The Strategic Guide to Business International Money Transfers in the UAE (2026)

Did you know that traditional exchange rate markups can reach 5%, effectively costing your business 5,000 AED for every 100,000 AED sent abroad? These hidden costs, combined with correspondent bank fees as high as 400 AED per transaction, often turn business international money transfers into a significant drain on your bottom line. It's frustrating to manage global growth when opaque pricing and slow settlement times disrupt your cash flow and erode your hard-earned margins.

You deserve a payment infrastructure that works as hard as you do. This guide provides a professional framework to master the complexities of global commerce by evaluating modern cross-border solutions and optimizing your transaction costs. PaySelect simplifies this process by allowing you to compare different payment partners, helping you move from legacy systems to a high-performance technical stack that offers transparent fee structures and seamless ERP integration.

We'll explore the impact of the Federal Decree-Law No. (6) of 2025 and the mandatory transition to ISO 20022 standards. You'll learn how to identify the right payment partners to ensure faster settlement and absolute regulatory compliance. By the end of this article, you'll have the strategic tools needed to transform your international payments from an operational burden into a competitive advantage.

Key Takeaways

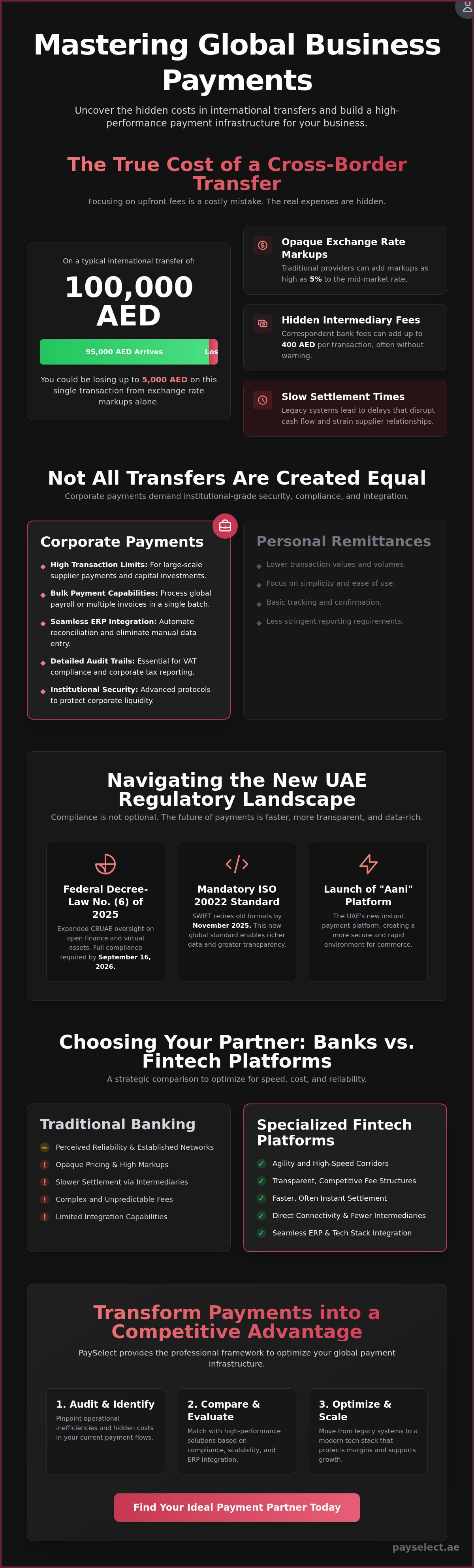

• Distinguish corporate liquidity requirements from personal remittances to ensure your cross-border operations meet institutional security and compliance standards.

• Identify the total cost of business international money transfers by auditing opaque exchange rate markups and hidden intermediary fees that erode profit margins.

• Evaluate the strategic trade-offs between the reliability of traditional banking and the agility of specialized fintech platforms to optimize your settlement speed.

• Apply a professional framework to select payment partners based on their regulatory compliance, technical scalability, and seamless ERP integration capabilities.

• Optimize your payment infrastructure by identifying operational inefficiencies and matching with high-performance global solutions through expert comparison tools.

The Landscape of Business International Money Transfers

The UAE has cemented its position as the world's second-largest hub for outbound remittances, trailing only the United States. For local enterprises, business international money transfers represent more than just a logistical task; they are a critical component of corporate liquidity management. In a market where high-value transactions are the norm, the ability to move capital across borders with precision and speed is a significant competitive advantage. While many are familiar with the basic concept of understanding wire transfers, the corporate requirements in 2026 have evolved far beyond simple bank-to-bank messaging. Modern businesses now operate within a complex ecosystem where traditional SWIFT banking coexists with high-speed fintech corridors and real-time payment rails.

The shift toward digital-first infrastructure is driven by the need for greater efficiency. Traditional systems often involve multiple intermediary banks, leading to settlement delays and unpredictable fees. In contrast, the current landscape favors solutions that offer direct connectivity and instant settlement. This transition is not merely about technology; it's about protecting profit margins. When a single transaction can involve hundreds of thousands of Dirhams, even a minor delay or a slight exchange rate markup can have a measurable impact on a company's bottom line. PaySelect supports this evolution by providing cross-border payment solution matching, helping businesses identify which providers offer the best technical fit for their specific trade corridors.

Commercial vs. Personal Transfer Requirements

Business transfers demand a level of rigor that personal remittances simply don't require. Corporate entities deal with significantly higher transaction limits and the necessity for bulk payment capabilities to manage global payroll or supplier invoices. Beyond the volume, VAT compliance and corporate tax reporting necessitate detailed audit trails for every Dirham moved. Modern businesses require seamless integration between their payment providers and existing ERP systems to automate reconciliation. This connectivity eliminates manual data entry, reduces human error, and ensures that financial records remain accurate and ready for regulatory inspection at any moment.

This level of precision is equally vital when analyzing the underlying assets of a transaction. For instance, businesses managing property portfolios often integrate independent market scoring from YALLA2X to verify historical listing data, ensuring that their high-value international transfers are aligned with current market valuations.

The Evolution of the UAE Payment Ecosystem

The regulatory environment in the UAE has undergone a major transformation with the implementation of Federal Decree-Law No. (6) of 2025. This law, which came into force in September 2025, expanded the Central Bank of the UAE's (CBUAE) oversight to include open finance and payment services using virtual assets. Financial institutions have until September 16, 2026, to fully comply with these strict new provisions. Simultaneously, the UAE is adopting the ISO 20022 global standard for financial messaging. As SWIFT retires older message formats by November 2025, the move to the data-rich MX format becomes mandatory. These changes, alongside the launch of the "Aani" instant payment platform, are creating a more transparent, secure, and rapid environment for international commerce.

Analyzing the Total Cost of Cross-Border Transactions

Many executives focus solely on the upfront service fee when initiating business international money transfers. This narrow focus is a mistake. Research indicates that the total cost of a traditional cross-border transaction can range from 3% to 7% of the payment value once all fees and markups are included. Understanding these costs is essential for maintaining healthy profit margins, especially as global remittance trends show an increasing volume of capital moving through the UAE's corridors. When you ignore the secondary layers of pricing, you risk a significant erosion of your corporate liquidity.

The true expense of moving money internationally is often hidden in the exchange rate. While a bank might advertise a low transaction fee, they frequently apply a significant markup to the mid-market rate. In the UAE, traditional banks and some payment providers apply markups as high as 5%. On a transfer of AED 100,000, this single "hidden tax" results in a loss of AED 5,000. This lack of transparency is a widespread issue; approximately 92% of traditional banks are not fully transparent about their currency conversion fees. When you factor in correspondent bank fees, which can reach AED 400 per transaction, the financial impact on your supplier relationships and bottom line becomes clear. You can use PaySelect's payment pricing comparison to audit these costs and identify more efficient alternatives.

Decoding Exchange Rate Mark-ups

The mid-market rate, or interbank rate, is the real-time price at which banks trade currencies with one another. Most providers don't offer this rate to businesses. Instead, they quote a "retail" rate that includes a spread. An FX mark-up is the difference between the interbank rate and the rate offered to the business. To calculate the real cost you're paying, subtract the provider's quoted rate from the current mid-market rate and multiply it by the total transaction volume. This simple audit often reveals that the "free" or "low-cost" transfer is actually the most expensive option in your stack.

Operational Fees and Hidden Surcharges

Beyond the exchange rate, you must account for fixed and variable operational fees. Major banks in the UAE typically charge SWIFT transfer fees ranging from AED 50 to AED 100 per transaction. These are often supplemented by intermediary bank charges deducted during the transfer process without prior notification. If a transfer fails due to incorrect data or regulatory flags, the cost of returning the funds can be substantial. Choosing a provider that offers validated payment rails and transparent fee structures ensures your suppliers receive the exact amount intended, protecting your reputation and operational fluidity.

Banks vs. Specialized Platforms: A Strategic Comparison

Choosing the right partner for business international money transfers is a strategic decision that defines your operational rhythm. It's no longer just about who you've banked with for decades; it's about finding the balance between institutional stability and digital agility. In the UAE's fast-moving economy, the choice between a legacy bank and a specialized platform impacts everything from settlement speed to your annual profit margins. Both options have distinct profiles that cater to different corporate needs and transaction volumes.

Security is a non-negotiable prerequisite in this landscape. Whether you choose a traditional bank or a fintech innovator, both must now operate under the expanded regulatory scope of the Central Bank of the UAE. With the implementation of Federal Decree-Law No. (6) of 2025, the standards for compliance and consumer protection have reached a new peak. The real differentiator now lies in the user experience and the technical utility of the platform. High-frequency finance teams require intuitive dashboards that offer clear visibility and remove the friction of manual data entry. PaySelect acts as a bridge in this decision process, helping you compare these providers to find the most efficient fit for your business.

Traditional UAE Banking Institutions

Traditional banks remain the rock-solid choice for large-scale institutional movements and complex financing. Their primary advantage is the depth of the relationship and the ability to handle exceptionally high-value limits within integrated accounts. However, the cons are often felt in the wallet and the clock. Legacy systems frequently involve slower processing times and higher FX spreads, with total costs often ranging between 3% and 7%. While some major banks have launched instant corridors to specific markets like the UK or India, many still rely on traditional rails that can take 2 to 5 business days for settlement. This delay is a significant pain point for businesses requiring immediate liquidity.

Digital-First Payment Specialists

Specialized fintech platforms are winning market share by focusing on performance enhancement and cost optimization. These providers often offer competitive FX rates and total transaction costs as low as 0.4% to 0.8%, which is a fraction of what traditional banks charge. Their strength lies in agility, offering real-time tracking and modern API connectivity that legacy banks struggle to match. For companies exploring cross-border payments, these specialists provide the fluidity needed for modern commerce. The trade-off is that they may require separate account funding and offer varied levels of customer support, making an independent comparison essential before implementation.

Key Criteria for Selecting an International Payment Partner

Selecting a partner for business international money transfers isn't just a one-time setup; it's a long-term strategic alignment. In the UAE, where the regulatory environment is rapidly tightening, your choice must be based on more than just the lowest headline fee. You need a partner that ensures your capital moves legally, efficiently, and predictably. A high-performance technical stack is no longer a luxury. It's a requirement for any business looking to maintain its edge in a fast-moving digital economy.

Compliance is the most critical pillar of your selection process. The Federal Decree-Law No. (6) of 2025 has significantly increased the stakes for financial violations, with administrative fines now reaching up to AED 1 billion in some cases. Your provider must demonstrate absolute adherence to UAE Anti-Money Laundering (AML) regulations and be ready for the full implementation of these rules by September 2026. Beyond legal safety, you should evaluate how easily a provider's systems integrate with your existing ERP or accounting software. This connectivity turns manual reconciliation into an automated process, allowing your finance team to focus on growth rather than data entry. If you're ready to optimize your setup, you can use PaySelect's cross-border payment solution matching to find a partner that meets these rigorous standards.

Risk Management and FX Tools

Volatility in global currency markets can quickly turn a profitable international contract into a financial loss. Sophisticated businesses use risk management tools like forward contracts and market orders to mitigate this danger. Forward contracts protect profit margins from currency volatility by allowing businesses to lock in a specific exchange rate for a future date. Automated hedging strategies also ensure your costs remain predictable even when the market shifts. These technical tools transform your finance department from a reactive cost center into a strategic asset for international expansion.

Customer Support and Operational Fluidity

Operational barriers often appear when payments get "stuck" within the global correspondent banking network. This is where dedicated account management becomes indispensable for corporate clients. Unlike personal remittance apps, professional platforms provide direct access to experts who can trace funds and resolve bottlenecks quickly. Fluidity is also maintained through intuitive dashboard design. A well-designed interface allows your team to manage high-frequency transfers without friction, ensuring your international ambition is never slowed down by poor technical utility. If disputes arise with traditional institutions, the new financial ombudsman, Sanadak, now provides a unified resolution process to protect your interests.

Optimizing Your Infrastructure with PaySelect

Most traditional guides focus on the mechanics of a single transaction. We take a different approach by focusing on your entire financial architecture. PaySelect identifies the specific friction points in your current setup that lead to settlement delays and margin erosion. By conducting a Payment Cost Optimization Audit, we expose the opaque fee structures and high FX markups that often go unnoticed in high-volume environments. Your business international money transfers shouldn't be an operational burden; they should be a source of strategic efficiency that supports your global expansion.

Our "Take the Test" tool provides a data-driven framework for selection. It matches your specific transaction volume, target trade corridors, and technical requirements with the right global partners. This process removes the guesswork from procurement, ensuring you don't settle for a provider that can't scale with your ambition. For large-scale organizations and hotel groups who may need to explore Marble Slabs from Altays Trading LLC for high-end developments, our bespoke advisory services offer a deep dive into complex payment ecosystems. We help you build a stack that is fully compliant with the Central Bank of the UAE’s mandates while maintaining the fluidity required for modern commerce.

Leveraging Independent Advisory

In an industry where most voices are biased toward their own processing services, PaySelect remains a strictly independent advisor. We provide an objective perspective that prioritizes your ultimate business outcome over any specific provider's bottom line. This independence is essential for moving beyond generic solutions to a bespoke infrastructure. For many businesses, this involves integrating high-performance payment gateways with their cross-border transfer solutions. This creates a seamless flow of capital from the moment of collection to final disbursement, removing the operational barriers that slow down traditional finance teams.

Taking the Next Step Toward Efficiency

The journey toward optimization begins with a comprehensive audit of your existing payment stack. We analyze your current contracts, verify exchange rate markups against real-time mid-market data, and identify redundant intermediary fees that can be eliminated. With the September 16, 2026, compliance deadline approaching for the new Federal Decree-Law, there's no better time to ensure your infrastructure is both legal and lean. A streamlined payment stack provides long-term value by protecting your margins and ensuring absolute regulatory certainty. Use the PaySelect platform today to compare providers and select the right partner for your next phase of international growth.

Mastering Your Global Capital Flow

Mastering your global capital flow requires moving beyond legacy banking habits to embrace a high-performance technical stack. You've identified how auditing hidden exchange rate markups and ensuring compliance with the latest Central Bank of the UAE regulations protects your profit margins. By prioritizing seamless ERP integration and faster settlement times, you transform your finance department from a cost center into a strategic engine for international growth. It's time to replace opaque fee structures with absolute clarity and operational fluidity.

Optimizing business international money transfers doesn't have to be a manual burden. PaySelect provides the independent advisory and bespoke payment infrastructure audits needed for enterprise-scale organizations to thrive in the MENA region. Our expert guidance from regional specialists helps you remove operational barriers and secure your competitive edge in a digital-first economy. This structured approach ensures your capital remains as mobile as your business ambitions.

Match your business with the ideal cross-border payment solution and start building a more resilient, cost-effective infrastructure today. Your international expansion deserves a partner that understands the nuances of the modern economy and values your efficiency.

Frequently Asked Questions

Is it cheaper to use a bank or a specialist provider for business transfers?

Specialist providers are generally more cost-effective than traditional banks for most corporate needs. While traditional banks often apply exchange rate markups as high as 5%, specialized fintech platforms frequently offer rates much closer to the mid-market price. These providers can reduce the total cost of business international money transfers to between 0.4% and 0.8%, which is a significant saving compared to the 3% to 7% typically charged by legacy institutions.

How long do business international money transfers typically take in the UAE?

Settlement times depend on the specific payment rail used by your provider. Traditional SWIFT transfers usually require 2 to 5 business days to clear. However, many modern platforms and specific bank corridors now offer near-instant settlement. For example, transfers from the UAE to countries like the UK, India, and the Philippines can often be completed within 60 minutes through specialized real-time payment corridors.

What documents are required for UAE businesses to send money abroad?

To comply with strict AML regulations, businesses must provide a standard set of corporate documents. This typically includes a valid Trade License, the Memorandum of Association, and the Emirates ID or passport copies of all ultimate beneficial owners. You'll also need to provide supporting documentation for the transaction itself, such as a commercial invoice or a signed contract, to verify the source of funds and the purpose of the payment.

Can I lock in an exchange rate for future business payments?

Yes, many specialized payment partners offer forward contracts as a core risk management tool. This allows your business to secure a specific exchange rate for a payment scheduled for a future date, protecting your profit margins from sudden currency volatility. It's a strategic way to ensure that your business international money transfers remain within budget, regardless of how the global markets shift before the settlement date.

Are international payment platforms as secure as traditional UAE banks?

Licensed international payment platforms must adhere to the same rigorous security standards as traditional financial institutions. The Central Bank of the UAE regulates all authorized providers under Federal Decree-Law No. (6) of 2025, ensuring they maintain high levels of capital adequacy and consumer protection. These platforms utilize advanced encryption and follow global standards like ISO 20022 to ensure your corporate data and funds remain secure throughout the transfer process.

How do I avoid hidden fees in cross-border business transactions?

The best way to avoid hidden costs is to demand a transparent breakdown of the "all-in" price before you commit to a transfer. This includes the upfront service fee, the exchange rate markup, and any potential correspondent bank charges, which can reach AED 400. Using an independent comparison tool like PaySelect helps you identify providers that offer fixed, transparent fee structures and helps you move away from opaque legacy pricing models.

What is the Central Bank of the UAE’s role in international transfers?

The Central Bank of the UAE (CBUAE) is the primary regulatory body responsible for overseeing the stability and integrity of the financial system. It sets the rules for licensing payment providers, enforces anti-money laundering (AML) compliance, and manages national payment infrastructures like the "Aani" platform. The 2025 legal framework expanded the CBUAE's powers to include the regulation of open finance and payment services involving virtual assets, ensuring a secure environment for global commerce.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.