Understanding Payment Gateway Approval Rates: A Merchant’s Guide to Revenue Recovery (2026)

Your payment gateway is either a catalyst for global expansion or a hidden drain on your bottom line. Every transaction that fails due to a "false decline" is more than a missed sale; it's a permanent loss of customer trust. Understanding payment gateway approval rates is no longer just a technical task for IT departments. It's a strategic necessity for any merchant aiming to capture their share of a digital economy projected to exceed $14 trillion in 2026.

We know that auditing your providers often feels like decoding a foreign language, especially when transparency is lacking. This guide provides a clear framework to master the factors behind transaction success so you can stop losing revenue to inefficient systems. You'll learn how to audit your current performance, negotiate better terms, and identify a gateway that offers superior authorization routing. We'll explore how modern infrastructure, such as AI-driven fraud prevention and payments orchestration, can transform your checkout from a point of friction into a seamless engine for growth. By comparing solutions and optimizing your costs, you can ensure your business remains fluid, competitive, and ready for the next level of international commerce.

Key Takeaways

• Learn to distinguish between hard and soft declines to pinpoint exactly where technical timeouts are draining your potential revenue.

• Gain a competitive edge by understanding payment gateway approval rates and the role 3D Secure protocols play in the modern UAE market.

• Discover why a one-size-fits-all gateway often fails and how to select a provider that offers the specific authorization routing your niche requires.

• Identify strategic improvements like tokenization and UI refinements that prevent common user-input errors and secure recurring billing success.

• Use independent comparison tools and performance audits to uncover hidden infrastructure bottlenecks and negotiate more favorable terms with providers.

The Mechanics of Payment Approval: Why Success Rates Matter in 2026

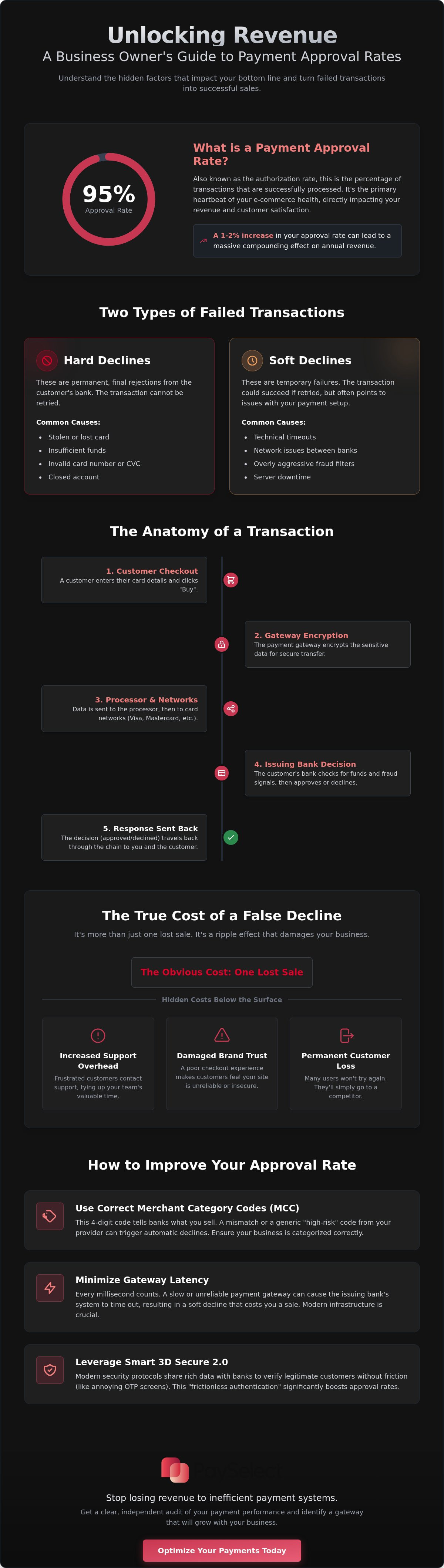

The payment approval rate, also known as the authorization rate, serves as the primary heartbeat of your e-commerce health. It represents the percentage of transactions that successfully clear the complex journey from a customer's wallet to your business bank account. In 2026, understanding payment gateway approval rates is the difference between a business that scales and one that stagnates. While many merchants focus solely on transaction fees, the real revenue driver is ensuring that legitimate customers don't face unnecessary barriers at checkout. High-performing businesses treat this metric as a strategic asset rather than a fixed cost.

Declines generally fall into two distinct categories. Hard declines occur when a transaction is permanently rejected, often due to a stolen card or insufficient funds. These are usually final. Soft declines are more insidious; these are temporary failures caused by technical timeouts, network issues, or overly aggressive fraud filters. By 2026 standards, your provider must offer real-time data transparency to help you distinguish between these types. A mere 1% to 2% increase in your approval rate can lead to a massive compounding effect on annual revenue. For high-volume merchants, this marginal gain often represents hundreds of thousands of dollars in recovered capital.

The Anatomy of a Transaction Flow

When a customer clicks the "buy" button, a high-speed data relay begins. The payment gateway encrypts the sensitive information and sends it to the payment processor, which then communicates with card networks and the issuing bank. Friction points often emerge during this relay, such as mismatched security protocols or outdated routing paths. The gateway acts as the secure messenger, and its ability to navigate these hurdles determines your success. Selecting the right infrastructure through a payment gateway comparison ensures your data path is clear, fast, and reliable.

Calculating the True Cost of Declines

The cost of a failed transaction extends far beyond the immediate loss of a sale. It impacts your customer lifetime value (CLV) significantly. A single false decline can permanently break brand trust, driving customers to shop with a competitor instead. Additionally, failed payments increase your operational friction. They drive up customer support overhead as frustrated users seek help for issues that shouldn't exist. PaySelect helps you identify these hidden bottlenecks. By utilizing a payment cost optimization audit, you can recover revenue that would otherwise be lost to technical inefficiencies and outdated system configurations.

Technical and Operational Factors Influencing Transaction Success

Understanding payment gateway approval rates requires a deep dive into the technical protocols that govern every click and swipe. In the UAE, where the government aims for 90% of financial transactions to be cashless by 2026, the technical bar is exceptionally high. Your infrastructure doesn't just need to work; it needs to excel under pressure. When a transaction fails, it's rarely a random event. It's usually the result of specific technical configurations that either build trust with the issuing bank or trigger an immediate red flag.

Merchant Category Codes (MCC) are a critical but often overlooked factor in this process. These four-digit numbers tell the issuing bank exactly what you sell. If your business is miscategorized, or if your provider places you in a generic high-risk bucket, your approval rates will suffer. Banks use these codes to assess risk levels instantly. If the code doesn't match the transaction profile, the bank is far more likely to issue a decline to protect themselves. Technical performance is equally vital. High gateway latency or frequent downtime can cause an issuing bank's system to time out, resulting in a soft decline that costs you a sale.

3DS 2.0 and Frictionless Authentication

The shift to 3DS 2.0 has revolutionized how we handle security in the MENA region. Unlike the original version which forced every customer through a clunky One-Time Password (OTP) screen, 3DS 2.0 uses rich data sharing. It sends over 100 data points to the bank, including device fingerprints and transaction history. This allows for frictionless authentication where the bank approves the sale without bothering the user. Smart merchants use specific exemptions for low-risk or low-value transactions to keep the checkout moving fast and improve their understanding payment gateway approval rates.

Fraud Management vs. Revenue Growth

Rigid fraud rules are often the biggest enemy of a healthy bottom line. "Set and forget" filters frequently block legitimate high-value orders because they don't fit a narrow, outdated profile. You need dynamic risk scoring that adapts to your specific industry and customer behavior. This is especially vital when handling international customers. Using specialized cross-border payment solutions helps you manage the different risk profiles of global markets without sacrificing local success.

Efficiency is your competitive advantage in a fast-moving digital landscape. If you're unsure if your current setup is optimal, exploring a payment gateway comparison can reveal where your technical performance is lagging and where revenue is being left on the table.

Evaluating Provider Performance: Why Gateways Are Not Created Equal

Selecting a partner based solely on a flat transaction fee is a common strategic error. On the surface, most providers promise similar connectivity, but the internal architecture determines your commercial ceiling. For merchants in niche industries or those handling high-ticket volumes, a one-size-fits-all approach often leads to sub-optimal results. These generic systems may lack the specific risk profiles required to handle your unique transaction flow, resulting in unnecessary declines that drain your revenue.

The distinction between direct acquirers and payment aggregators is a fundamental part of understanding payment gateway approval rates. Direct acquirers maintain a primary relationship with banking networks, which often results in faster processing and higher transparency. In contrast, aggregators group multiple merchants under a single umbrella. While aggregators offer rapid onboarding, they often provide less granular control over how your transactions are routed. In the national market, local acquiring is a non-negotiable advantage. Processing UAE-issued cards through local banks significantly reduces the likelihood of a transaction being flagged as suspicious by an international security filter. Key benefits of local acquiring include:

Higher Authorization Rates

Local banks trust local traffic more than foreign requests.

Reduced Fees

Eliminating cross-border surcharges improves your margins.

Faster Settlement

Localized paths often mean quicker access to your capital.

Smart Routing and Cascading Logic

Modern infrastructure must do more than just pass data; it must think. Smart routing automatically directs each transaction to the bank most likely to grant an approval based on historical performance and card type. If a transaction fails, cascading logic instantly retries the payment with a backup acquirer. This happens in milliseconds, remaining completely invisible to the customer. When selecting a payment gateway, you must audit whether these advanced recovery features are built into the core stack or if you're left with a static, single-path system.

Data Transparency and Decline Analysis

Transparency is the only way to audit your provider's true performance. You need access to Raw Response Codes, which are the specific, unfiltered messages sent back by the issuing bank. These codes tell you exactly why a bank said no. Analyzing these patterns reveals if failures happen more often with certain card types or during specific times of the day. A provider that offers deep data transparency and performance tuning becomes a strategic partner. PaySelect simplifies this evaluation by providing an unbiased comparison of how different providers handle these critical technical details, ensuring you find the right fit for your expansion goals.

Strategic Steps to Optimise Your Payment Acceptance

Strategic optimization turns a passive payment process into a high-performance revenue engine. While backend routing is vital, your front-end experience dictates the quality of data entering the system. Improving your bottom line starts with understanding payment gateway approval rates as a reflection of your entire user journey. Simple friction points often cause legitimate transactions to fail before they even reach the bank, resulting in lost sales that were easily preventable.

Monitoring your fraud-to-sales ratio is a critical part of this strategy. Many merchants are inadvertently too defensive. If your decline rate is exceptionally high but your chargeback rate is near zero, your fraud filters are likely blocking genuine customers. You need to find a balance where security protects your business without strangling your growth. This requires a dynamic approach to risk that evolves with your transaction history and customer behavior patterns.

Checkout UX and Data Accuracy

User-input errors remain a primary cause of transaction declines. Implementing real-time card validation catches typos in card numbers or expiry dates before the customer clicks "pay." This proactive approach reduces the volume of "invalid card" responses from issuers. Digital wallets like Apple Pay and Google Pay further enhance success rates by utilizing pre-validated data and biometric authentication, which banks perceive as lower risk. For businesses with physical locations, ensuring your POS machines and online gateways share a unified customer profile allows for smoother cross-channel verification and higher trust scores from issuing banks.

The Power of Local Payment Methods

National market penetration in the UAE requires more than just accepting major credit cards. The rapid rise of local initiatives like the Aani instant payments platform and the Jaywan domestic card network has changed consumer expectations. Offering these preferred local methods reduces the risk of "suspicious activity" flags that often plague international processing paths. Aligning your payment stack with these specific local schemes ensures your transactions are recognized as domestic traffic, which typically enjoys higher authorization success.

Beyond the immediate checkout, leveraging tokenization and "Account Updater" services can automate revenue recovery. Tokenization allows for seamless returning customer experiences, while updater services refresh expired card details in the background. If you're ready to audit your current infrastructure for these features, using a payment gateway comparison tool is the most efficient way to identify which providers offer the best technical stack for your specific needs.

Navigating the UAE Payments Landscape with PaySelect

In a landscape where the UAE e-commerce sector is projected to reach USD 13.8 billion by 2029, the margin for error in transaction processing is non-existent. Merchants often struggle with complex technical jargon and a lack of transparency in gateway reporting. PaySelect serves as an independent bridge, connecting businesses with high-performance infrastructure designed to maximize revenue. By focusing on understanding payment gateway approval rates, we help you move beyond surface-level fees to find the technical architecture that actually converts. Our platform ensures that technical utility isn't just a service, but a strategic tool for your business transformation.

For enterprise-scale organizations, the challenge is often reducing operational drag while increasing approval velocity. PaySelect helps identify hidden bottlenecks that traditional providers might overlook. By utilizing our payment infrastructure consulting, you gain a partner that values your time and security equally. We provide the structural clarity needed to present complex technical solutions as simple, manageable, and ready for implementation. This results in a frictionless flow that leads your business toward expansion without hesitation.

Unbiased Comparison for Strategic Growth

Independence is a rare asset in the payments sector. Many recommendations in the industry are driven by referral-heavy sales tactics rather than technical merit. PaySelect breaks this cycle by providing a data-driven, merchant-focused methodology. We analyze your specific transaction volume, geographic reach, and risk profile to identify the ideal payment gateway. Independence matters because your growth shouldn't be limited by a provider's commission structure. We offer a clear framework to audit performance, giving you the knowledge to negotiate better terms. Whether you need cross-border payment solution matching or a deep dive into authorization routing, our focus remains on your ultimate business outcome.

Getting Started: Your Path to Higher Approvals

Improving your success rates begins with a comprehensive audit of your current payment stack. Hidden bottlenecks, such as suboptimal routing or outdated fraud rules, often go unnoticed without an external review. PaySelect’s specialized tools are designed to match you with providers that excel in your specific category. During a Payment Cost Optimization Audit, we look for opportunities for technical refinement that typical providers might overlook. This process identifies exactly where you're losing revenue and provides a clear path to recovery. You'll gain the insights needed to select the highest-performing payment infrastructure for your unique needs.

Take the PaySelect test today to find your ideal payment partner and start your journey toward recovered revenue and seamless global expansion.

Transforming Payments into a Strategic Performance Catalyst

The difference between a successful transaction and a lost customer often rests on the technical infrastructure behind your checkout button. By prioritizing smart routing, leveraging 3DS 2.0 protocols, and embracing local acquiring strategies, you shift from defensive fraud management to proactive revenue recovery. These strategic adjustments ensure that your business remains fluid and ready to scale within the rapidly expanding UAE digital landscape.

Mastering the nuances of understanding payment gateway approval rates is the most direct path to improving your bottom line in 2026. You don't have to navigate this complex environment alone. PaySelect offers independent advisory, regional expertise, and cost optimization to help you identify the technical bottlenecks currently limiting your growth. We act as a bridge between complex global infrastructures and the intuitive needs of your business, ensuring every part of your payment stack is built for speed and reliability.

Find the highest-performing payment gateway for your business with PaySelect. It's time to build a payment stack that supports your international ambition and delivers the results your business deserves.

Frequently Asked Questions

What is a good payment gateway approval rate for UAE businesses?

High-performing merchants in the UAE typically aim for authorization rates above 90 percent. Elite performers who utilize advanced payments orchestration often achieve rates exceeding 97 percent. If your current rate falls below 85 percent, it usually indicates significant technical friction, suboptimal routing, or overly aggressive fraud filters that require immediate auditing to recover lost revenue.

How does 3D Secure 2.0 affect my transaction success rates?

3DS 2.0 improves success rates by facilitating frictionless authentication through the exchange of rich data between merchants and banks. This modern protocol reduces the need for disruptive One-Time Passwords (OTPs) on low-risk transactions. By providing more context to the issuing bank, you build trust and significantly decrease checkout abandonment caused by clunky legacy security steps.

Can changing my payment gateway really improve my authorization rates?

Yes, because different gateways offer varying levels of connectivity and routing intelligence. Understanding payment gateway approval rates involves recognizing that some providers have deeper local acquiring relationships in the UAE than others. Switching to a provider with superior cascading logic and smarter bank connectivity can immediately save transactions that your current system might decline.

What are the most common reasons for "soft declines" in online payments?

Soft declines usually stem from temporary technical hurdles such as network timeouts, system maintenance at the issuing bank, or sensitive fraud triggers. Unlike hard declines for insufficient funds, these are legitimate sales that fail due to infrastructure issues. Implementing automated retries or smarter routing paths can often recover these transactions without requiring any additional action from your customer.

How does local acquiring in the UAE differ from using a global gateway?

Local acquiring routes your transactions through UAE-based banks, which usually results in higher trust scores from local card issuers. Global gateways often process traffic through international hubs, which can trigger security red flags and cross-border surcharges. Using local infrastructure ensures your transactions are perceived as domestic traffic, leading to faster settlement and higher approval velocity.

What is smart routing and do I need it for my small business?

Smart routing is a technology that automatically directs each transaction to the bank most likely to approve it based on real-time data. While essential for high-volume enterprises, small businesses also benefit from this increased reliability. It removes operational barriers by ensuring your payments aren't dependent on a single, potentially unstable connection, providing a more professional experience for your customers.

How can I reduce false declines without increasing my risk of fraud?

You can achieve this by moving away from rigid, "set and forget" fraud rules toward dynamic risk scoring and 3DS 2.0. These systems analyze over 100 data points to verify legitimate users instantly. This approach maintains high security standards while ensuring that genuine customers enjoy a fluid checkout experience, effectively balancing revenue growth with robust protection against bad actors.

How often should I audit my payment gateway performance?

You should conduct a thorough performance audit at least once every six months. This frequency aligns with the biannual interchange rate updates from major card networks in April and October. Regular reviews ensure your understanding payment gateway approval rates stays current as regional regulations evolve, allowing you to optimize costs and identify new technical bottlenecks before they impact your bottom line.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.