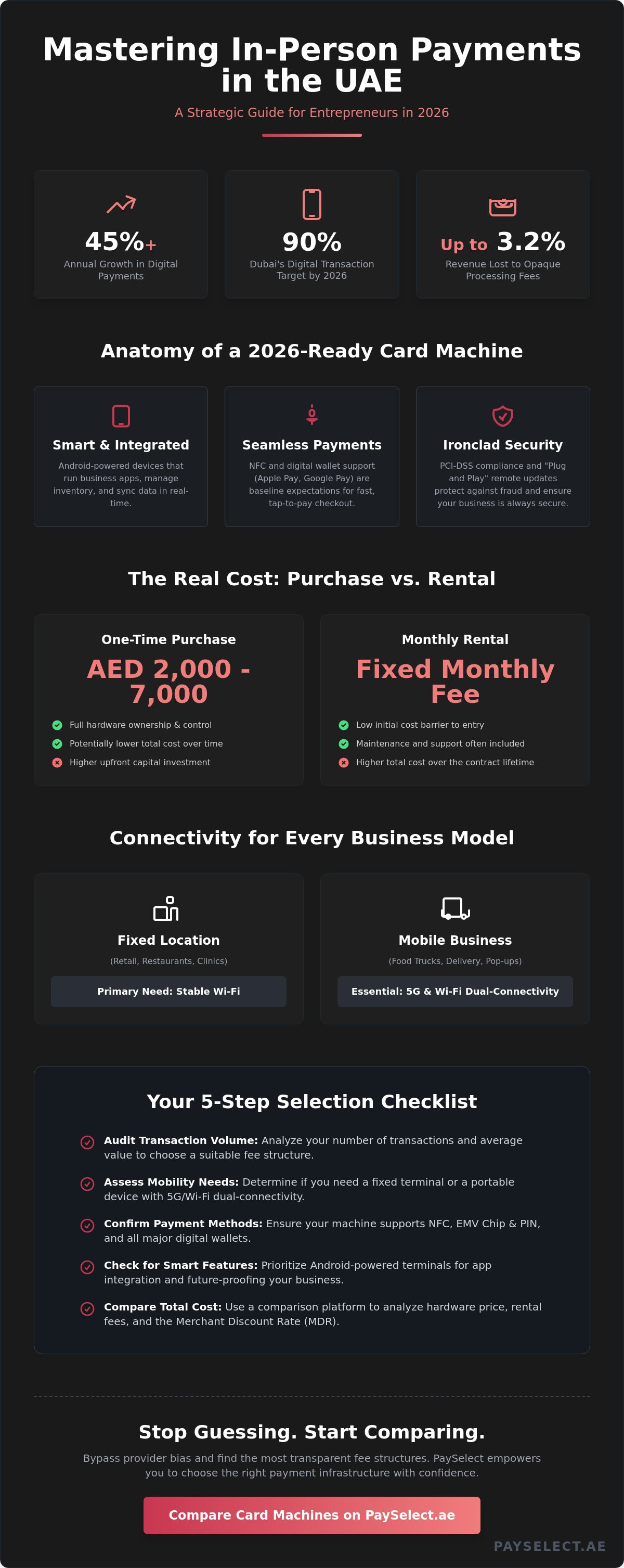

Digital payments in the UAE have grown by over 45% annually since 2024, yet many entrepreneurs still lose up to 3.2% of their gross volume to opaque processing fees. You know that modernizing your checkout is essential as Dubai moves toward a 90% digital transaction target by the end of 2026. However, selecting a card machine shouldn't mean settling for outdated hardware or long settlement periods that stall your cash flow. It's frustrating to face complex fee structures that eat into your margins while your business waits days for its own hard-earned revenue.

This guide empowers you to master the complexities of in-person payments and discover how to select the most cost-effective infrastructure for your specific needs. You'll find a transparent breakdown of industry costs, from purchase prices ranging between AED 2,000 and AED 7,000 to the latest hybrid settlement trends. We've simplified the selection process by highlighting terminals that support NFC, mobile wallets, and mandatory e-invoicing standards. By comparing the market through PaySelect, you can streamline your operations, accelerate your growth, and ensure your payment setup is ready for the digital future.

Key Takeaways

• Transition from traditional terminals to Android-powered smart devices to unlock better integration and sophisticated business functionality.

• Ensure your card machine supports 5G and Wi-Fi dual-connectivity to maintain a seamless checkout experience regardless of your location.

• Calculate the real cost of processing by comparing fixed monthly rentals against one-time purchase models and the Merchant Discount Rate.

• Align your hardware choice with your specific business model by auditing transaction volumes and mobility needs before committing to a contract.

• Discover how to use independent comparison platforms to bypass provider bias and secure the most transparent fee structures for your infrastructure.

What is a Modern Card Machine in the UAE Financial Landscape?

A What is a payment terminal in the context of a high-growth economy like the UAE? At its core, a card machine is the physical interface of your merchant account. It acts as a secure gateway that validates, authorizes, and records every in-person transaction. In 2026, the definition has expanded. We've seen a decisive shift from traditional "dumb" terminals to Android-powered smart devices. These modern machines offer the same flexibility as a smartphone, allowing you to run business apps, manage inventory, and sync data across your entire infrastructure in real time.

Security remains the highest priority for businesses looking to scale. Every modern terminal must adhere to strict PCI-DSS compliance standards. This global security framework ensures that sensitive cardholder data is encrypted and protected against fraud. As the UAE pushes toward its "Cashless 2030" vision, maintaining these standards is essential for building customer trust and avoiding heavy penalties. For smaller businesses or mobile vendors, "SoftPOS" technology offers a sleek alternative. This innovation allows you to accept payments directly on an NFC-enabled smartphone, turning existing hardware into a powerful tool for commerce without the need for a separate device.

The Evolution of In-Person Payments

The journey of payment technology in the region has been rapid. We've moved from magnetic stripes to EMV chip and PIN, and now to the total dominance of NFC (Near Field Communication). Contactless payments are no longer a luxury; they're a baseline expectation. With digital payments growing by 45% annually since 2024, your hardware must support digital wallets like Apple Pay, Google Pay, and Samsung Pay. This evolution ensures that your checkout process is fast, frictionless, and ready for a global audience that prefers tapping over swiping. It's a necessary step as Dubai works toward its goal of 90% digital transactions by the end of 2026.

Why Your Business Needs a Dedicated Terminal

Choosing a dedicated card machine is a strategic move for any entrepreneur. There's a direct correlation between accepting card payments and seeing an increase in average transaction values. Customers spend more when they have the freedom to use their preferred payment method. Beyond the sale, these terminals act as data hubs. They provide real-time analytics that help you identify peak trading hours and popular inventory items. This level of insight allows you to optimize your staffing and stock levels, turning a simple utility into a powerful tool for business transformation and growth.

Technical Specifications: Choosing the Right Infrastructure

Modern payment infrastructure is the backbone of transaction speed and reliability. In 2026, simply having a card machine isn't enough; your hardware must be a high-performance gateway capable of handling the UAE’s rapid digital shift. Accepting payments in the UAE now requires 5G and Wi-Fi dual-connectivity as a baseline standard. This redundancy ensures that if your primary network falters, the system switches instantly to a secondary signal, preventing lost sales and frustrated customers. Businesses implementing these advanced, contactless systems report up to a 60% reduction in transaction times, directly impacting your daily throughput and bottom line.

Security and maintenance have also evolved into a hands-off experience. You shouldn't have to manually update your devices or worry about outdated firmware. Leading solutions now utilize "Plug and Play" remote updates. This allows security patches and feature enhancements to be pushed to your device overnight without interrupting your operations. It’s an essential feature for maintaining PCI-DSS compliance and ensuring your business is always protected against emerging digital threats. If you're unsure which hardware fits your volume, you can compare modern POS machines to find a technical match for your specific industry.

Connectivity and Portability Standards

Your physical location dictates your connectivity needs. While fixed retail outlets rely on stable Wi-Fi, mobile businesses like food trucks or delivery services require robust 4G or 5G GPRS capabilities. The rise of "Mini POS" devices has transformed pop-up services, offering full functionality in a pocket-sized form factor. Even in areas with intermittent signals, ensure your device supports offline processing. This allows you to continue transacting securely, with payments syncing once the connection is restored, keeping your commerce borderless and uninterrupted.

Hardware Durability and User Interface

The transition toward large, intuitive touchscreens has streamlined the checkout process for both staff and customers. These interfaces must support dual-language functionality, as Arabic and English are required features for POS systems in the UAE market. When selecting a card machine, consider the environment. High-volume retail requires industrial-grade build quality that can withstand constant use, whereas a boutique might prioritize a sleek, ergonomic design. Additionally, consider your receipt strategy. While thermal printers remain common, the UAE’s move toward mandatory e-invoicing means your hardware should easily transition to digital-only receipts to stay ahead of 2026 regulations.

The Real Cost of a Card Machine: Beyond the Sticker Price

Many business owners focus solely on the upfront hardware price when choosing a card machine. This is a strategic oversight. The true expense of payment processing lies in the ongoing Merchant Discount Rate (MDR). In the UAE, transaction fees typically range from 2.5% to 3.5% of the transaction value. When you factor in additional flat fees per swipe, your total monthly cost often lands between 3.0% and 3.2% of your gross payment volume. It's also vital to remember that UAE law makes it illegal to pass these fees onto your customers; the cost is strictly a merchant's business expense.

Hidden costs often hide in the fine print of service agreements. You'll likely encounter setup fees, monthly statement fees, and minimum monthly volume requirements. If your sales drop below a specific threshold, some providers charge a penalty to cover their infrastructure costs. Another factor to monitor is Dynamic Currency Conversion (DCC). While DCC allows international tourists to pay in their home currency, the conversion margins are shared between the provider and the merchant. This can be a secondary revenue stream or a hidden cost depending on your contract's transparency. PaySelect helps you navigate these opaque structures by providing a side-by-side breakdown of these variables.

Understanding Transaction Fee Models

Fee structures generally fall into two categories: flat-rate or tiered pricing. Flat-rate models offer a single percentage for all transactions, providing predictable costs. Tiered pricing is more complex, distinguishing between local debit cards and international credit cards. While local transactions are generally more affordable, international fees can increase by an additional 1.5% due to cross-border processing. Always verify if your provider adds a fixed fee, such as AED 1.00 per transaction, as this significantly impacts businesses with low average ticket sizes.

Total Cost of Ownership (TCO) Analysis

To understand your financial commitment, calculate the Total Cost of Ownership (TCO) over a 12-month period. You must weigh the pros and cons of different hardware models:

Purchase Model

One-time payments for a complete EPOS package typically range from AED 2,000 to AED 7,000.

Rental Model

Monthly rentals start around AED 199, which preserves cash flow but costs more over several years.

The "Free" Trap

Hardware offered at zero cost often carries significantly higher transaction rates.

Identifying your break-even point is essential. If you're a high-volume business, paying more for the hardware upfront to secure a lower MDR will save you thousands of Dirhams annually. Using independent comparison tools ensures you don't overpay for "free" incentives that erode your long-term margins.

How to Select Your Provider: A Strategic Framework

Selecting the right card machine is a strategic decision that dictates your operational speed and long-term financial health. Don't simply sign with the first provider that offers a terminal. Instead, follow a structured framework to ensure your infrastructure supports your ambition to scale. First, audit your transaction volume and average ticket size. High-volume businesses must prioritize lower percentage-based MDRs, while those with smaller ticket sizes must avoid high flat per-transaction fees that quickly erode profit margins. Second, define your mobility needs. A fixed boutique requires stable Wi-Fi connectivity, whereas a delivery fleet requires 5G-enabled portability to maintain a seamless customer experience on the go.

Third, evaluate your integration requirements. In 2026, your terminal shouldn't exist in a vacuum; it should sync seamlessly with your ERP or accounting software to automate reconciliation and reduce human error. Fourth, compare settlement times. Cash flow is the lifeblood of your business. With Dubai aiming for 90% digital transactions by the end of 2026, waiting several days for your funds to clear is an unnecessary barrier to your growth. Finally, use a POS machine comparison tool to filter providers based on these specific technical and financial criteria. This logical flow removes the guesswork and ensures you partner with a provider that understands your unique business infrastructure.

Matching Industry Needs to Terminal Features

Every sector has distinct requirements that your hardware must accommodate. A generic solution often creates friction at the point of sale, slowing down your service and frustrating your team. Consider these industry-specific features during your search:

Retail

Prioritize high-speed processing and real-time inventory synchronization to prevent stockouts and accelerate the checkout line.

Hospitality

Look for advanced tipping functions, table management, and pre-authorization capabilities essential for hotel bookings and dining services.

Service Sector

Focus on portability, rugged build quality, and long battery life for field work, home deliveries, or pop-up events.

The Importance of Independent Advisory

Traditional bank-direct offers often lack the flexibility modern entrepreneurs require. While they project stability, their fee structures can be rigid and their technology slow to update. Fintech aggregators have simplified the selection process by offering more competitive rates and faster onboarding. This is especially critical for businesses serving international clients who demand "borderless" payment experiences. An independent advisor helps you identify which providers offer the best cross-border rates and multi-currency support without bias. By looking beyond traditional institutions, you can find a partner that views payment processing as a strategic tool for transformation. If you're ready to optimize your setup, take the test today to find your ideal match.

Streamlining Your Selection with PaySelect

PaySelect operates as the independent bridge between ambitious merchants and the complex landscape of financial providers. We don't sell hardware; we provide the clarity you need to choose the right infrastructure. Our proprietary "Take the Test" tool is designed to remove bias from the selection process. It filters through dozens of variables to match your specific volume, industry, and mobility needs with the most efficient partner. This ensures you never settle for a card machine based on a salesperson's pitch, but rather on data-backed performance metrics that align with your bottom line.

For businesses operating both online and offline, we offer the unique advantage of comparing payment gateways alongside physical POS solutions. This holistic view is vital for maintaining a unified financial ecosystem where data flows freely between your digital and physical storefronts. If you're managing enterprise-scale operations, our advisory services provide deep-dive optimization for your entire payment stack. We help you identify inefficiencies in your current setup and implement solutions that accelerate your settlement cycles and reduce operational friction across all touchpoints.

The PaySelect Advantage: Transparency and Speed

Manual research for a new payment provider can take weeks of sales meetings and confusing contract reviews. PaySelect slashes this timeline by providing immediate access to unbiased data on transaction costs and settlement terms. We empower you to make decisions in minutes that would otherwise take days. This efficiency is particularly valuable when you need to optimize your cross-border payment strategy. Our expert consulting ensures your business can handle international transactions with the same ease as local ones, removing the barriers to global expansion and ensuring your reach is truly borderless.

Empowering Your Business Growth

Future-Proof Your Payment Infrastructure

Your payment setup isn't just a utility; it's a strategic tool for business transformation. With the UAE's mandatory e-invoicing rollout beginning July 1, 2026, and large enterprises required to go live by January 1, 2027, the window to upgrade your infrastructure is closing. A modern card machine serves as the essential gateway to this digital future. It ensures your business remains compliant while capturing the 45% annual growth in digital payments seen across the region. By auditing your transaction volumes and identifying hidden fee structures, you position your brand for sustainable scaling.

PaySelect simplifies this transition by acting as your dedicated fintech partner. We offer an independent and unbiased comparison of the entire market, providing coverage across all major UAE payment providers. Our expert advisory focuses on cost optimization and settlement efficiency, removing the barriers that stall your cash flow. Find the perfect card machine for your business with PaySelect and lead your industry with absolute confidence. Your business is ready to embrace the borderless digital economy; make sure your technology is ready too.

Frequently Asked Questions

What is the average cost of a card machine in the UAE?

A card machine in the UAE typically costs between AED 2,000 and AED 7,000 for a one-time purchase. Alternatively, you can opt for rental models that start from approximately AED 199 per month. It's important to remember that these figures represent hardware costs only; you'll also pay transaction fees that generally average between 3.0% and 3.2% of your gross payment volume.

How long does it take to get a card machine for my business?

The onboarding process usually takes between 3 and 7 business days from the moment you submit your documentation. This timeline includes the verification of your trade license, the setup of your merchant account, and the physical delivery of the terminal to your location. Fintech-led providers often offer faster approval cycles than traditional banks, helping you start accepting payments without unnecessary delays.

Can I use a card machine without a local bank account?

You cannot use a card machine in the UAE without a local corporate bank account. Merchant service providers require a local account to settle your funds in AED and to comply with UAE Central Bank regulations. This ensures that your financial transactions are secure, transparent, and fully integrated into the local banking infrastructure for seamless cash flow management.

What is the difference between a POS terminal and a payment gateway?

A POS terminal is the physical hardware used to process card payments in person, while a payment gateway is the digital software used for online transactions. The terminal reads physical chips or NFC signals at your storefront. In contrast, the gateway encrypts and transmits card data from your website to the processor, acting as the virtual equivalent of a physical machine.

What documents are required to apply for a merchant account in the UAE?

You must provide a valid UAE Trade License, passport and Emirates ID copies of the owners, and a Memorandum of Association. Additionally, most providers require at least 3 to 6 months of corporate bank statements to verify your business activity. Having these documents prepared in advance accelerates the application process and helps you avoid common setup pain points.

Are there card machines that don’t require a monthly rental fee?

Yes, many providers offer a "one-time purchase" model that eliminates recurring monthly rental fees. A complete EPOS package can be purchased for a single payment of around AED 3,499. While the initial investment is higher, this model is often more cost-effective for established businesses that want to reduce their long-term monthly overhead and own their hardware outright.

How do I reduce the transaction fees on my current card machine?

To reduce your fees, you should perform a detailed audit of your current Merchant Discount Rate (MDR) against your monthly transaction volume. If your volume has increased significantly, you can often negotiate a more competitive rate with your provider. Alternatively, switching to an Interchange++ pricing model offers greater transparency and can lower costs by breaking down fees into their base components.

What happens if my card machine loses internet connection?

Modern terminals are designed with 5G and Wi-Fi dual-connectivity to prevent downtime if one network fails. If all connectivity is lost, many devices support an "offline processing" mode that stores transaction data securely. Once the connection is restored, the device automatically syncs the data and completes the settlements, ensuring your business never misses a sale due to technical issues.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.