to reconciliation errors and high overhead costs. We solve this by offering a structured framework that prioritizes data over sales pitches.

Our 'Take the Test' tool acts as a digital consultant. It evaluates your business model, transaction volume, and expansion goals to recommend a tailored solution. This removes the guesswork from selecting payment gateways that actually serve your bottom line. By transitioning from a disjointed setup to an integrated stack, you reduce technical debt and improve your cash flow visibility immediately.

Why Independence Matters in Fintech

Traditional providers focus on selling their own proprietary products. An independent consultant focuses on your results. This distinction is vital because transparency directly influences your profit margins. When you base your decisions on objective data, you avoid hidden fees and restrictive contracts that often plague standard agreements. We build partnerships on trust and technical accuracy; not aggressive sales targets. This approach empowers you to select a payment infrastructure that scales as fast as your ambition.

• Eliminate data silos through unified reporting across all sales channels.

• Reduce manual reconciliation time by up to 40% using automated settlement tools.

• Access unbiased comparisons that highlight the unique strengths of different market players.

Next Steps for Your Business Growth

The first step toward optimization is benchmarking. Compare your current processing costs and success rates against the national average of 98% for top-tier providers in the region. If your current infrastructure falls short, it's time to prepare for a seamless migration. We guide enterprise-scale businesses through this transition to ensure zero downtime during the switch. This ensures your revenue stream remains uninterrupted while you upgrade to superior technology.

Scaling your reach requires modern tools like cross-border payments and dynamic payment links. These features allow you to accept AED and other global currencies from international customers without the friction of traditional banking delays. By refining your strategy now, you position your business to lead the market through 2026 and beyond. Efficiency isn't just a goal; it's the foundation of your future expansion.

Future-Proof Your UAE Commerce Strategy

The landscape for digital trade in the Emirates is accelerating. By 2026, businesses that don't optimize their payment infrastructure will face higher costs and slower growth as consumer demand for instant transactions peaks. Success requires mastering merchant discount rates, minimizing hidden fees, and ensuring your stack integrates seamlessly with local regulations. Navigating these technical hurdles alone often leads to wasted capital and integration delays that stall your momentum.

PaySelect acts as your strategic partner by providing an independent and unbiased comparison tool designed for the local market. We offer expert advisory for enterprise-scale optimization and maintain a comprehensive database of national providers to ensure you never overpay for processing. Our framework helps you streamline operations, accelerate settlements in AED, and empower your brand to scale across the region with absolute confidence. It's time to turn your financial infrastructure into a competitive advantage.

Take the test and find your perfect payment partner today

Your path to a borderless, efficient, and highly profitable future starts with the right choice today.

Frequently Asked Questions

What is the average transaction fee for businesses in the UAE?

Transaction fees for businesses in the UAE typically range from 1.5% to 3.0% for local credit and debit cards. Most providers also charge a fixed fee between AED 0.50 and AED 1.50 per transaction. PaySelect helps you navigate these costs by identifying the most efficient payment structures for your specific volume, ensuring your margins remain protected as you scale your operations.

How long does it take to set up a payment gateway for a new business?

Setup times depend on the provider type, with aggregators offering approval in 24 to 72 hours. Direct merchant accounts involve more rigorous vetting and usually take 10 to 20 business days to finalize. We streamline this process by managing the complex documentation and technical requirements, allowing you to focus on your core operations while we accelerate your path to market.

Can I use the same provider for both my online store and physical POS?

You can use a single provider for both digital storefronts and physical retail locations through unified commerce platforms. This approach centralizes your data, making it easier to track sales and manage inventory across all channels. PaySelect eliminates the friction of managing multiple systems, providing a seamless experience that empowers your business to reach customers wherever they choose to shop.

What is the difference between an aggregator and a direct merchant account?

An aggregator groups multiple businesses under a single merchant ID for fast setup, while a direct merchant account provides a unique ID specifically for your company. Aggregators are ideal for startups processing less than AED 100,000 monthly, but direct accounts offer lower long-term rates and better control. We help you transition between these models as your payment volume grows and your needs become more complex.

How do cross-border payment solutions help reduce currency exchange costs?

Cross-border solutions reduce costs by utilizing local settlement networks and competitive mid-market exchange rates. Traditional banks often charge a 3% to 5% markup on currency conversion, but modern fintech tools can lower this to under 1%. PaySelect provides the borderless infrastructure needed to capture global sales without the burden of excessive hidden fees, directly boosting your bottom line in the global economy.

Is it possible to integrate a payment gateway without extensive coding knowledge?

It's entirely possible to integrate a gateway using no-code plugins or hosted checkout pages that require zero technical expertise. Most major e-commerce platforms offer pre-built connectors that you can activate in minutes. PaySelect prioritizes user experience by offering intuitive tools that simplify the integration process, ensuring you can start accepting transactions without the need for a dedicated development team.

What should I do if my merchant account application is rejected?

If your application is rejected, you should first request a specific reason, which is often related to high-risk business categories or incomplete KYC documentation. Update your business plan, ensure your website meets all compliance standards, and consider providers that specialize in your specific industry. PaySelect acts as a strategic partner, helping you resolve these common pain points and positioning your business for successful approval.

How often should I audit my payment processing costs for optimization?

You should audit your processing costs every 6 months or whenever your monthly transaction volume increases by 20%. Regular reviews help identify hidden fees and provide the leverage needed to negotiate better rates as your business matures. PaySelect focuses on continuous optimization, giving you the insights needed to refine your financial strategy and maintain a competitive edge in the fast-paced UAE market.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.