The UAE Payment Gateway Landscape in 2026: A Strategic Overview

Selecting a payment gateway in the UAE is no longer a simple technical task; it is a critical financial decision that directly impacts your profitability, customer experience, and ability to scale. A payment gateway acts as the secure bridge between your business, your customers, and the complex network of banks and card schemes. It authorises transactions in real-time, ensuring funds are transferred securely and efficiently from the customer's account to yours.

The UAE's fintech sector has matured rapidly, moving beyond basic transaction processing to offer sophisticated financial ecosystems. For business leaders, 2026 represents a pivotal moment where digital commerce standards, driven by national economic ambitions and regulatory oversight from the Central Bank of the UAE, demand a more strategic approach to payment infrastructure.

The Shift from Utility to Strategic Asset

In today's competitive market, your payment infrastructure is a strategic asset that influences customer conversion and long-term retention. A seamless, fast, and reliable checkout experience builds trust, while a clunky or slow process can lead to abandoned carts and lost revenue. As the UAE pushes towards a borderless digital economy, the right gateway becomes an enabler of growth, not just a utility for processing sales. Understanding the fundamental differences between providers is the first step in building this asset. To learn more, you can explore various payment gateway types and how they fit different business models.

Key Categories and Market Dynamics

The UAE market features a diverse range of providers, which can generally be grouped into several categories. These include established regional champions with deep local knowledge and global technology giants offering extensive international networks. Alongside these are niche providers that cater to specific industries with tailored solutions. A crucial distinction for any business is understanding the difference between an aggregator model and a direct merchant account. Aggregators offer faster onboarding and simpler integration, making them ideal for startups, while direct accounts provide greater control and potentially lower rates for high-volume enterprises.

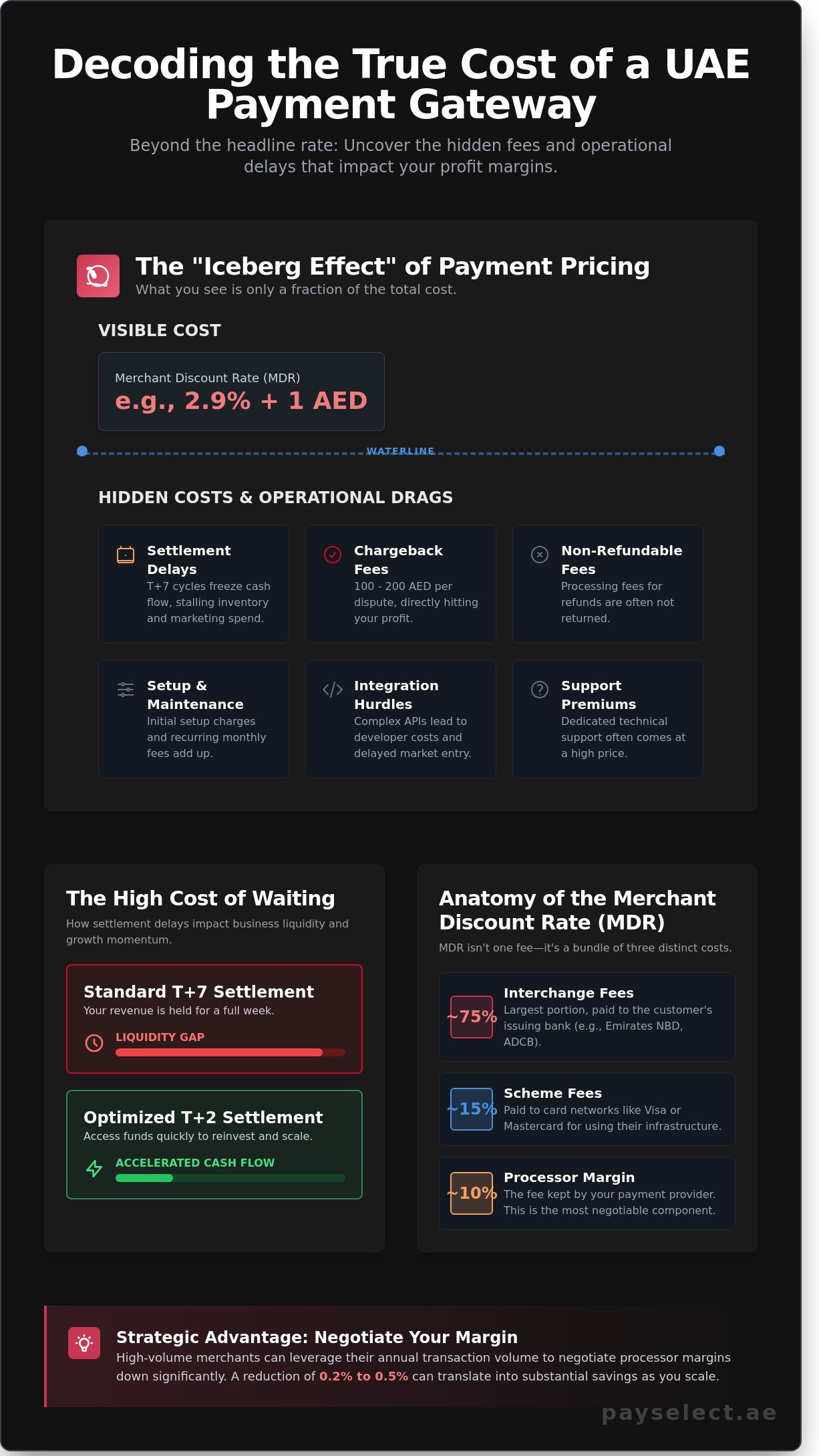

Beyond Transaction Fees: Decoding the True Cost of a Payment Gateway

The headline transaction fee, or Merchant Discount Rate (MDR), is just the tip of the iceberg when it comes to the true cost of payment processing. A comprehensive evaluation requires a deep dive into the Total Cost of Ownership (TCO), uncovering the hidden fees and operational impacts that affect your bottom line.

The Iceberg Effect

Many pricing structures contain costs that are not immediately obvious, such as setup fees, monthly maintenance charges, and fees for technical support.

Settlement Cycles

The time it takes for funds to reach your bank account (e.g., T+2 or T+7 days) directly impacts your operational liquidity and cash flow. Longer cycles can strain working capital.

Hidden Costs

Be aware of charges for ancillary services like chargebacks, refunds, and international card processing, which can accumulate significantly over time.

The Merchant Discount Rate (MDR) Explained

The MDR is a percentage of each transaction that is paid to the payment provider. It is not a single fee but a combination of three key components: the interchange fee (paid to the customer's bank), the scheme fee (paid to the card network like Visa or Mastercard), and the processor's margin. This rate often varies based on the card type used, with different fees for domestic, international, and corporate cards. Businesses with significant transaction volume are often in a strong position to negotiate more favourable MDRs.

Foreign Exchange (FX) and Cross-Border Optimisation

For businesses serving an international clientele, accepting payments in non-AED currencies introduces another layer of cost. Many gateways apply a hidden markup on their foreign exchange conversion rates, which can erode your margins on every cross-border sale. Understanding these FX costs is essential for accurate financial planning. Furthermore, while some providers offer dynamic currency conversion (DCC) as a feature, it's important to know how it is implemented and whether the benefit is passed to you or solely to the processor. A well-structured gateway can help you optimise cross-border payments and minimise currency-related losses.

Infrastructure and Integration Costs

The initial setup and ongoing maintenance of your payment integration contribute to its TCO. A complex API may require significant developer hours, while a simple plug-and-play solution can get you to market faster. However, the most significant infrastructure cost can be poor uptime. Every minute your gateway is down during a peak sales period translates to direct revenue loss and damages customer trust. Total Cost of Ownership in the context of UAE payment gateways extends beyond transaction fees to include integration expenses, currency conversion markups, and the financial impact of settlement delays and system downtime.

A Framework for Evaluation: Comparing UAE Providers on Value

An effective evaluation moves beyond a simple price comparison to assess providers based on technical performance, regulatory expertise, and support quality. The right partner offers more than just processing; they provide a resilient and scalable foundation for your business growth.

Technical Agility

Does the provider’s technology support your future product roadmap, including subscriptions, mobile payments, and marketplace functionalities?

Local Knowledge

How well does the provider understand UAE-specific regulations and consumer payment preferences?

API Flexibility

A well-documented and flexible API is crucial for creating custom checkout experiences and integrating payments deep within your existing software stack.

Dashboard Analytics

Powerful reporting and analytics tools provide the financial insights needed to make data-driven decisions and reconcile transactions efficiently.

Technical Reliability and Uptime

For any serious e-commerce or digital business, an uptime of 99.9% should be considered the absolute minimum standard. Ask potential providers about their server redundancy and failover mechanisms, which ensure continuous service even if one component fails. High latency, or slow response times, during the checkout process is a primary driver of cart abandonment, making speed as critical as reliability.

Security, Compliance, and Trust

Security is non-negotiable in digital payments. All reputable providers in the UAE must be PCI-DSS Level 1 compliant, the highest standard for data security in the payments industry. Modern gateways should also support 3D Secure 2.0 (3DS2), an authentication protocol that helps reduce fraud while minimising friction for legitimate customers. Furthermore, understanding local data residency laws and ensuring your provider complies with them is essential for avoiding regulatory penalties.

Customer Support and Account Management

When issues arise, access to timely and knowledgeable support is invaluable. The value of having a dedicated relationship manager who operates in the UAE time zone cannot be overstated, especially for resolving complex settlement or technical queries. While self-service portals are useful, enterprise-scale businesses require a higher level of support to troubleshoot API issues and optimise their payment performance.

Tailoring Your Stack: Selection Criteria for Every Business Stage

The ideal payment gateway for a startup is often different from what an established enterprise requires. Matching a provider's capabilities to your specific business model, scale, and industry is key to building a future-proof payment stack.

Startup Checklist

Focus on speed to market, low or no setup fees, and simple, user-friendly integrations.

Enterprise Requirements

Prioritise deep customisation options, preferential pricing for high transaction volumes, and sophisticated reporting and reconciliation tools.

Industry Nuances

A SaaS business with recurring billing has different needs than a hospitality group managing online bookings or an e-commerce store with high-volume, low-value transactions.

Solutions for High-Growth Startups

For early-stage businesses, no-code or low-code integrations via plugins for popular e-commerce platforms are often the fastest way to start accepting payments. Features like payment links are incredibly powerful for selling through social media, WhatsApp, or email invoices without needing a full website. As the business scales, the ability to transition smoothly from a simple hosted checkout page to a fully embedded API becomes a critical factor.

Optimising Enterprise and Multi-Entity Infrastructure

Large organisations often struggle with fragmented payment systems across different brands or locations. The right gateway can help consolidate these disparate streams into a single, unified reporting dashboard, providing a clear source of truth for financial teams. For ultimate flexibility and redundancy, many enterprises adopt a payment orchestration layer to manage multiple gateways simultaneously. This strategy can also involve integrating online gateways with physical POS systems for a true omnichannel commerce experience.

Navigating Cross-Border and GCC Expansion

If your growth strategy includes expanding into neighbouring GCC markets, select a gateway that simplifies this process. A provider with a strong regional footprint can allow you to accept local payment methods popular in other countries, such as Mada or KNET, through a single technical integration based in the UAE. A unified GCC payment stack provides a strategic advantage by centralising financial reporting, simplifying technical maintenance, and creating a consistent customer checkout experience across multiple countries.

Streamlining Your Selection with PaySelect Independent Advisory

The payment gateway market is crowded with marketing claims and complex pricing sheets. PaySelect cuts through the noise by providing an independent, data-driven framework to help you make the right choice for your business. We remove the bias from the selection process, empowering you to compare providers on the factors that truly matter.

Unbiased Comparison

Our tools and advisory services are provider-agnostic, ensuring our recommendations are aligned exclusively with your business needs.

Cost Optimisation

We help you move beyond selection to continuous optimisation, using our expertise to uncover hidden fees and negotiate better rates.

Strategic Guidance

The PaySelect advisory journey is a partnership focused on building a payment infrastructure that supports your long-term growth ambitions.

The Power of Independent Data

Our provider-agnostic approach ensures that the advice you receive is objective and focused on protecting your interests as a merchant. We provide access to transparent pricing and performance data that is not readily available on public websites, giving you a distinct advantage in negotiations. For large-scale national organisations, we facilitate a structured Request for Proposal (RFP) process to ensure all technical, commercial, and legal requirements are met.

Infrastructure Audits and Cost Optimisation

Many businesses unknowingly suffer from revenue leakage within their existing payment stack due to suboptimal routing, high chargeback rates, or punitive FX markups. A professional payment infrastructure audit from PaySelect can identify these weak points and deliver a clear, actionable plan to fix them. The return on investment from a strategic re-selection or renegotiation often results in significant, recurring savings on processing costs.

Get Started with Your Optimised Payment Strategy

Upgrading your payment gateway is one of the highest-impact decisions you can make for your digital business. The first step is to understand your options in the current market. Use the PaySelect comparison tool for an instant scan of leading providers, or contact our advisory team for a comprehensive audit of your existing infrastructure.

Optimise your payment stack with PaySelect today

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.