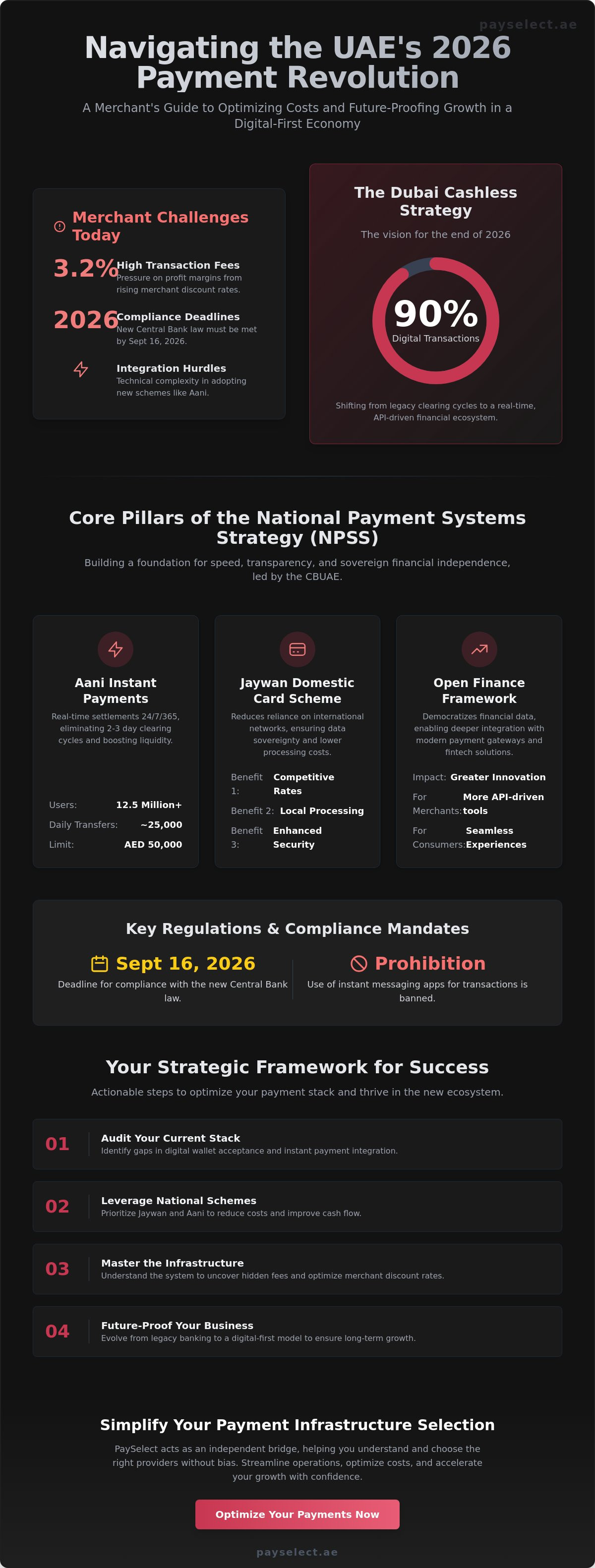

Did you know that by the end of 2026, the Dubai Cashless Strategy aims for 90% of all transactions to be digital? As you transition toward this goal, you've likely felt the weight of transaction fees reaching 3.2% and the pressure to meet the September 16, 2026, compliance deadline for the new Central Bank law. Mastering the evolving UAE Payment Infrastructure is no longer a utility; it's a strategic move to protect your margins and accelerate your growth.

We recognize the frustration of reconciling cross-border payments and the technical hurdles of integrating instant schemes like Aani. This guide empowers you to optimize costs, reduce merchant discount rates, and secure a future-proofed financial architecture. You'll learn how to meet new regulatory restrictions on messaging-based transactions, leverage domestic card schemes, and implement a borderless payment strategy. We'll show you how to streamline your operations, integrate with national schemes, and scale with absolute confidence.

Key Takeaways

• Understand the evolution from legacy banking to a digital-first ecosystem to future-proof your business operations.

• Leverage national schemes to enhance your business liquidity and reduce dependency on international payment networks.

• Master the UAE Payment Infrastructure to identify hidden processing fees and significantly optimize your merchant discount rates.

• Audit your current payment stack to bridge critical gaps in digital wallet acceptance and instant payment integration.

• Discover how to use independent matching tools to select the ideal payment providers based on your specific industry requirements.

Understanding the UAE Payment Infrastructure in 2026

The UAE Payment Infrastructure is the invisible network of technology, regulations, and institutions that ensures money moves safely between businesses and consumers. It has evolved from a traditional banking model into a sophisticated, digital-first ecosystem. This transformation is central to the UAE's diversified economy, which continues to move beyond oil to become a global financial leader. The Central Bank of the UAE (CBUAE) leads this change through the National Payment Systems Strategy (NPSS). This strategy prioritizes interoperability, ensuring that whether a customer pays via a card, a phone, or a QR code, the transaction is fast, secure, and reliable.

The Evolution of Digital Payments

The landscape has shifted rapidly from cash-heavy operations to a digital mandate. Government initiatives like the Dubai Cashless Strategy aim for 90% of all transactions to be digital by 2026. This shift replaces slow, legacy clearing cycles with real-time settlements, improving business liquidity instantly. Merchants no longer have to wait days for funds to reflect in their accounts. Instead, the current infrastructure supports a seamless, API-driven flow that eliminates the friction of traditional banking. By the end of 2026, the UAE will be one of the most digitally advanced payment markets in the world, with mobile and instant transfers becoming the primary method of commerce.

Key Regulatory Bodies and Their Impact

Al Etihad Payments, a subsidiary of the CBUAE, operates the core national infrastructure, including the Aani platform which has already surpassed 12.5 million users. These bodies have introduced Open Finance frameworks that democratize financial data, allowing businesses to integrate more deeply with modern payment gateways. Compliance is no longer optional; the deadline of September 16, 2026, for the new Central Bank law requires all entities to align with these national standards. This includes strict adherence to new rules, such as the prohibition of using instant messaging apps for customer transactions, which came into effect in April 2026. Adhering to these regulations is a prerequisite for any merchant looking to scale their operations securely.

Navigating these changes can be difficult for business owners who face high transaction fees and complex integration hurdles. PaySelect acts as an independent bridge, helping you understand the differences between various providers without bias. We simplify the complexities of the UAE Payment Infrastructure so you can focus on growth. Our goal is to empower your business to streamline operations, optimize costs, and accelerate your expansion across the region.

Core Pillars of the National Payment Systems Strategy

The UAE Payment Infrastructure rests on several strategic pillars designed to modernize how businesses handle capital. The National Payment Systems Strategy isn't just about moving money; it's about building a foundation for speed, transparency, and sovereign financial independence. This Payments evolution in the UAE reflects a move toward a digital-first economy where every transaction adds value to the business ecosystem. Key to this is the integration of cross-border payment solutions that align with local standards. Additionally, the Wage Protection System (WPS) remains a critical component, ensuring payroll compliance is baked into the national digital framework to protect both employers and employees.

Instant Payments and Cash Flow Management

The Aani platform is the centerpiece of the Instant Payment Platform (IPP). It already processes approximately 25,000 transfers daily using only mobile numbers, proving that the market is ready for speed. For a merchant, this technology removes the standard 2-3 day waiting period for funds to clear. You get immediate access to liquidity. With a transaction limit of up to AED 50,000, Aani allows for substantial B2B and B2C volume to move 24/7/365. Managing liquidity becomes simpler when you have real-time data at your fingertips. You can restock inventory, pay vendors, or manage payroll without the lag associated with legacy bank transfers. This constant availability ensures your business never stops moving, even during weekends or public holidays.

Domestic vs. International Card Schemes

The launch of Jaywan, the UAE’s domestic card scheme, marks a major change in the local ecosystem. Jaywan reduces the reliance on international networks, ensuring that payment data is processed and stored within the country. For merchants, this often leads to more competitive processing rates compared to traditional global schemes. While total monthly processing costs for credit cards often sit between 3.0% and 3.2%, domestic schemes aim to optimize these figures by removing international routing fees. Security is also a major focus, as local routing provides a direct line to national fraud detection systems. This localized approach improves merchant acceptance rates and fosters financial inclusion across the Emirates. It's a strategic shift that empowers local businesses to keep more of their revenue while providing a seamless experience for their customers.

If your business deals with international suppliers, you can streamline your global transfers to match the efficiency of these local systems. PaySelect helps you bridge the gap between these national pillars and your daily operations, ensuring you always use the most efficient path for your capital.

Overcoming Merchant Challenges in the Local Ecosystem

Navigating the fragmented provider landscape is the primary hurdle for most merchants. You're often forced to choose between legacy reliability and modern speed, but rarely get both without facing high costs. Many businesses struggle with a "one-size-fits-all" approach that doesn't account for their specific transaction volumes or industry needs. This fragmentation leads to operational friction, making it difficult to maintain a consistent customer experience across different channels.

High Merchant Discount Rates (MDR) and hidden processing fees represent a significant drain on your bottom line. A merchant processing AED 200,000 monthly can expect to pay around AED 5,500 in processing fees alone. When you include VAT and potential foreign exchange charges, total monthly costs often reach between 3.0% and 3.2% of gross payment volume. The UAE National Payment Systems Strategy addresses this by promoting domestic schemes like Jaywan. These initiatives aim to lower the cost of doing business by bypassing international interchange markups and keeping data local.

Decoding Transaction Costs and Fees

Typical transaction fees are a combination of interchange, scheme, and acquirer fees. Understanding this breakdown is essential for optimization. National infrastructure projects are actively working to cap these costs, especially for domestic transactions. You should look for transparent pricing models, such as Interchange++, which break down every cost component. This transparency allows you to see exactly how much you're paying for the network versus the service, empowering you to negotiate better terms as your volume grows.

Integration and Technical Scalability

Integrating a payment gateway into a legacy system shouldn't take months. Modern API-first architectures allow you to scale without rebuilding your entire stack. We're seeing a rise in low-code and no-code options that help retailers quickly ditch cash on delivery, which still accounts for 20-25% of e-commerce orders. The real challenge is balancing this speed with security. By September 16, 2026, all entities must ensure full compliance with the new Central Bank law. This includes moving away from insecure instant messaging platforms for transactions and maintaining rigorous PCI-DSS standards. PaySelect helps you bridge these gaps by acting as an independent partner, matching your merchant needs with the right infrastructure to ensure you don't sacrifice security for settlement speed.

Strategic Framework for Optimizing Your Payment Stack

Building a resilient financial foundation requires a structured approach to your UAE Payment Infrastructure. You can't manage what you don't measure. Optimization begins with a cold, hard look at your current data to find where capital is leaking. A strategic framework ensures you aren't just reacting to new regulations, such as the September 2026 compliance deadline, but actively using them to gain a competitive edge. Follow these five steps to streamline your operations.

Step 1: Audit

your current transaction volumes and fee structures to establish a baseline for performance.

Step 2: Identify gaps

in payment method acceptance. If you aren't yet integrated with instant schemes or popular digital wallets, you're likely losing customers at the checkout.

Step 3: Evaluate hardware

requirements for POS systems in your physical locations to ensure they support contactless and mobile payments.

Step 4: Assess cross-border needs

for multi-currency capabilities, especially if you deal with international suppliers or a global customer base.

Step 5: Select providers

that offer the best balance of cost, technology, and proactive support.

Auditing Your Current Infrastructure

Successful optimization depends on tracking three key metrics: transaction success rates, chargeback ratios, and effective fee rates. You must look beyond the headline MDR to find hidden costs like minimum monthly fees, statement charges, or terminal maintenance costs. A semi-annual audit is the industry standard for cost optimization because it allows businesses to renegotiate terms as their transaction volumes grow. This process ensures your provider's pricing remains competitive as your business scales. If your success rates are dipping below 95%, it's a clear signal that your current technical setup needs an overhaul.

Future-Proofing for 2026 and Beyond

The next phase of the national strategy involves the adoption of Central Bank Digital Currencies (CBDC) like Aber and the integration of AI-driven fraud detection. Modular payment stacks are superior to all-in-one legacy solutions because they allow you to swap specific components without disrupting your entire operation. This flexibility is essential for adopting new technologies as they emerge. By choosing an API-first approach, you ensure your business remains ready for the next wave of innovation in the digital economy. You can evaluate your current payment stack today to ensure you're ready for the shifts coming in 2026.

PaySelect helps you navigate these steps by providing an independent perspective on the market. We identify where your current setup falls short and match you with infrastructure that aligns with your specific industry needs. Whether you're moving away from cash on delivery or scaling your e-commerce presence, we provide the clarity needed to make informed decisions without the technical jargon.

Simplifying Infrastructure Selection with PaySelect

Navigating the UAE Payment Infrastructure shouldn't feel like a solo mission. While the national shift toward digital-first systems offers immense potential, the sheer variety of providers and technical requirements can lead to decision fatigue. PaySelect acts as an independent bridge. We connect your business to the most efficient financial technology without the bias of a single provider. Our mission is to transform payment processing from a complex cost center into a streamlined strategic asset.

For large-scale organizations and expansive hotel groups, the challenge often lies in reconciling high transaction volumes across multiple properties. Conversely, SMEs frequently find themselves trapped in a "black box" of fees, paying more than necessary because they lack market transparency. We solve these pain points through our "Take the Test" tool. This resource matches merchants with providers based on industry-specific infrastructure needs, ensuring your technical stack aligns perfectly with your operational goals. Whether you need robust POS machines for retail or a high-capacity payment gateway for e-commerce, we provide the clarity needed to choose with confidence.

The Power of Independent Comparison

Unbiased data is your most valuable asset when selecting a financial partner. Direct negotiations with providers are often un-audited, leaving businesses unaware of more competitive rates available in the wider market. PaySelect constantly monitors the landscape to ensure merchants access the most efficient pricing and technology. By using an independent comparison tool, you bypass the friction of traditional sales cycles. You gain a clear view of how different providers handle settlements, technical support, and regional compliance. This transparency empowers you to negotiate from a position of strength, securing terms that protect your margins as you scale.

Next Steps for Your Business

The deadline of September 16, 2026, for new Central Bank compliance is approaching fast. Now is the time to benchmark your current rates and audit your technical capabilities. Start by using the PaySelect tool to see how your current transaction costs compare to the market standard. Once you have your baseline, prepare for a consultation with a payment infrastructure expert who can help you navigate the transition to instant schemes like Aani or domestic cards like Jaywan. Don't let legacy systems hold back your growth in a digital-first economy. Streamline your operations, optimize your costs, and scale your reach today.

Secure Your Competitive Edge in the 2026 Landscape

The path to a cashless economy is now clearly defined. With the September 16, 2026, compliance deadline approaching, businesses must move beyond legacy thinking to protect their margins. You've learned how the UAE Payment Infrastructure is shifting toward real-time settlements and localized card schemes to reduce the typical 3.2% transaction cost burden. Eliminating the 25% cash-on-delivery rate isn't just about convenience; it's about unlocking the liquidity your business needs to expand.

PaySelect acts as your rock-solid financial partner in this transition. We offer independent and unbiased advisory services, providing expert-led cost optimization audits tailored for both SMEs and large-scale enterprises. Our matching tool removes the guesswork from provider selection, ensuring your technical stack is as efficient as possible. Take the next step and optimize your payment infrastructure with the PaySelect comparison tool. You have the ambition to grow; we provide the seamless technology to make it happen. Let's build a borderless future together.

Frequently Asked Questions

What are the main components of the UAE payment infrastructure?

The UAE Payment Infrastructure consists of three primary layers: retail payment systems like Aani, domestic card schemes like Jaywan, and the regulatory framework managed by the Central Bank of the UAE (CBUAE). These components work together to facilitate real-time money movement and digital settlements. This network replaces slow, legacy banking cycles with an API-driven ecosystem that supports 24/7 commerce across the Emirates.

How does the National Payment Systems Strategy (NPSS) affect my business?

The NPSS directly impacts your liquidity by enabling instant settlements and reducing the time capital stays locked in clearing cycles. It supports the Dubai Cashless Strategy goal of reaching 90% digital transactions by the end of 2026. For your business, this means moving away from expensive cash-on-delivery models, which still represent 20-25% of e-commerce orders, toward more efficient digital channels.

Is it mandatory for UAE businesses to accept instant payments like Aani?

Acceptance isn't strictly mandatory by law, but it's becoming a market standard as the Aani platform surpassed 12.5 million users in April 2026. Customers now expect the convenience of transfers that use only a mobile number. Ignoring these schemes can lead to lost sales, especially since the platform processes 25,000 daily transfers with a transaction limit of AED 50,000.

What is the Domestic Card Scheme (Jaywan) and how does it reduce costs?

Jaywan is the UAE's localized card scheme that ensures payment data is processed and stored within the country. It reduces costs for merchants by bypassing the high fees typically charged by international networks for local routing. This localization allows you to keep more of your revenue while providing a secure, government-backed payment method for your customers.

How can I reduce my merchant transaction fees in the UAE?

You can reduce fees by auditing your monthly statements for hidden costs and shifting volume toward domestic schemes or crypto gateways, which often charge between 0.4% and 1.0%. This is significantly lower than the standard credit card processing costs. Switching to an Interchange++ pricing model also provides the transparency needed to negotiate better rates as your transaction volume grows.

What should I look for when choosing a payment gateway for a new business?

Prioritize gateways that offer seamless API integration, support for national schemes like Aani, and full compliance with the Retail Payment Services and Card Schemes (RPSCS) regulation. You must also ensure the provider can handle your growth. Exceeding an average of AED 10 million in monthly transactions for three consecutive months triggers higher capital and governance requirements that your provider must manage.

How does the Central Bank of the UAE regulate digital payment providers?

The CBUAE regulates providers through the RPSCS Regulation and the new Federal Decree Law No. 6 of 2025. This law covers Open Finance and payment services using virtual assets. Additionally, all licensed financial institutions must adhere to the April 2026 prohibition on using instant messaging platforms like WhatsApp for customer transactions to ensure data security and consumer protection.

Can I use the same infrastructure for both local and cross-border payments?

Yes, modern modular stacks allow you to integrate local elements of the UAE Payment Infrastructure alongside international cross-border solutions. This unified approach simplifies your financial reconciliation and provides a consistent experience for both local residents and global tourists. Using a single technical bridge helps you manage multiple currencies and settlement types without the complexity of managing separate, disconnected systems.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.