By September 16, 2026, every payment provider in the UAE must comply with Federal Decree-Law No. 6 of 2025 or face criminal penalties. This massive regulatory shift arrives as the local e-commerce market climbs toward a projected 12.30 billion dollar valuation. For your business, understanding what is a payment aggregator vs payment gateway is no longer just a technical detail. It's a strategic necessity to protect your margins and ensure long-term compliance.

You probably know the frustration of high transaction fees cutting into your bottom line or complex KYC requirements that stall your growth for weeks. It's exhausting to deal with hidden costs that only surface after you've integrated a solution. We'll show you how to master the critical differences between aggregators and gateways to build a scalable, cost-effective payment infrastructure. This guide provides a clear look at which model fits your current volume, how to lower operational costs, and the fastest way to achieve a seamless time-to-market in the UAE's competitive digital economy.

Key Takeaways

• Distinguish between a payment gateway's secure data transmission and an aggregator's simplified merchant account structure to build a resilient infrastructure.

• Navigate the 2026 UAE regulatory landscape to ensure your payment model remains compliant with the latest Central Bank licensing requirements.

• Evaluate setup speeds and fee structures to choose a solution that balances fast market entry with sustainable transaction margins.

• Analyze what is a payment aggregator vs payment gateway to determine which model aligns with your business's current volume and technical resources.

• Utilize independent comparison tools and audits to optimize your payment stack and remove hidden operational barriers to growth.

Understanding the UAE Payment Ecosystem in 2026

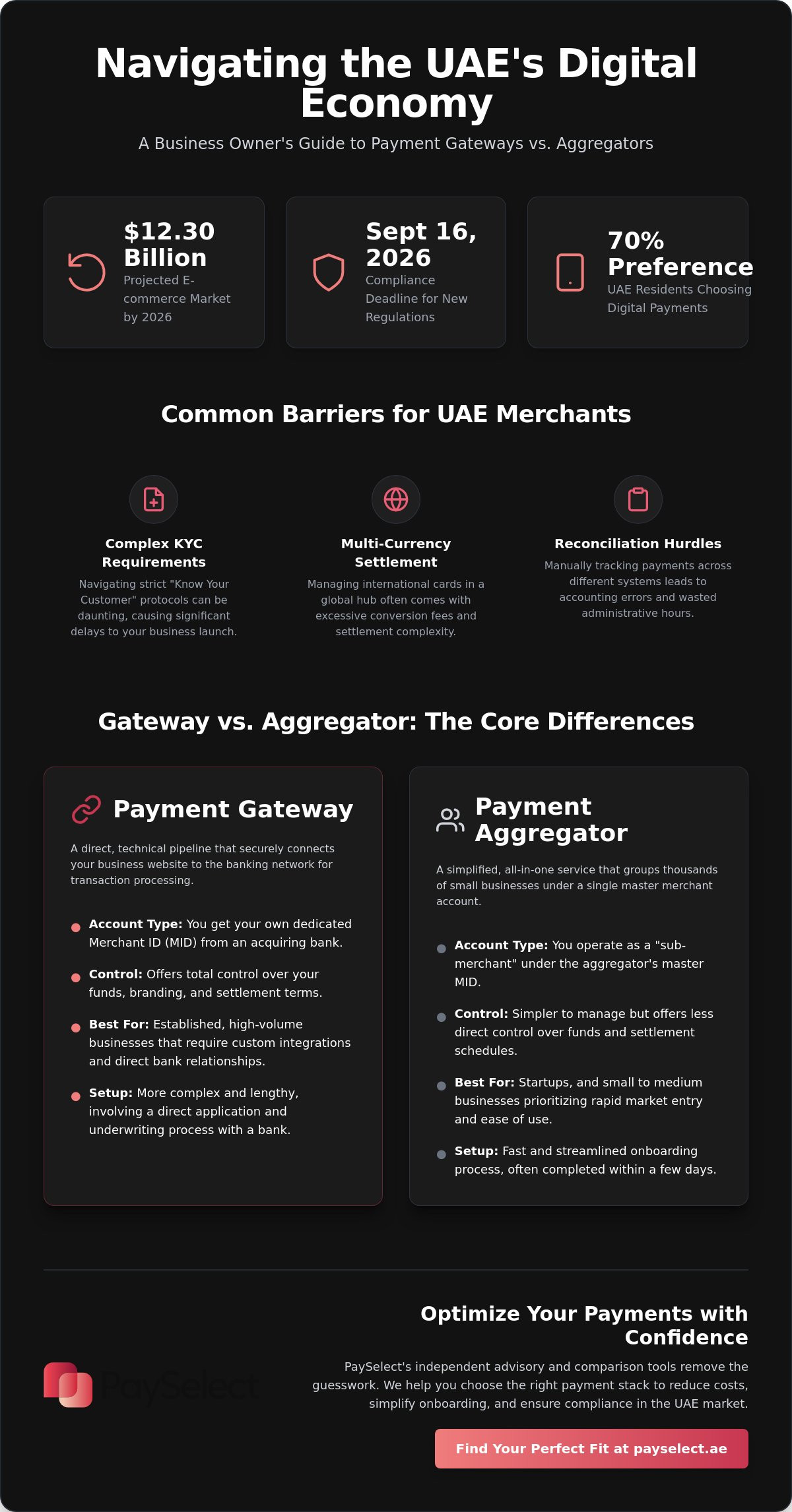

The UAE has moved beyond the era of cash-on-delivery dominance. By 2026, the e-commerce market is set to reach 12.30 billion USD, driven by a population that increasingly prefers a cashless lifestyle. This transition isn't just about convenience; it's a fundamental shift in how businesses must operate to survive. As a merchant, the decision between an "all-in-one" solution or a customized "best-of-breed" stack determines your operational agility and long-term profit margins.

The Central Bank of the UAE (CBUAE) has tightened the framework to ensure security and consumer protection. With the compliance deadline for Federal Decree-Law No. 6 of 2025 set for September 16, 2026, every Payment Service Provider must meet rigorous standards. This regulatory clarity helps legitimate businesses but adds complexity to the selection process. Many entrepreneurs struggle with fragmented terminology, often paying for premium features they never utilize because they don't fully grasp what is a payment aggregator vs payment gateway in the context of their specific needs.

The Surge in Digital Transactions

Digital adoption is accelerating across the Emirates. Nearly 70% of residents now prefer digital payments over cash, creating a market where a smooth checkout is mandatory rather than optional. This shift means your infrastructure choice is now a front-end competitive advantage. Customers expect speed, security, and variety. If your system can't handle the 60% of transactions now occurring on mobile devices, you're losing revenue to more agile competitors who have optimized their payment flow for a mobile-first audience.

Common Merchant Pain Points

Setting up a payment system in this high-growth environment is rarely simple. Ordinary business owners often face significant barriers that can delay a product launch by months. These challenges include:

Complex KYC Requirements

Navigating the "Know Your Customer" protocols required by the CBUAE can be daunting for new entrants.

Multi-Currency Settlement

Managing transactions in a global hub requires a system that handles international cards without excessive conversion fees.

Reconciliation Hurdles

Manually tracking payments across different platforms leads to accounting errors and wasted administrative hours.

PaySelect bridges these gaps by providing a Payment Gateway Comparison Tool and specialized infrastructure consulting. Instead of guessing, you get a data-driven roadmap to optimize your costs and simplify your onboarding process. Mastering the distinction of what is a payment aggregator vs payment gateway is the first step toward removing operational barriers and focusing on your international expansion.

Defining the Core Infrastructure: Gateway vs. Aggregator

Understanding the technical backbone of your business starts with a single question: what is a payment aggregator vs payment gateway? While these terms are often used interchangeably, they represent two distinct paths for moving money from a customer's wallet to your bank account. Choosing the wrong path can lead to higher fees, delayed settlements, or unexpected account freezes. Each model serves a specific business stage, and the right choice depends on your volume, technical capacity, and speed requirements.

The Payment Gateway: Your Direct Connection

A payment gateway serves as the "technical pipe" that links your website to the banking network. When you use a gateway, you must secure your own Merchant Identification Number (MID) from an acquiring bank. This individual account gives you total control over your funds and settlement terms. A payment gateway is the software that encrypts and transmits card data to the processor.

This model provides a direct relationship with financial institutions, offering stability for high-volume businesses. It's built for those who require custom integration and specific bank partnerships. If you're looking for a setup that scales with your enterprise needs, you can use our Payment Gateway Comparison Tool to find the right technical fit for your infrastructure.

The Payment Aggregator: The Simplified Interface

A payment aggregator operates differently by grouping thousands of small businesses under a single master merchant account. This "sub-merchant" model is detailed in the payment and settlement systems glossary, which highlights how these entities facilitate transactions for third parties. For a new UAE startup, this is often the fastest route to market because you don't need to sign a separate agreement with a bank.

Aggregators handle the heavy lifting of compliance and technical integration. You trade a bit of control for speed. Instead of waiting weeks for bank approval, you can often start accepting payments within 24 to 48 hours. It's a frictionless way to test a new product or enter the market without a massive upfront investment.

Shared Infrastructure vs. Individual Accounts

The fundamental difference lies in how the infrastructure is shared. An aggregator is a collective environment. You share the master account's reputation and risk profile with other merchants. If one merchant in the group triggers a high volume of chargebacks, it could potentially impact the entire group's processing status. This is a common pain point for businesses that scale quickly and suddenly find their funds held for review.

A gateway, conversely, is an isolated environment. Your MID is yours alone. Your funds flow directly from the processor to your business bank account without passing through a third party's master account first. This distinction is the core of the what is a payment aggregator vs payment gateway debate. While aggregators offer simplicity and rapid onboarding, gateways provide the dedicated infrastructure required for complex, high-volume operations.

Comparing the Operational Models: Which One Wins?

Deciding which model wins requires looking past technical definitions to the daily operational impact on your cash flow. While an aggregator offers a rapid entry point, a dedicated gateway provides the structural integrity needed for high-volume scaling. The choice often boils down to a trade-off between immediate speed and long-term cost efficiency. The debate over what is a payment aggregator vs payment gateway often centers on these specific operational trade-offs that determine your business's agility.

Control and customization represent the next major divide. A gateway allows you to brand the checkout experience entirely, maintaining a seamless user journey that builds trust. You own the data. You manage the relationship. Aggregators often redirect customers to a hosted payment page, which can occasionally disrupt the conversion funnel for high-end brands. For businesses looking to expand internationally, the ability to customize every touchpoint becomes a significant strategic asset.

Fee Structures and Hidden Costs

Aggregator pricing models are built for simplicity. You typically face higher per-transaction fees, ranging from 2.5% to 2.9% plus a fixed fee of around AED 1.00. There are usually no setup costs, making it attractive for low-volume startups. It's important to remember that a 5% VAT applies to all payment service charges in the UAE. These costs can compound quickly as your sales grow.

Gateways operate on a tiered structure that rewards volume. You pay monthly fees, often ranging from AED 99 to over AED 300, but you benefit from lower transaction rates. Identifying hidden charges like statement fees, PCI compliance levies, or early termination penalties is crucial. Using a payment pricing comparison tool helps you uncover these variables before they impact your margins.

Onboarding and Scalability

Aggregators deliver on the 24-hour setup promise. They remove the friction of individual bank negotiations, allowing you to go live almost instantly. This speed is a massive advantage for testing new markets or launching seasonal campaigns. It's the ultimate tool for a fast time-to-market when you don't have the luxury of waiting weeks for bank approvals.

High-growth companies eventually find the aggregator model restrictive. As your monthly volume increases, the higher transaction fees become a bottleneck. Migrating to a dedicated gateway allows for better liquidity management and faster settlement cycles. This transition ensures your infrastructure supports your ambition. PaySelect simplifies this evolution through a Payment Cost Optimization Audit, ensuring your stack remains lean as you scale. Understanding what is a payment aggregator vs payment gateway at each stage of your growth prevents you from outgrowing your infrastructure prematurely.

Choosing the Right Fit for Your Business Stage

Selecting the right infrastructure requires an honest assessment of your current transaction volume and technical resources. The debate over what is a payment aggregator vs payment gateway isn't about which technology is superior. It's about which model removes the most barriers for your specific stage of growth. Startups usually need speed. Enterprises need surgical precision over their margins. Your choice today should reflect where you intend to be in twelve months.

The SME Perspective: Prioritizing Ease of Use

For small and medium enterprises, reducing technical overhead is a survival tactic. Small teams can't afford to manage complex bank integrations or dedicated compliance officers. An aggregator provides immediate access to integrated tools like invoicing and payment links, which are essential for businesses moving away from cash. You can compare payment gateways for SMEs to see how these all-in-one solutions simplify your daily operations and speed up your time-to-market.

The Enterprise Perspective: Prioritizing Cost and Control

As your monthly volume climbs, the math changes. Enterprise-level merchants benefit from direct bank relationships that allow for negotiated rates and faster settlements. Customizing the user journey becomes a strategic priority to maximize conversion rates. Payment orchestration is also critical for those managing multi-region operations, especially since 58% of UAE online purchases are made from international vendors. A dedicated gateway provides the granular data needed to optimize every dirham spent on processing.

Many sophisticated businesses now adopt a hybrid approach. They use an aggregator for fast expansion into new markets while maintaining a dedicated gateway for their core high-volume traffic. This creates redundancy. It ensures that a single technical failure doesn't halt all revenue. Avoid the common pitfall of signing long-term contracts with high exit fees before you've tested your volume projections. Understanding what is a payment aggregator vs payment gateway allows you to build a stack that is both resilient and cost-effective.

Use our Payment Gateway Comparison Tool to find the infrastructure that aligns with your growth trajectory.

Optimizing Your Payment Stack with Independent Advisory

Independence is the cornerstone of a high-performing payment infrastructure. Most providers will naturally advocate for their own specific model, whether it's a gateway or an aggregator. This creates a conflict of interest that often leaves merchants with suboptimal rates or rigid systems that don't scale. PaySelect operates with absolute neutrality. We don't process payments; we provide the intelligence you need to choose the right partner. By clarifying what is a payment aggregator vs payment gateway based on your specific transaction data, we ensure your stack is built for performance rather than provider profit.

Our "Take the Test" tool matches your business profile to the right provider in seconds. This data-driven approach removes the guesswork from your decision-making process. Professional infrastructure audits further refine this by identifying inefficiencies in your current setup. Data wins every time. When you align your infrastructure with your actual volume, you eliminate technical bottlenecks and protect your margins from unnecessary erosion.

The PaySelect Advantage

Our approach centers on transparency and operational fluidity. We offer an unbiased comparison of UAE payment providers, focusing on the ultimate business outcome rather than brand loyalty. Many businesses suffer from "leaking" revenue due to inefficient routing or outdated fee structures that no longer match their size. Our advisory services identify these hidden costs and provide a clear roadmap for recovery. This is especially critical for international growth. For instance, optimizing cross-border payment costs can significantly improve your bottom line in a market where international purchases are a major revenue driver. We act as a bridge between complex global infrastructures and your need for simple, manageable implementation.

Actionable Next Steps for Merchants

Waiting for the September 16, 2026, regulatory deadline is a risk you don't need to take. Proactive planning is the only way to ensure continuity. Start by conducting a self-audit of your current transaction volume and fee breakdown. Use our comparison tools to benchmark your current provider against the wider market. If you're processing high volumes, even small percentage differences translate into thousands of dirhams in annual savings.

Consulting with experts now allows you to prepare for the shifts in the UAE digital landscape. We help you resolve the what is a payment aggregator vs payment gateway dilemma by matching your unique transaction profile to the most cost-effective infrastructure. This ensures your business remains compliant, scalable, and ready for the 12.30 billion dollar e-commerce market of 2026. Efficiency is a competitive advantage. Secure yours today.

Future-Proof Your UAE Payment Infrastructure

The UAE digital economy moves at a relentless pace. With the September 2026 regulatory deadline approaching, your choice of infrastructure dictates your ability to scale without friction. You've seen how aggregators provide the speed needed for immediate market entry, while dedicated gateways offer the control required for high-volume enterprise operations. Understanding what is a payment aggregator vs payment gateway in the context of your specific transaction data is the only way to protect your margins from hidden costs and operational bottlenecks.

PaySelect provides the clarity you need through independent and unbiased advisory services. Leveraging deep MENA payment industry expertise, we help everyone from ambitious startups to global hotel groups optimize their payment stacks. We identify leaking revenue and match you with providers that align with your long-term expansion goals. Don't let technical complexity stall your growth in a market projected to reach 12.30 billion dollars.

Match your business with the perfect payment solution today and build a foundation that's ready for the future of international commerce.

Frequently Asked Questions

Is a payment aggregator the same as a payment processor?

No, they perform different roles in the transaction chain. A payment processor is the technical entity that moves money between banks. An aggregator is a service provider that uses its own master merchant account to process payments for multiple smaller businesses. This distinction is a key part of understanding what is a payment aggregator vs payment gateway, as one provides the account while the other provides the technology.

Do I need a separate bank account for a payment gateway?

Yes, using a dedicated gateway usually requires a separate merchant account. Unlike the aggregator model, where you use a shared account, a gateway connects your specific Merchant Identification Number (MID) to the banking network. This setup gives you more control over your funds and settlement schedules. It's a standard requirement for businesses that have outgrown the simplified sub-merchant structure of an aggregator.

Which is safer for customers: an aggregator or a gateway?

Both models provide high levels of security as long as the provider is PCI DSS compliant. Gateways and aggregators both encrypt sensitive data to protect against fraud. The primary difference lies in the user experience. A gateway often allows for a fully integrated checkout on your own site. An aggregator might redirect customers to a hosted page, but both must adhere to the same Central Bank of the UAE security standards.

Can I switch from an aggregator to a gateway later as I grow?

Yes, migrating from an aggregator to a gateway is a common growth strategy. As your transaction volume increases, the higher percentage fees of an aggregator can become a significant operational burden. Switching to a gateway allows you to negotiate better rates directly with banks. This transition helps you lower your overall processing costs while gaining more control over your customer's checkout journey and data.

How long does it take to get approved for a dedicated merchant account in the UAE?

Approval for a dedicated merchant account typically takes between 2 to 4 weeks. This timeline is due to the extensive "Know Your Customer" (KYC) requirements and background checks performed by UAE banks. In contrast, aggregators can often approve new sub-merchants within 24 to 48 hours. If you need a fast time-to-market, starting with an aggregator while applying for a dedicated gateway is often a smart move.

Are payment aggregators more expensive than gateways for high-volume businesses?

Yes, aggregators are generally more expensive once you reach a certain scale. They typically charge higher transaction fees, often ranging from 2.5% to 2.9% plus a fixed fee. While they have no monthly costs, these percentages add up quickly. Gateways often have monthly fees but offer much lower transaction rates. Understanding what is a payment aggregator vs payment gateway helps you identify the tipping point where a gateway becomes more cost-effective.

What are the main PCI compliance differences between these two models?

Aggregators typically simplify the compliance process by handling most PCI DSS requirements on your behalf. Since you're using their shared infrastructure, they take on the majority of the security burden. With a dedicated gateway, your level of responsibility depends on your integration method. If you host the payment form on your own servers, you'll face much stricter compliance audits and technical requirements to ensure data security.

Can I use an aggregator for international cross-border payments?

Yes, most aggregators in the UAE are built to handle international transactions and multiple currencies. This is a vital feature considering that 58% of online purchases in the UAE are made from international vendors. While aggregators make it easy to accept global cards, keep an eye on currency conversion fees. These costs can vary significantly between providers, so it's essential to compare total costs before committing to a specific partner.

Disclaimer

This content is for informational purposes only and should not be considered financial, legal, or regulatory advice. Payment provider availability, pricing, and approval processes vary depending on individual business circumstances. PaySelect does not guarantee provider acceptance or specific outcomes. Businesses should conduct their own due diligence before entering into any agreements.